Amazon ain’t done growing yet.

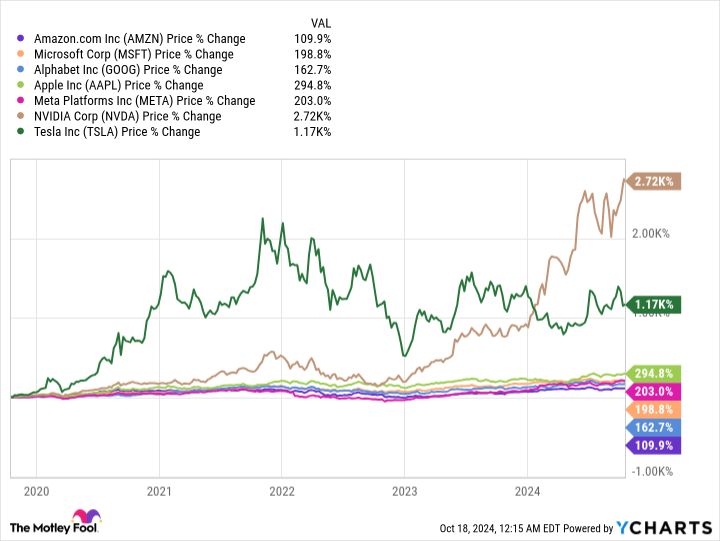

Of the Magnificent Seven stocks, you might be surprised to know that Amazon (AMZN 0.78%) has actually had the lowest returns over the past five years.

That’s pretty curious, especially since the Covid-19 pandemic solidified just how important Amazon’s e-commerce and cloud franchises are to consumers and businesses alike.

This is because the post-pandemic period reversed many of the positive trends Amazon experienced during the stay-at-home period. Add in the retirement of founder Jeff Bezos, and that has been a recipe for shareholder skepticism.

However, virtually all of Amazon’s businesses are now showing improving metrics, and more positive developments appear on the way. Here are five solid reasons to buy Amazon stock today.

1. AWS is reaccelerating

Last quarter, Amazon Web Services (AWS) saw revenue growth accelerate for the third consecutive quarter at 19%, while operating margins expanded along with that growth to a very healthy 35.5%, up from just 24.2% in the year ago-quarter.

AWS isn’t growing quite as fast as rivals, but that’s because of the law of large numbers as the largest cloud in the space. But at a $100 billion-plus revenue run-rate, a 19% growth rate is really impressive.

While some had thought Amazon had fallen behind rivals in artificial intelligence, AWS’s reacceleration and new product announcements indicate that’s not the case. While rival Microsoft has an exclusive relationship with early leader OpenAI, Amazon has invested in Anthropic, the company behind the impressive Claude large language models (LLMs) and run by OpenAI’s old head of research. Moreover, AWS is committed to the broadest range of generative AI options through its Bedrock platform.

It’s quite possible that LLMs become somewhat commoditized over time, but Amazon has always been great at taking competitive businesses and becoming a scaled low-cost provider. On that note, Amazon had the foresight to invest early in its own homegrown chips since 2015. Amazon’s in-house CPU processors called Graviton greatly lower costs versus x86 merchant solutions.

But the cost difference relative to third parties will be even more important in the age of AI, as training on Nvidia chips is massively expensive. Back in July, an Amazon executive noted its in-house AI Trainium and Inferentia chips are 40% to 50% cheaper than Nvidia’s on a price-performance basis. Given Amazon’s wide scale and early investment in low-cost chips, AWS should be quite competitive in the AI age.

2. E-commerce continues to get more efficient

Since last year, CEO Andy Jassy’s plan to make Amazon’s e-commerce operations more profitable has been a smashing success. Both North American and International operating margins have increased every quarter since the fourth quarter of 2022, thanks to Jassy’s implementation of a regional system that has lowered Amazon’s cost to deliver packages. Paid units delivered have outstripped growth in shipping costs every quarter since Q3 2022.

Investors have always been somewhat skeptical of Amazon’s e-commerce operations ever being profitable, but both the North American and International segments are now profitable, with steadily improving margins.

3. Advertising growth set to continue

One of the biggest bright spots for Amazon in the past few years has been the growth of its advertising business, which spans its retail site and Prime Video. Growing in the 20% range at a $50 billion annualized run-rate, Amazon’s ads business is now a serious digital ads player behind to Search, Facebook and Instagram.

But advertising should maintain its strong growth, with Amazon able to link its troves of customer data to better target ads to customers more likely to make a purchase. Moreover, the segment still has untapped opportunities. Prime Video doesn’t even show ads yet in several major international markets, but Amazon is now set to unleash digital video ads in India, Brazil, Japan, New Zealand and the Netherlands in 2025, which should add to growth.

As long as customers continue flocking to Amazon’s online stores and signing up for Prime, which seems likely, high-margin ads are likely to follow.

Image source: Getty Images.

4. New ventures

Just because Amazon is becoming more profitable doesn’t mean the company isn’t investing in new growth areas. These include expanding into grocery stores, healthcare, and perhaps most exciting, Project Kuiper, Amazon’s nascent satellite broadband offering.

Project Kuiper aims to rival SpaceX’s Starlink business. While the costs of launching satellites into orbit is expensive, as some estimate the initial cost will run Amazon some $20 billion, that high entry cost blocks out too much competition. Meanwhile, if successful, analysts estimate Kuiper could add tens of billion in profits to Amazon annually.

According to the company, Kuiper broadband services are set to become available sometime next year. That could be another catalyst for the stock in 2025.

5. More cost cuts on the way

On top of these positive growth prospects, CEO Andy Jassy announced last month that Amazon is embarking on an efficiency initiative through the end of this year. Jassy and his team now aim to get rid of layers of middle management by increasing the ratio of individuals to managers by 15%. Moreover, Jassy is asking employees to return to the office five days a week, after seeing the benefits over the last 15 months when employees were called back to the office at least three days a week.

The two initiatives appear related, as those who don’t wish to work five days a week may quit, thereby helping management with its cost-cutting decisions. If the initiative helps boost Amazon’s efficiency, as Jassy’s previous efficiency initiatives in e-commerce did, then shareholders should have even more profitable growth to look forward to.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Billy Duberstein and/or his clients have positions in Amazon and Microsoft. The Motley Fool has positions in and recommends Amazon, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.