Nvidia won’t be the leader in AI forever.

Nvidia has been the king of the first wave of artificial intelligence (AI) investing. Its graphics processing units (GPUs) are being purchased by the truckload by the biggest cloud computing and AI modeling companies. Eventually, if they have all the computing power they want, Nvidia’s business would decline as new computing capacity wouldn’t be needed.

This will give way to the next wave of AI investments, and if you’re looking to cash in on this trend, I’ve got three companies that are slated to do well.

Cloud computing is going to grow tremendously

The next wave will benefit companies currently training and developing AI models or those offering cloud computing services to companies developing AI. The major cloud computing players are Amazon (AMZN 0.91%), Microsoft (MSFT -0.78%), and Alphabet (GOOG 0.86%) (GOOGL 0.89%). As the industry leaders, they have been some of the largest purchasers of Nvidia’s GPUs in recent quarters.

All three also have affiliations with generative AI models, with Amazon and Microsoft investing in and partnering with Anthropic and Open AI, respectively. Alphabet is developing its generative AI model, Gemini, in-house. With all three companies having strong ties to top-tier generative AI models, they have properly positioned themselves to provide users with the tools they need to create AI models.

However, having a generative AI model for cloud computing clients is just table stakes for a much larger game. Many workloads are still processed on-site at businesses around the globe. While some of these workloads may never migrate to the cloud, a large majority will. This is why the cloud computing market opportunity is expected to increase from $676 billion in 2024 to $2.3 trillion by 2032, according to Fortune Business Insights.

Because it is easy to scale up or down the computing power you rent in the cloud, it is ideal for training in-house AI models, as businesses don’t have to buy expensive computing power from companies like Nvidia permanently. With the general trend toward the cloud being accelerated by AI demand, it’s clear this will be a huge investment trend.

But does that make all three stocks buys?

All three stocks have unique price points

The wrinkle with each of these companies is that cloud computing isn’t the only thing they do. While cloud computing continues to be one of the best (if not the best) performing segments in each of these businesses, other core businesses steer the stocks. Additionally, the prices you must pay for the stocks vary widely.

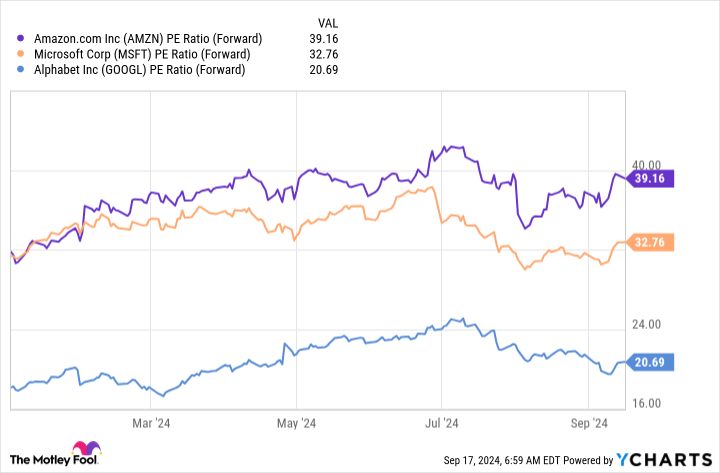

AMZN PE Ratio (Forward) data by YCharts

Amazon is the most expensive, but that’s because it has the most potential in cloud computing. Amazon Web Services (AWS) is the market leader in cloud computing. But because Amazon’s ancillary businesses are all fairly low-margin, AWS accounts for 64% of its operating profit despite only contributing 18% of revenue. This means that if AWS sees brisk growth, Amazon’s profits will quickly rise, decreasing Amazon’s expensive valuation rapidly.

Although Amazon technically is more expensive from a forward price-to-earnings (P/E) ratio, I’d argue that Microsoft is the most expensive. Its business has steadily grown revenue, but its profit margins have remained relatively flat. As a result, there really isn’t any big upside for Microsoft; it must maintain its status quo to retain its premium price tag.

MSFT Revenue (Quarterly YoY Growth) data by YCharts

Last is Alphabet, which is actually cheaper than the broader market (measured by the S&P 500, which trades at 22.7 times forward earnings). Alphabet doesn’t have the premium valuation of its peers because it has been behind on several key product launches, but that doesn’t mean it can’t be a solid investment. Alphabet has much to gain from its cloud computing wing because it is just starting to turn profitable and could be a huge boost to profits as it moves toward AWS-like margins.

All three cloud computing businesses have merits, but Amazon and Alphabet stand out as better investment options than Microsoft right now, solely based on their potential to grow profits.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Alphabet and Amazon. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.