Here’s why Nvidia and Taiwan Semiconductor look poised to continue their strong runs.

With 2024 starting to wind down, it appears it is going to be a very good year for the stock market, with the S&P 500 up about 24% year to date as of this writing. Tech stocks, in particular, have had a good run, with many benefiting from the advent of artificial intelligence (AI).

Two standouts this year in the semiconductor space have been Nvidia (NVDA -4.18%) and Taiwan Semiconductor Manufacturing (TSM -2.63%), or TSMC for short. But despite the strong performances of these two stocks, it looks like they have a lot of upside still ahead.

Let’s look at why Nvidia and TSMC look like no-brainer buys, even after their recent run-ups.

1. Nvidia

Nvidia has unquestionably been the biggest winner of the AI infrastructure build out, as its graphic processing units (GPUs) have become the backbone of the computing power needed to train large language models (LLMs). As cloud computing companies, AI start-ups, and other tech leaders have rushed to advance their AI models, there has been an insatiable appetite for Nvidia’s AI chips.

This has led to astonishing revenue growth for the company this year, with revenue up a whopping 135% year over year through the first nine months of its fiscal year. Its earnings per share (EPS), meanwhile, have nearly tripled over this same period.

And while its growth this past year has been outstanding, there is reason to believe Nvidia will continue to grow strongly into the future. Customer demand remains strong, and as their AI models advance, they will need exponentially more computing power, which comes from Nvidia’s GPUs.

For example, Meta Platforms has said its Llama 4 LLM would need 10 times the compute power as its Llama 3 LLM, while xAI’s Grok-3 AI model was trained using 100,000 GPUs versus Grok-2, which used 20,000 GPUs. Meanwhile, Nvidia’s largest customers have generally indicated that their capital expenditure (capex) spending will rise next year as they chase the once-in-a-lifetime opportunity of AI.

In addition to the AI training opportunities the company is seeing, Nvidia is also seeing a big pickup in its GPUs being used for AI inference, while it is also seeing increasing enterprise and industrial usage as well, marking another avenue of growth for the company. And while Nvidia is not the only company that makes GPUs, its CUDA software platform long ago became the standard upon which developers learned to program GPUs, creating a wide moat for the company. This is a large part of the reason why the company has such a dominant position in the market today.

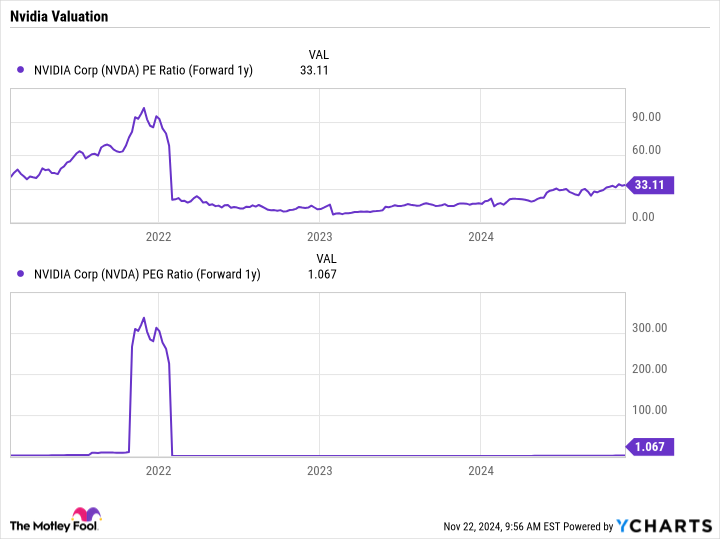

Meanwhile, despite the stock’s huge gains over the past few years, the stock remains attractively valued, with a forward price-to-earnings (P/E) of 33 times next year’s analyst estimates and a price/earnings-to-growth (PEG) ratio of just over 1. A PEG ratio of under 1 is usually viewed as undervalued, but growth stocks will often have multiples well above 1.

NVDA PE Ratio (Forward 1y) data by YCharts

Between the growth opportunities still in front of it, its wide moat, and attractive valuation, Nvidia stock is a great option for investors moving forward.

Image source: Getty Images.

2. Taiwan Semiconductor

Another chip stock riding the AI wave is TSMC, the world’s largest semiconductor contract manufacturing company. TSMC makes the chips that semiconductor companies design, and it counts Apple and Nvidia among its largest customers.

And while TSMC is not the world’s only semiconductor contract manufacturer, like Nvidia, it too has been able to create a wide moat. It has done this through its advanced technology and scale advantages. This has led the company to thrive, which can be seen in the 36% increase in revenue the company saw in Q3 and 50% jump in earnings per ADR (this is similar to EPS). This can be contrasted with Intel’s third-party foundry business, which has been drowning in losses and saw revenue decline last quarter.

The company is benefiting from the huge demand coming from AI chips, and is also set to benefit from any increased chip demand coming from a hardware and smartphone upgrade cycle, as more powerful devices are needed to run AI.

TSMC has also seen strong pricing power, which has been pushing up its gross margins. Meanwhile, according to Morgan Stanley, the company has already told customers that it will raise prices in 2025, including by 10% for AI semiconductors.

Also, similar to Nvidia, TSMC is attractively valued despite the run-up in its stock price. It trades at a forward P/E of about 21.5x based on next year’s analyst estimates, with a PEG of about 1.1.

TSM PE Ratio (Forward 1y) data by YCharts

Given the huge demand for semiconductors, combined with TSMC’s improving gross margins and pricing power, not to mention its attractive valuation, this is a strong option for investors to consider at current levels.

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, Intel, Meta Platforms, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends the following options: short February 2025 $27 calls on Intel. The Motley Fool has a disclosure policy.