These companies are on track to win big from their lucrative niches thanks to AI.

Investing in solid companies and holding them for a long time is a robust strategy that could help investors significantly boost their wealth in the long run and construct a million-dollar portfolio. This strategy allows investors to capitalize on disruptive and secular growth trends, as well as benefit from the power of compounding.

For instance, a $10,000 investment in shares of Nvidia a decade ago is now worth a whopping $1.94 million. A big reason why Nvidia has made investors richer in the past decade is the secular growth trends in the gaming and data center segments, and the advent of artificial intelligence (AI) has supercharged the company’s growth.

Of course, it would be difficult for other AI stocks to deliver Nvidia-like gains, but investing in companies that are on track to capitalize on AI development could help investors get rich over time and even help them get close to their goal of becoming millionaires.

In this article, I will take a closer look at Palantir Technologies (PLTR 0.51%) and Taiwan Semiconductor Manufacturing (TSM -0.36%), two companies that are playing a crucial role in the AI space. Investing in these two names and including them in a diversified portfolio could eventually help investors construct a million-dollar portfolio in the long run. Let’s look at the reasons why.

1. Palantir Technologies

Palantir Technologies is sitting on a huge growth opportunity within the AI software market. According to Bloomberg Insights, the demand for generative AI software could generate $280 billion in additional revenue through 2032. Palantir has delivered $2.33 billion in revenue in the past 12 months, indicating that it is at the beginning of a terrific growth curve within the AI software market.

The good part is that Palantir has already started gaining traction in the AI software space. This is evident from the metrics that the company reported for the first quarter of 2024. Palantir, which was primarily known for supplying data analytics and software platforms to government agencies, is now targeting commercial customers with its AI software platform. This has led to a nice jump in its commercial customer base.

For instance, in the first quarter of 2024, Palantir’s count of commercial customers in the U.S. increased by an impressive 69% year over year. What’s more, the total contract value of U.S. commercial customers was up 131% from the year-ago period to $286 million. This stronger growth in the contract value as compared to the customer count indicates that Palantir is driving greater spending from each customer.

The overall commercial customer count was up 53% year over year to 427 last quarter. In all, Palantir’s overall commercial revenue increased 27% year over year in the first quarter to $299 million, outpacing the 21% growth in the company’s overall revenue. Palantir management said on the company’s latest earnings conference call that the new customers it is landing are “expanding their work with us.”

Citing home improvement retailer Lowe’s, Palantir said that the company has “accelerated its engagement from a starting point of no AI to utilizing production level AI for over 1,000 customer service agents, resulting in a 75% reduction in overdue tasks.”

Not surprisingly, Palantir says that more customers are expanding their use of its AI software, which helped boost the company’s revenue.

This is evident from the 38% year-over-year jump in Palantir’s remaining performance obligations (RPO) last quarter, which is a metric that refers to the total value of its future contracts that are yet to be fulfilled. It won’t be surprising to see this metric heading higher in the future thanks to the secular growth opportunity in the AI software market, especially considering that Palantir is among the top two players in this space.

All this explains why analysts are forecasting Palantir’s earnings to increase at an impressive annual rate of more than 85% for the next five years. The long-term growth opportunity in the AI software market indicates it could sustain impressive levels of growth for a long time to come. That’s why investors looking to add an AI stock to their portfolios that could help them become millionaires should consider buying Palantir before it flies higher.

2. Taiwan Semiconductor Manufacturing

Taiwan Semiconductor Manufacturing, popularly known as TSMC, is playing a pioneering role in the proliferation of AI. Nvidia may hold the limelight because of its dominance in the market for AI chips, but the graphics specialist wouldn’t have delivered such outstanding growth in revenue and earnings without TSMC.

That’s because Nvidia is a semiconductor company that designs the chips but doesn’t manufacture them. The manufacturing is done by foundries such as TSMC. This explains why TSMC is witnessing a turnaround in its fortunes.

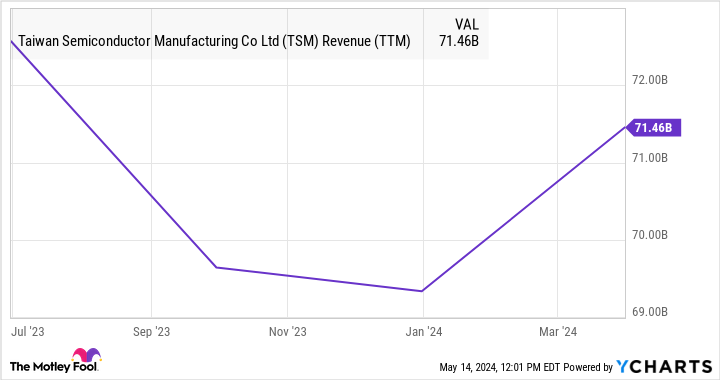

TSM Revenue (TTM) data by YCharts

The semiconductor market contracted 8.2% last year thanks to weak chip demand from the smartphone and personal computer (PC) markets. However, the market returned to growth in the fourth quarter of 2023 with an 11.6% year-over-year increase in revenue, which can be attributed to the AI-driven demand for chips.

This year, the semiconductor industry’s revenue is expected to jump 13%. AI is going to play a central role in this turnaround as the AI chip market is forecast to grow at an annual rate of 38% through 2030, generating an annual revenue of $207 billion at the end of the forecast period. TSMC is poised to take advantage of this secular growth opportunity because it is the world’s leading semiconductor foundry with a market share of 61%.

Also, TSMC’s manufacturing services are not only used by Nvidia but also by other companies such as Intel and AMD. All this explains why TSMC reported impressive growth last quarter. Additionally, its revenue for April shot up an impressive 60% year over year, indicating the terrific momentum it is now witnessing.

TSMC is working to produce more advanced chips, such as the 3-nanometer chips it expects will help create products worth a massive $1.5 trillion over a five-year period. There is a good chance that the company will remain the foundry of choice for chipmakers looking to capitalize on the AI boom.

As such, TSMC is a top semiconductor stock that investors can buy right now to make the most of AI proliferation. Its shares are trading at just 24 times forward earnings, a discount to the Nasdaq-100‘s earnings multiple of 30 (using the index as a proxy for tech stocks). Analysts are expecting the company’s earnings to increase at 21.5% for the next five years, which could send its bottom line to $13.74 per share in 2028.

If TSMC trades at 30 times earnings at that time, its stock price could increase to $412, a jump of 182% from current levels. Investors can expect the stock to deliver even more gains over the longer run, and it may even help them become millionaires when bought as a part of a diversified portfolio.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Nvidia, Palantir Technologies, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and Lowe’s Companies and recommends the following options: long January 2025 $45 calls on Intel and short May 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.