The e-commerce software company is living up to all the hype — and then some.

Are you looking for a new stock pick to capitalize on the market’s newfound strength? Consider stepping into a stake in Shopify (SHOP -0.54%). It’s a right place/right time kind of prospect… something all investors were reminded of Tuesday. Fortunately, it’s not too late to jump in.

What’s Shopify?

On the off-chance you’re reading this and don’t know, Shopify helps businesses of all sizes establish and operate an e-commerce presence. From online shopping carts to payment processing to inventory management tools to marketing support (and more), Shopify can offer almost anything. It monetizes its technology on a subscription basis, as well as on a per-transaction basis.

To fully appreciate the power and potential of Shopify, however, you must understand the “why” of its existence. In simplest terms, it’s the un-Amazon, offering an alternative means of selling online to merchants that don’t want to be beholden to North America’s biggest online mall.

Amazon wasn’t always seen in this frustrating light. In its early days, sellers loved the reach it could provide. As could have been predicted, though, the platform became very crowded. Amazon itself also began competing head-to-head with many of its merchants.

That’s why many merchants and brands are increasingly exploring alternative online-selling options. Lots of them are choosing Shopify. Not only does this choice ultimately cost sellers less, it also allows these users to forge their own direct relationships with consumers. Although the company no longer discloses a specific number of merchants utilizing its services, most estimates put the figure in the ballpark of between 2 million and 4 million.

Regardless of the estimated number of paying sellers, Shopify does disclose some telling fiscal metrics. During its recently ended quarter, for instance, the company facilitated the sale of $69.7 billion worth of merchandise, turning that into nearly $2.2 billion worth of revenue for itself. Both figures are well up from year-earlier comparisons. That’s a small part of the first of three reasons you might want to scoop up a piece of this company sooner than later, in fact.

Its story is interesting, to be sure. But so were the stories behind Groupon, GoPro, and Blue Apron. Mere premises don’t pay the proverbial (and actual) bills. What makes Shopify a must-have investment here and now? Three reasons stand out among several.

1. It’s growing — reliably

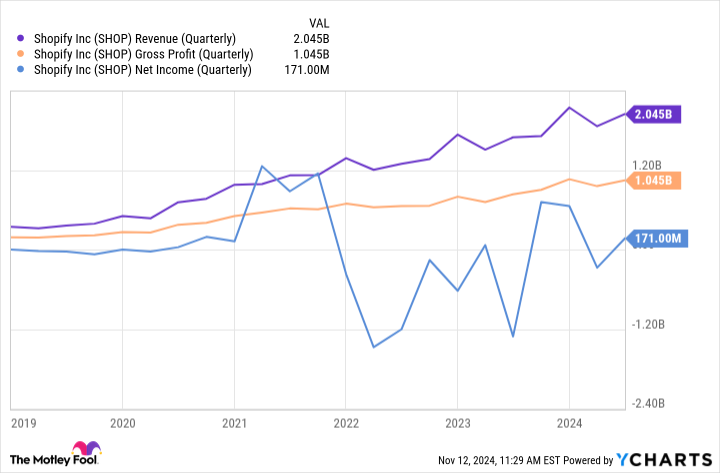

As noted, last quarter’s top line was up — and to no small degree. Revenue improved 26% year over year, more than doubling the company’s operating income, and boosting free cash flow from $276 million during the third quarter of last year to $421 million for the three-month stretch ending in September of this year. That’s impressive, given the lethargic economic environment and tepid consumerism.

SHOP Revenue (Quarterly) data by YCharts

Making this performance even more impressive is the fact that last quarter was the sixth consecutive one that revenue grew more than 25% (not factoring in the company’s recently sold logistics business).

2. Shopify’s service is precisely what merchants need right now

There’s a reason this company is doing the seemingly unthinkable: The options that Shopify offers merchants, brands, and independent sellers are exactly what they want — and need — at this point in time.

In e-commerce’s infancy, platforms like Amazon’s and eBay‘s met a need that most would-be sellers couldn’t satisfy on their own. The online shopping arena evolved, though. Thanks to the passage of time along the advent of social media and the continued refinement of web marketing tools, the lines between entertainment and commerce and information have been blurred. Most brands can now find their own customers rather than relying on a third party to handle this heavy lifting.

The only thing these merchants need is a means of turning web traffic into a transaction. That’s where Shopify shines.

3. The opportunity is enormous

The thing is, as much as the online marketplace may have evolved since its early days, there’s still plenty of growth opportunity ahead.

It seems almost unbelievable, given the known size of the e-commerce market, but the U.S. Census Bureau reports that only about 16% of the United States’ retail sales are made online. The other 84% of them are still done in-store. The worldwide numbers are in the same ballpark. Although there are some retail sales that will never be made online, a huge chunk of current brick-and-mortar sales could still become e-commerce business.

In this vein, market research outfit Straits Research predicts the global e-commerce software market is set to grow at an annualized pace of over 12% through 2032. Shopify is positioned to capture much of this growth, particularly now that it’s turning up the heat on its overseas and international efforts.

Be smart, but not stubborn

Anyone reading this likely already knows that Shopify shares soared on Tuesday in response to its impressive third-quarter report and encouraging guidance. Specifically, the company expects “revenues to grow at a mid-to-high-twenties percentage rate,” pushing gross profits up by a similar degree.

Problem? The post-earnings jump was so strong that it leaves shares uncomfortably vulnerable to profit-taking pressure. It wouldn’t be wrong to let the rally cool a bit and let this stock find its footing around its new price.

Just don’t linger on the sidelines too long. This stock isn’t exactly a stranger to such moves. Several similar jumps have been logged since shares began to recover back in the middle of 2022. None of them have proven too problematic to let the long-term rally reignite.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and Shopify. The Motley Fool recommends eBay. The Motley Fool has a disclosure policy.