Artificial intelligence is set to power each of these stocks moving forward.

Tech stocks led the market in the first half of 2024, and there is no reason they can’t continue leading the market into the future. Artificial intelligence (AI) appears to be a game changer that should help power the sector higher in the years to come.

Let’s look at three tech stocks to buy this year and beyond.

1. Nvidia

No company has benefited more from the increased interest in AI than Nvidia (NVDA -6.62%), whose graphic processing units (GPUs) are being used to harness the power of AI in the data center. The company has created a stranglehold on the GPU market through its Compute Unified Device Architecture (CUDA) software platform that long ago became the industry standard for programming GPUs before AI became the next big thing.

With developers trained on its software platform, it has become difficult for other chipmakers to make a dent in Nvidia’s dominance, and there does not appear to be anything on the horizon to challenge its market-leading position. At the same time, the company sped up its innovation cycle to further widen its lead, looking to push out new GPU architecture platforms almost every year.

The company’s growth has been nothing short of spectacular, with its first-quarter revenue soaring 262% year over year to $26 billion. While that level of growth is unsustainable, demand for many of its chips outstrips supply, and customers are still in the early days of building out their AI infrastructures. This should continue to lead to strong growth in the years to come.

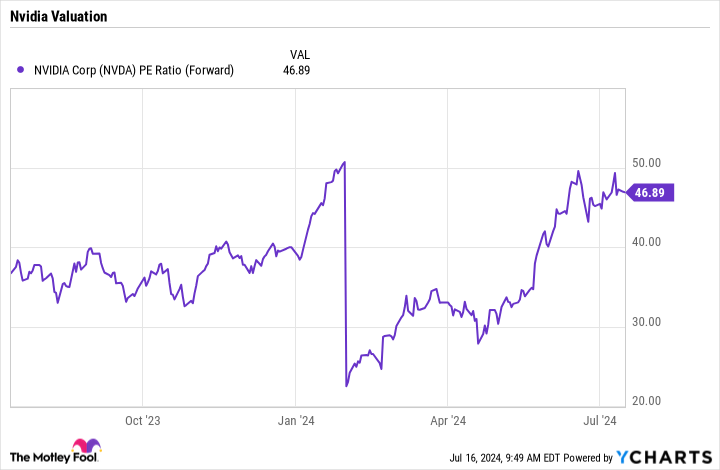

At the same time, given its growth, the stock is reasonably priced at a forward price-to-earnings (P/E) ratio of under 47 times.

NVDA PE Ratio (Forward) data by YCharts. PE = price to earnings.

2. Microsoft

While Nvidia has been at the forefront of AI on the chip side, Microsoft (MSFT -1.33%) has been the AI leader on the cloud computing and software side. Through its partnership with and investment in OpenAI, Microsoft has incorporated AI throughout its various offerings.

Its Azure cloud-computing business has been the biggest beneficiary of AI thus far, as shown by the segment’s revenue jumping 31% year over year last quarter. This is a pay-as-you-go business where customers pay only for the resources they use, and that usage has been soaring as clients use the Azure platform to build their own AI solutions. The company has seen deals getting bigger, with Azure deals worth more than $10 million last quarter doubling and $100 million-plus deals up 80%.

Meanwhile, Microsoft’s introduction of AI assistant Copilots is helping power other parts of its business as well. Its GitHub Copilot, which can make suggestions to help complete coding, helped power a 45% increase in revenue for its developer platform GitHub segment. The company is also using AI in its Microsoft 365 and LinkedIn offerings, which helped drive 14% and 29% year-over-year revenue growth, respectively, in each segment last quarter.

Trading at a forward P/E of under 34 times, the stock’s valuation is consistent with where it has traded over the past five years. Given the growth potential from AI in front of it, this is a solid stock to buy at current levels.

MSFT PE Ratio (Forward) data by YCharts. PE = price to earnings.

3. DocuSign

While Nvidia and Microsoft have been early AI leaders, DocuSign (DOCU -1.26%) has the potential to be a later AI beneficiary. The company known for its e-signature solution has witnessed its growth slow as it saw a lot of pull forward in demand due to the COVID-19 pandemic and then saw one of its biggest end markets, residential real estate, come under pressure.

However, this company has a cash-rich balance sheet and generates a lot of free cash flow. At the same time, with its new Intelligent Agreement Management (IAM) solution, it is looking to combine its e-signature and contract lifecycle management (CLM) products to become a platform company.

It will also begin incorporating AI technology into its new IAM platform, which it obtained from its recent acquisition of AI-powered agreement-management software company Lexion. The company has already introduced a number of new features to be included in IAM, such as Maestro, which can create agreements without coding, and Navigator, which can store and analyze a customer’s agreement databases.

DOCU PE Ratio (Forward) data by YCharts. PE = price to earnings. EV = enterprise value.

Trading at a forward P/E ratio under 18 and an enterprise value-to-EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of under 12, the stock is attractively valued, given its leading position in the e-signature market and potential growth drivers with its new IAM solution.