The AI server play should see hypergrowth for at least the next few years.

The artificial intelligence (AI) revolution is in full swing, and according to one Wall Street analyst, things don’t appear to be slowing down any time soon for one extremely well-positioned company.

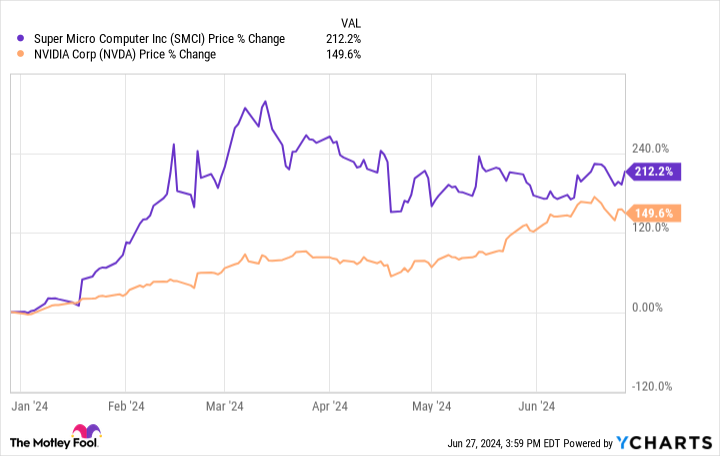

While most investors are gravitating toward chip leader Nvidia (NVDA -0.36%) at the moment, AI is and will continue to mint other market winners as well. In fact, one S&P 500 AI company has outperformed even Nvidia this year. And despite this stock’s impressive 2024 run, one Wall Street analyst predicts another 70% surge.

Super Micro Computer has beaten Nvidia and is ready for a liquid cooling breakout

This year, server-maker Super Micro Computer (SMCI -7.98%) has already surged 212%, handily outperforming Nvidia’s impressive 149% year-to-date gain.

Supermicro has undoubtedly benefited handily from a close partnership with Nvidia as a preferred server partner. However, the company has also been gaining market share thanks to its in-house engineering prowess.

Supermicro’s strategy of building servers out of “building block” pieces allows for fast, large-scale customization while also saving customers money. With the building block architecture, parts of a server are easily swapped and upgraded rather than having to replace the whole unit.

Moreover, the building block architecture and close relationship with Silicon Valley tech companies generally allow Supermicro to custom-build servers faster than rivals. With so many companies falling over themselves to build advanced AI infrastructure as quickly as possible, it’s no wonder customers are flocking to Supermicro’s solutions.

In addition, Supermicro’s longtime ethos of resource-saving, energy-efficient design has come to the fore in the age of AI. AI chips require a tremendous amount of energy and must dissipate lots of heat. To help further lower energy costs, Supermicro is now rolling out its own direct liquid cooling (DLC) technology.

DLC technology has been around for decades. However, because it’s an added cost and can take a long time to deploy in a data center, it has garnered only around 1% of the data center market.

However, AI servers are becoming extremely energy-intensive and will soon require DLC as opposed to air-cooled racks. DLC data centers limit the need for extensive air conditioning systems, saving both energy and space within the data center and thereby allowing even denser server clusters.

From its mere 1% market share, CEO Charles Liang expects a wave of DLC deployments to make up 15% of Supermicro racks this year and 30% next year. According to Liang, Supermicro can deliver DLC solutions within weeks today, and DLC deployment can help reduce data center power usage by up to 40%.

So, despite the company’s 200% revenue growth last quarter, DLC’s benefits to customers should help keep up the company’s hypergrowth and margins for the foreseeable future.

Is Super Micro Computer going to $1,500 per share? Image source: Getty Images.

Loop Capital thinks Supermicro is going to $1,500

Over the past few years, Supermicro has routinely trounced even the most bullish analyst expectations. But with this year’s admission to the S&P 500 Index, many more Wall Street analysts have begun covering the stock.

One of the most bullish is the technology-centered research shop Loop Capital. In April, Loop analyst Ananda Baruah raised his price target on Super Micro Computer from $600 to $1,500 per share.

Explaining the increase, Baruah correctly noted that Supermicro has developed a reputation as “an increasing leader in the need for both complexity and scale” for AI deployments. Furthermore, Baruah sees Supermicro’s speed and agility as a key factor, elaborating, “While it’s not truly possible to know the magnitude of these wins or timeframe of deployments, there has been a general industry dynamic of standing up deployments faster as opposed to slower.”

To obtain his valuation, Baruah sees Supermicro earning between $50 and $60 in fiscal 2026, ending in June of 2026, on revenue of between $30 billion and $40 billion. That compares with estimates for nearly $15 billion in revenue and $24 billion in fiscal 2024, which ends today, June 30.

With that type of growth and earnings power, Baruah thinks Supermicro can retain a 25 to 30 price-to-earnings (P/E) ratio, even in 2026. So, 30 times $50 or 25 times $60 gets one to his $1,500 target.

Supermicro could be more advantaged than Nvidia

While Nvidia is the king of AI chips today, the company is also due to receive an onslaught of competition from other processor companies and cloud giants’ custom ASICs (application-specific integrated circuits). However, Supermicro’s servers can house any kind of AI chip.

Thus, Supermicro should see continued growth and share gains no matter which AI chip wins the day or even if the wins are spread out among several chipmakers. That makes the stock a solid buy today, even after its impressive year-to-date gains.

Billy Duberstein and/or his clients have positions in Super Micro Computer and has the following options: short January 2025 $1,840 calls on Super Micro Computer, short January 2025 $110 puts on Super Micro Computer, short January 2025 $125 puts on Super Micro Computer, short January 2025 $130 puts on Super Micro Computer, short January 2025 $280 calls on Super Micro Computer, and short January 2025 $85 puts on Super Micro Computer. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.