One key Nvidia competitor looks increasingly attractive in the current environment.

When it comes to finding a top artificial intelligence (AI) stock to buy, investors may feel little motivation to look beyond Nvidia. Indeed, CEO Jensen Huang’s decision to develop AI chips before Nvidia’s competitors made it the dominant chip company in a lucrative and fast-growing niche. Naturally, investors want to own such a stock.

However, despite Nvidia’s market lead, many investors will balk at the stock’s valuation. Indeed, given its stock price, Nvidia looks to have little room to exceed the market’s high expectations. This situation may prompt investors to look for opportunities in other AI stocks, and one Nvidia competitor could become an excellent alternative.

Consider this top AI stock

Investors looking for AI opportunities outside of Nvidia may want to consider one of its leading competitors, Advanced Micro Devices (AMD -4.00%).

To counter Nvidia’s lead in AI chips, AMD has released AI accelerators of its own. Its MI300 series of chips serves as an alternative for many customers who cannot obtain or afford Nvidia’s more expensive AI chips.

In fact, Oracle just chose AMD’s MI300X chips to power its latest OCI Compute Supercluster instance. This win is a sign AMD has become a more formidable competitor in this market.

Following up on the MI300X chips, AMD plans to release the MI325X chips late this year. These will allow up to 288GB of memory and will accommodate bandwidths of up to 6 terabytes per second.

Moving forward, AMD will introduce its upgraded CDNA architecture in 2025, which should increase computational throughput. Given the company’s history of catching and sometimes surpassing its competitors, these advances could be significant for AMD and the AI chip industry at large.

Signs of improvement

Admittedly, AMD’s current financials are unlikely to impress investors. The $11 billion of revenue for the first half of the year rose only 6% yearly. Also, the $388 million in net income for that period shows it has only begun to recover from the $112 million in losses in the year-ago quarter.

However, the data center segment, which manages its AI chips, earned revenue of $5.2 billion in the first half of the year, a 98% yearly increase.

Also, the data center segment’s proportion of total revenue grew from 24% in the first two quarters of 2023 to 46% in the first half of this year. This is likely mimicking the growth pattern of Nvidia, which now derives 88% of its revenue from the data center segment. Three years before, the data center segment was not even Nvidia’s largest, a testament to how much AI accelerators can transform a semiconductor company.

Furthermore, massive revenue drops in AMD’s gaming and embedded segments contributed to its tepid growth rate. Assuming AMD can return those segments to a growth mode (or at least stop the declines), the company’s financial picture should improve.

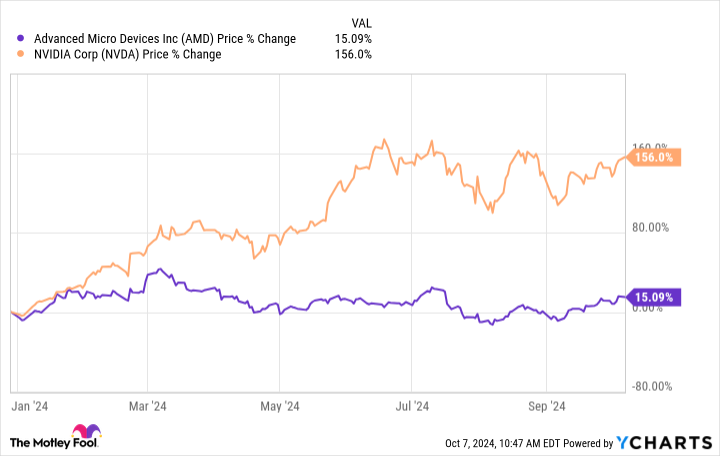

So far, AMD’s growth has lagged behind its rival, as its stock has risen by just 15% compared to Nvidia’s more than 155%. Also, the recent return to profitability has arguably made the P/E ratio a poor representation of its valuation.

Nonetheless, AMD stock sells for 12 times sales, compared to Nvidia’s price-to-sales (P/S) ratio of 33. If AMD can close much of its competitive gap, that stock may be ready to skyrocket as AI chips become an increasingly dominant revenue stream for the company.

Investing in AMD

Given this potential, the time may be now for AMD.

Indeed, Nvidia’s early lead in AI chips caught the company by surprise. However, it has worked to compete and innovate in this field, and the revenue numbers confirm that. Like with Nvidia, AMD’s data center segment is becoming increasingly dominant thanks to its growing sales in AI chips.

Additionally, AMD’s stock price growth has been tepid this year, likely due to significant declines in the gaming and embedded segments.

Still, the market has priced Nvidia’s stock for perfection, implying limited upside in the near term. In contrast, AMD has tremendous upside if it can maintain growth rates with AI chips and return these struggling segments to growth. That could set up the conditions needed for AMD’s stock to outperform Nvidia, even if it has not closed the technical gap.

Will Healy has positions in Advanced Micro Devices. The Motley Fool has positions in and recommends Advanced Micro Devices, Nvidia, and Oracle. The Motley Fool has a disclosure policy.