While many analysts and investors will be looking at revenue and profit growth, two other figures are more important to me right now.

Semiconductor darling Nvidia (NVDA -0.84%) is set to report fiscal 2025 third-quarter earnings on Nov. 20. While there will be a lot to digest from the report, there are two items in particular that I will be on the lookout for.

Let’s explore what I’m most curious about as Nvidia earnings loom, and what I think these factors could mean for investors.

1. How’s the $50 billion buyback progressing?

Through the first half of Nvidia’s fiscal 2025, the company repurchased 162.1 million shares of common stock for $15.1 billion. Under its remaining share repurchase program, Nvidia is authorized to buy back an additional $7.5 billion of stock.

However, in addition to the $7.5 billion referenced above, Nvidia announced in August that its board of directors approved another $50 billion of buybacks.

On the surface, Nvidia increasing its share buyback program could be viewed as a bullish sign for investors. Generally speaking, companies buy back stock when management believes shares are undervalued. In this particular case, I’m very curious to see how much of the $50 billion authorization has actually gone to repurchases.

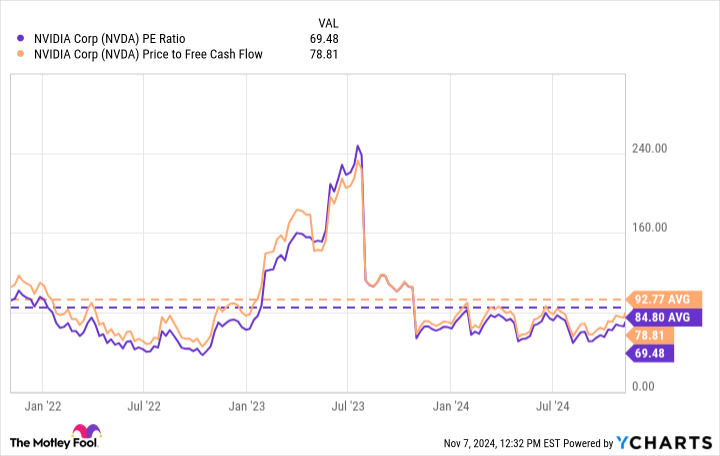

Data by YCharts.

Based on the past two years, Nvidia stock trades below its average price-to-earnings (P/E) and price-to-free cash flow (P/FCF) multiples as of this writing.

Since the company’s new Blackwell GPU is shaping up to be a massively successful product launch, there’s reason to believe Nvidia stock is poised to break out. Such a move would come with valuation expansion and, therefore, a more pricey stock.

For these reasons, I’ll be looking closely to see if the company repurchased any stock during the fiscal third quarter at more reasonable valuations, prior to any Blackwell-driven tailwinds. If this is not the case, I can’t help but feel the $50 billion buyback is a bit of a PR stunt — or as Motley Fool contributor Sean Williams eloquently put it, a “smoke-and-mirrors campaign.“

2. Blackwell, Blackwell, Blackwell

The hype surrounding Nvidia’s new Blackwell GPU is very real. CEO Jensen Huang has said that demand for Blackwell is “insane,” while Morgan Stanley analysts are projecting the product launch could yield $10 billion in revenue in fiscal 2025 alone.

While the Blackwell storyline has been shaping up to be nice and rosy, there could be a bit of a hiccup looming in the background. IT infrastructure company Super Micro Computer specializes in sophisticated chip architecture and storage clusters for data centers. One of the company’s closest partners is Nvidia, making it well-positioned to benefit from the upcoming Blackwell launch. Well, actually, maybe not.

Over the last several months, Supermicro has been at the center of a scandal that was kicked off by a short report from Hindenburg Research, which accused the company of accounting violations. Most recently, it was dropped by its auditor, Ernst & Young. In the midst of the drama, Nvidia is reported to be moving Blackwell orders away from Supermicro in lieu of other vendors.

While I see this as a prudent move on behalf of Nvidia’s management, it’s hard to know how this will affect supply-and-demand dynamics in the short term. As a result, Supermicro’s woes could very well permeate into some near-term headwinds for Nvidia’s growth.

Image source: Getty Images.

The bottom line

To be clear, I’m not going to run for the hills if Nvidia hasn’t started putting a dent in its new $50 billion buyback, or if Blackwell’s growth winds up being more protracted than originally anticipated in the short term.

Nvidia stock has been on quite a tear over the last couple of years, and that trend is likely going to continue over the next year or so thanks to tailwinds driven by Blackwell. Since that could make Nvidia stock even more expensive, it’s natural to wonder when and at what price range management might consider buying back stock a sound financial move.