Nvidia’s stock has massive expectations built into it, but the company could easily attain those lofty goals.

Nvidia (NVDA -2.61%) has become the hottest stock on the market due to its incredible rise thanks to unprecedented demand for artificial intelligence (AI). With the stock recently up around 160% this year, its rise has made many investors a lot of money.

However, if you’re going to be an Nvidia investor, there are three things you must know that could affect your perspective on the stock.

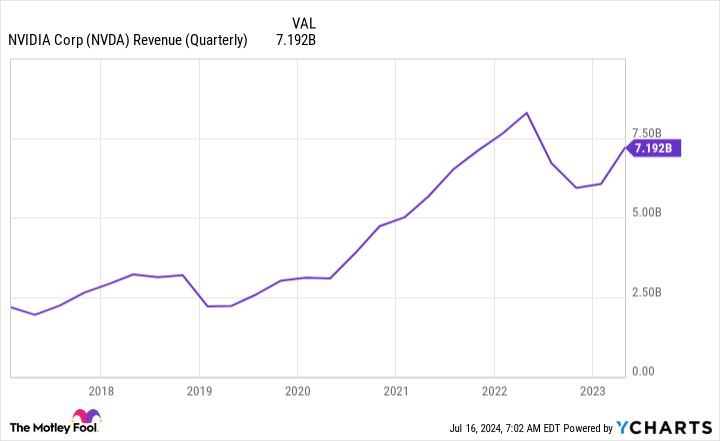

1. Nvidia is historically a cyclical company

Although Nvidia has some software products, it’s not a software company. Its primary product is its graphics processing units (GPUs), which enable its users to train AI models. Because GPUs can process multiple calculations in parallel, they are effective at complex computing tasks. Combine that with the ability to hook hundreds or thousands together, and it makes sense that Nvidia’s GPUs are flying off the shelf.

However, times aren’t always peachy at Nvidia.

The chip industry is known to be cyclical, as demand rises and falls based on a secondary trend. Nvidia’s last two cyclical cycles were tied to cryptocurrency, and the company saw significant revenue drawdowns after the cycle was complete.

NVDA Revenue (Quarterly) data by YCharts

However, Nvidia has always emerged a stronger company from its various cyclical drawdowns. This is key, as investors must weigh this success against the backdrop of another drawdown that is eventually coming.

Once AI computing demand is built out, Nvidia will undoubtedly see a drop in demand. The problem is, nobody knows if that’s in the next quarter, next year, or the next decade. If it doesn’t occur for a while, investing in Nvidia now could be smart. But investors could be in trouble if it’s right around the corner.

2. Nvidia’s valuation is incredibly high

After a run-up like Nvidia’s, it’s no surprise that the stock has a premium price tag attached to it. But just how expensive is it?

Because Nvidia is a mature company, using the price-to-earnings (P/E) ratio is a smart idea. Additionally, because Nvidia is experiencing significant change, the forward P/E ratio is also a useful metric, as the two combined show what expectations are built into the stock over the next 12 months.

NVDA PE Ratio data by YCharts

A valuation of 47 times forward earnings is incredibly expensive, especially considering the S&P 500 trades for around 22.7 times forward earnings. Because of Nvidia’s premium status and top-tier execution, seeing the stock trade at a 30 times earnings multiple when the pandemonium has settled down isn’t out of the question. But for Nvidia to reach that valuation, it must grow its earnings by 151%.

While some may think that’s easy, especially considering that Nvidia grew its earnings per share by 629% in Q1 of FY 2025 (ending April 28), it will start reaching quarters with tougher comparison figures. As a result, its growth rates won’t look as impressive, even though they will still be rapid.

Wall Street analysts expect Nvidia to grow its earnings by 60% over the next 12 months. So it’s not out of the question that the company must continue growing at its current pace for two years to return to a reasonable valuation.

That’s a long time of sustained strong growth. But is it realistic?

3. AI demand isn’t going away

Although it seems like all anyone has talked about is AI this and AI that, it’s because AI will be a life-altering product like the internet. Technology has barely scratched the surface of how AI can assist in daily tasks, and to power the next wave of innovation even more computing power will be needed.

Furthermore, a GPU used in a data center lasts around five years, so eventually it will need to be replaced. This will fuel another wave of demand for Nvidia’s GPUs, which could further extend Nvidia’s growth.

As an investor, Nvidia’s valuation scares me. But there is a case to be made that the stock could still be worth the price you’re paying today if the growth extends out for another few years.

If you keep that in mind, Nvidia stock may be for you. Otherwise, if you invest in an index fund, you’ll still have heavy Nvidia exposure because it makes up about 6.7% of the S&P 500.

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.