The tech and e-commerce giant has delivered solid growth over the past year, but it has plenty of room left to run.

Amazon (AMZN -2.33%) has become a stock to watch, pulling off an impressive turnaround after the tech sector downturn that affected a raft of growth stocks in 2022. The company’s share price plunged 50% during that challenging year, but has more than recovered with a 123% gain since Jan. 1, 2023. From the start of 2022 to today, it’s now up by about 17%.

The retail giant has benefited from a series of cost-cutting measures and easing inflation. Amazon’s growing cash reserves have allowed it to invest heavily in expanding industries like artificial intelligence (AI) and digital advertising.

The company is on a promising growth path that makes its stock too good to pass up right now. Meanwhile, its price-to-sales ratio of about 3 indicates it remains a bargain compared to some of its competitors.

Here are three reasons to buy Amazon stock like there’s no tomorrow.

1. Stellar retail growth

Rises in the cost of living forced millions of consumers to cut back on their discretionary spending in 2022, and the interest rate hikes that the Federal Reserve enacted to fight that inflation set off declines across the stock market. That year, Amazon’s e-commerce profits plummeted. However, its retail growth over the last year has shown that Amazon was able to successfully navigate the economic headwinds, and reflects the reliability of its business over the long term.

Despite its expansions into other industries, Amazon’s retail-focused segments make up more than 80% of its net sales. As a result, recent growth in its North America and international divisions has significantly boosted its overall earnings.

In the first quarter, Amazon’s revenue increased by 13% year over year to $143 billion, beating Wall Street’s consensus estimate by $750 million. The company’s North America and international segments posted revenue growth of 12% and 10%, respectively, during the quarter.

However, the most impressive result was on the operating income metric. In Q1, Amazon’s North America and international segments delivered a combined $6 billion in operating income, a significant improvement from their $349 million in total losses in the prior-year period.

2. A budding digital advertising business

This year, Amazon ventured into the streaming advertising market when it introduced ads on its Prime Video platform. And only six months later, the move is driving revenue.

In Q1, revenue from the advertising services segment spiked 25% year over year. This budding business could boost the company’s top line for years.

A forecast from market research firm Statista projects that the digital advertising market will hit $740 billion this year, and it’s continuing to grow. Meanwhile, the massive audience on Prime Video allows Amazon to price ads on the platform competitively. Amazon is charging between $30 and $35 per 1,000 impressions. For reference, Netflix was charging up to $45 per 1,000 impressions on its ad-supported tier, but recently lowered its prices to align with Amazon’s. Smaller streaming platforms could have difficulty offering advertisers similar rates.

In Q1, Prime Video had a leading 22% market share in video streaming, ahead of Netflix (21%) and No. 3 player Warner Bros. Discovery‘s Max (14%). As a result, the company could have a lucrative future in advertising, further diversifying its business model.

3. Amazon has the cash to flourish in AI

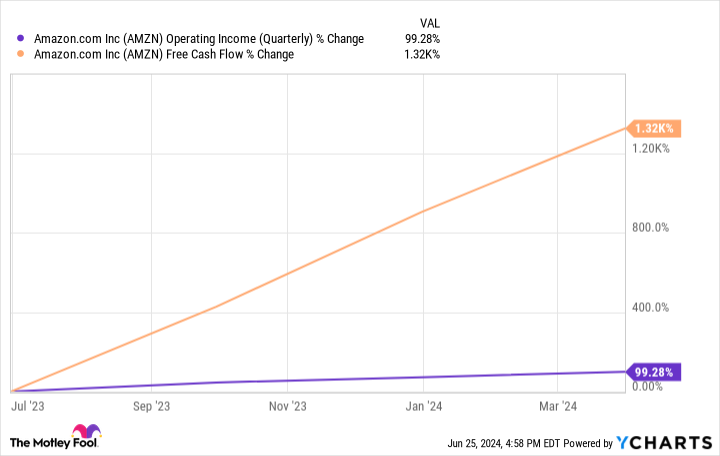

Data by YCharts.

Amazon’s operating income and free cash flow have skyrocketed over the last year thanks to significant gains both in its e-commerce segments and its cloud business, Amazon Web Services (AWS). In Q1, AWS’ operating income nearly doubled year over year to $9 billion. That amounted to more than 60% of the company’s total operating income, even though AWS brings in the lowest portion of its revenue.

With its renewed profits, Amazon has gone all in on AI. Cloud platforms are a crucial growth area in AI as companies increasingly turn to cloud services in hopes of boosting their productivity with AI technology. And AWS has a competitive edge with a leading 31% market share in cloud infrastructure.

Amazon has added a range of AI tools to AWS this year, invested billions into building data centers worldwide, and ventured into chip design to create its own AI processors as it seeks to expand its position in that high-growth market.

Amazon’s stock has risen by 95% over the last five years. However, given its growth catalysts in multiple markets, it could do even better over the next half-decade, particularly in light of its current low price-to-sales ratio. As such, Amazon is a stock to buy like there’s no tomorrow.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Dani Cook has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Netflix, and Warner Bros. Discovery. The Motley Fool has a disclosure policy.