These Nasdaq-100 constituents look set to deliver more gains thanks to the growing demand for their AI hardware.

The Nasdaq-100 index is up 10% so far in 2024, and that’s not surprising since it has benefited from the solid growth reported by its major constituents, which are benefiting from the increasing demand for artificial intelligence (AI) and cloud computing.

The good part is that the Nasdaq-100 could keep heading higher as the year progresses. Deutsche Bank estimates that the index could rise 19% in 2024 based on cooling inflation and solid economic growth in the U.S. Meanwhile, the proliferation of AI is likely to remain a top driver for technology stocks in 2024, and it could play a central role in boosting the Nasdaq-100.

Let’s take a closer look at two Nasdaq-100 components — Nvidia (NVDA -0.09%) and Qualcomm (QCOM -1.35%) — that are delivering outstanding results from AI adoption. We’ll see why it makes sense to buy these two AI stocks before the Nasdaq clocks more gains.

1. Nvidia

Nvidia’s stunning 121% gains in 2024 have played a central role in sending the Nasdaq-100 higher. And the stock’s outstanding rally seems to be here to stay. Analysts have been increasing their earnings expectations for the chipmaker following its latest quarterly report.

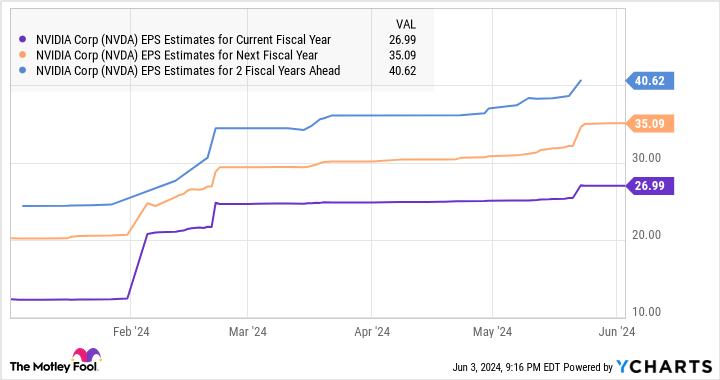

Over the past 30 days, 47 analysts have bumped up their earnings per share (EPS) estimate for fiscal 2025, while 44 have done the same for fiscal 2026. The improving EPS expectations from Nvidia are captured in the following chart.

NVDA EPS estimates for current fiscal year; data by YCharts.

There are two reasons analysts expect Nvidia to deliver stronger earnings. First, the company has been able to maintain its stranglehold over the AI chip market. It ended 2023 with a 94% share of the AI server market. As a result, its revenue from sales of data center chips shot up a remarkable 427% year over year in the first quarter of fiscal 2025 (which ended on April 28) to a record $22.6 billion.

Nvidia’s peers such as AMD and Intel reported data center revenue of $2.3 billion and $3 billion, respectively, in the first quarter of 2024. More importantly, Nvidia can sustain its dominance in the AI chip market with the arrival of a new generation of chips that could widen the technology gap it enjoys over rivals. Its upcoming chips based on the Blackwell architecture are touted to be four times faster than the current chips based on the Hopper architecture.

Nvidia points out that the demand for its Blackwell chips is so strong that it will have difficulty meeting it going into 2025. So the company’s AI lead seems here to stay, and that should allow it to ship more units of its AI graphics cards.

The second reason analysts are upbeat about Nvidia’s bottom-line growth is because of its immense pricing power in AI chips. According to Raymond James, it might cost Nvidia $6,000 to manufacture one Blackwell B200 accelerator. Since each processor is expected to be sold for $30,000 to $40,000, it stands to make a hefty profit on its new chips.

In all, the secular growth of the market for AI chips is going to be a big tailwind for Nvidia because of the reasons discussed above, which is why there is a good chance that this AI stock could soar further following the outstanding gains that it has already clocked in 2024.

2. Qualcomm

Qualcomm has achieved impressive momentum in 2024 with 41% gains so far, and this Nasdaq-100 stock seems built for more upside because of AI-related tailwinds in the smartphone and personal computer (PC) markets that seem set to drive a turnaround in its fortunes.

Qualcomm’s revenue in fiscal 2023 (which ended in September last year) fell 19% to $35.8 billion. Its adjusted earnings also fell 33% to $8.43 per share.

However, revenue in the first six months of fiscal 2024 has increased 3% year over year to $19.3 billion. It also reported a 13% year-over-year hike in adjusted earnings to $2.44 per share in the second quarter of fiscal 2024.

Analysts are expecting Qualcomm’s revenue to increase 7% in the current fiscal year to $38.3 billion, while earnings are forecast to jump 18% to $9.91 per share. More importantly, as the following chart indicates, Qualcomm is expected to deliver growth over the next couple of fiscal years as well.

QCOM revenue estimates for next fiscal year: data by YCharts.

But there is a good chance that Qualcomm’s growth could be stronger than expected because the demand for AI-enabled smartphones is set to take off, and Qualcomm is expected to be a key beneficiary of this market.

Counterpoint Research predicts that a total of 1 billion AI-enabled smartphones could be shipped between 2024 and 2027. The researcher expects Qualcomm’s chips to power more than 80% of generative-AI enabled smartphones over the next couple of years, not surprising because its chips are already powering Samsung‘s flagship AI-enabled Galaxy smartphones.

Moreover, Qualcomm’s strategy of deploying AI in midrange smartphones could help it remain the top player in this market in the long run. At the same time, the company has started making headway in the market for AI-enabled PCs as well. Microsoft recently announced new AI personal computers powered by Qualcomm chips.

The company said that all leading PC original equipment manufacturers are set to launch AI PCs powered by its Snapdragon chips very soon. This is likely to open another solid opportunity for Qualcomm as shipments are forecast to increase at an annual rate of 44% through 2028, according to Canalys.

All this indicates that Qualcomm’s growth could eventually accelerate, which is why it would be a good idea to buy the stock while it is trading at just 20 times forward earnings, a discount to the Nasdaq-100’s forward earnings multiple of 27.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Microsoft, Nvidia, and Qualcomm. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel, long January 2026 $395 calls on Microsoft, short August 2024 $35 calls on Intel, and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.