Nvidia shares have increased 11-fold in four years, but Wall Street analysts are still bullish.

Nvidia (NVDA 2.57%) shares advanced 1,080% during the last four years, meaning $10,000 invested in the semiconductor company in May 2020 would now be worth $118,000. To put those numbers in context, the S&P 500 (^GSPC 0.70%) returned 91% during the same period, such that $10,000 invested four years ago would now be worth $19,100.

Nvidia brought its share price down with a 4-for-1 stock split in July 2021, and the company now has a 10-for-1 stock split planned for next month. After the market closes on Friday, June 7, shareholders will receive nine new shares of Nvidia stock for every share owned at the previous close. To be clear, the split will have no direct impact on the value of the company, but it will make shares more affordable.

Despite Nvidia’s phenomenal run, 90% of Wall Street analysts that follow the company still rate the stock a buy, and the other 10% rate the stock a hold. Not a single analyst recommends selling. Nvidia bears a median price target of $1,200 per share, implying about 13% upside from its current price of $1,064 per share.

Here’s what investors should know about this artificial intelligence stock.

Nvidia is a leader in accelerated data center computing

Nvidia is best known for its graphics processing units (GPUs), chips that are the gold standard in (1) rendering ultra-realistic computer graphics in multimedia like video games and (2) accelerating complex data center workloads like artificial intelligence (AI) applications. The company has an exceptionally strong presence in both markets, though its largest growth opportunities lie in the latter category.

For context, Wells Fargo data compiled by Eric Flaningam suggests that Nvidia accounted for 98% of data center GPU spending in 2023, and the company is expected to capture 94% market share in 2024. Perhaps more important, Nvidia accounted for 92% of spending on data center GPUs used for generative AI workloads in 2023, according to IoT Analytics.

That dominance is due in part to its full-stack strategy. GPUs are only one element of the data center stack, but other components are needed to build and run complex applications. That includes central processing units (CPUs), networking platforms, and software development tools. Nvidia addresses every layer of the stack. That makes the company a one-stop shop for AI training and inference, and it supports the rapid innovation that has kept Nvidia ahead of its peers.

CEO Jensen Huang commented on that advantage during the latest earnings call. “We’re moving so fast and advancing [our systems] quickly because we have all the stacks here. We literally build the entire data center and we can monitor everything, measure everything, optimize across everything,” he told analysts. “This deep intimate knowledge at the entire data center scale is fundamentally what sets us apart today.”

Nvidia just delivered another blockbuster financial report

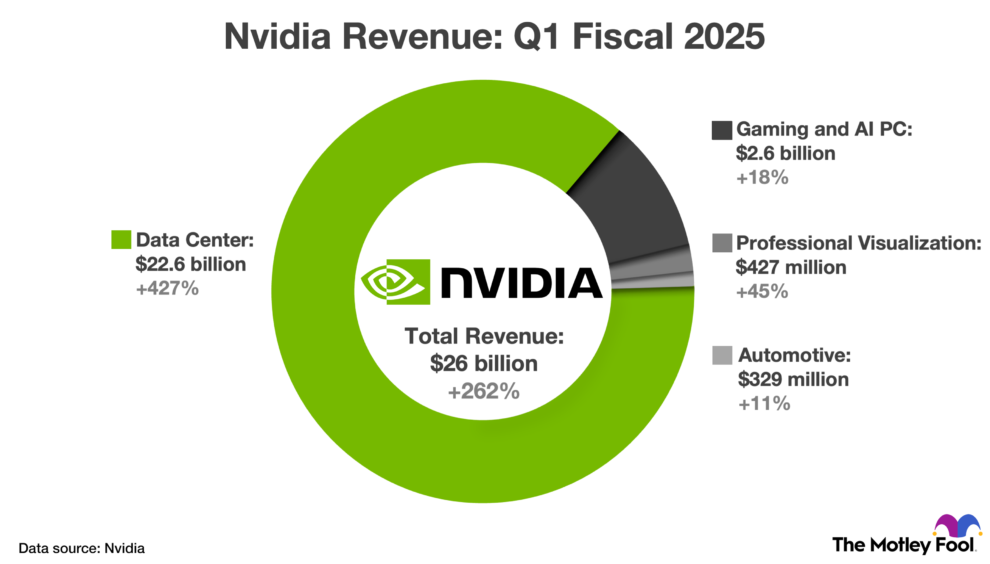

Nvidia reported financial results for the first quarter of fiscal 2025 (ended April 28, 2024) that easily surpassed Wall Street’s expectations. Revenue rose 262% to $26 billion on exceptional sales growth in the data center product category, which itself was driven by demand for generative AI systems. Meanwhile, non-GAAP net income soared 461% to $6.12 per diluted share.

The chart below provides more detail on first-quarter revenue growth across Nvidia’s four primary product categories.

Nvidia’s revenue growth by product category in the first quarter of fiscal 2025 (ended April 28, 2024). OEM & Other was excluded because it represented just 0.3% of total revenue.

Looking ahead, Nvidia guided for $28 billion in second-quarter revenue, implying 75% growth. That easily beat the $26.6 billion Wall Street analysts anticipated. Management also guided for roughly $15.5 billion in non-GAAP net income, implying about 130% growth.

More importantly, CFO Colette Kress recently told analysts that “demand may exceed supply well into next year” due to the upcoming launch of Blackwell, the name given to Nvidia’s next-generation AI factory platform. The Blackwell GPU architecture delivers up to four times faster AI training and 30 times faster AI inferencing as compared to the previous Hopper GPU architecture.

Nvidia stock trades at a somewhat reasonable valuation

The graphics processor market is forecasted to compound at 28% annually through 2030, and AI spending across hardware, software, and services is projected to grow at 37% annually during the same period, according to Grand View Research. Based on those estimates, Nvidia has a good shot at annual earnings growth in the low-30% range (plus or minus a few points) through the end of the decade.

Indeed, Wall Street expects the company to grow earnings per share at 38% annually over the next three to five years. That consensus estimate makes the current valuation of 62.3 times earnings seem relatively reasonable, especially compared to other AI stocks. I say that because those values (the price-to-earnings ratio divided by the forecasted earnings growth) give Nvidia a PEG ratio of 1.6. Meanwhile, chipmaker Advanced Micro Devices has a PEG ratio of 5.8, and cloud services providers Alphabet and Microsoft have PEG ratios of 1.5 and 2.7, respectively.

That does not mean Nvidia shares are cheap, but the stock is (arguably) cheaper than AMD and Microsoft, and nearly as cheap as Alphabet. I think investors can buy a few shares of Nvidia right now, provided they keep their purchases small (maybe 2% of their portfolios). Investors should also understand the risks associated with Wall Street’s lofty expectations. Nvidia stock could implode if the company fails to match earnings growth projections set by analysts.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Wells Fargo is an advertising partner of The Ascent, a Motley Fool company. Trevor Jennewine has positions in Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.