The NASDAQ index has risen 24% year-to-date and is hovering near record highs following a summer lull. Once again, the rally has been powered largely by the ‘Magnificent 7’ – a select group of mega-cap tech stocks that have soared to stratospheric valuations in recent years.

This group includes the six largest stocks trading on Wall Street – Apple, Nvidia, Microsoft, Alphabet, Amazon, and Meta – as well as Elon Musk’s Tesla. Together, these companies have been leaders in innovation, especially of the AI tech that is so rapidly changing the tech world.

Pivotal Research analyst Jeffrey Wlodarczak has been closely examining the ‘Magnificent 7’ and is now offering fresh recommendations on Amazon (NASDAQ:AMZN) and Alphabet (NASDAQ:GOOGL). Let’s take a closer look at what makes these two stand out and why they are receiving Wlodarczak’s endorsement.

Amazon

We’ll start with Amazon, the global leader in online retail. This company is a proven survivor, an original ‘dot.com’ that survived the tech bubble of the late 90s–early 2000s and has grown to become one of the world’s largest publicly traded firms. While the company started out as an online bookseller, today e-shoppers can find virtually anything on Amazon – and the company will guarantee delivery almost anywhere in the world.

Amazon backs up its huge inventory, covering everything from books and toys to pharmaceuticals, clothing, and phone cases, with a network of high-tech warehouses and logistics facilities. The company’s warehouses use AI and robotic tech, backed up by a human workforce, to pack and ship anything to anywhere.

This combination of huge inventory and fast delivery has made Amazon the world leader in e-commerce – and allowed the company to build up an enormous market cap of nearly $2 trillion, making Amazon the world’s fifth-largest public company. Amazon has used its deep pockets to expand its customer base by expanding its product and service offerings.

On the product side, Amazon has recently been pushing its ‘digital pharmacy’ business, allowing customers to fill prescriptions online, with fully accredited pharmacists. Earlier this month, the company announced that it will be opening 20 new pharmacies, doubling the number of cities with same-day delivery service available.

On the service side, the company’s cloud computing platform, AWS, has become increasingly popular. AWS, which is a direct competitor to Google Cloud and Microsoft’s Azure, has become an important revenue driver for Amazon – and accounted for $26.3 billion of the company’s $148 billion topline in Q2 of this year (the last quarter reported). That makes AWS responsible for almost 18% of the total revenue in a quarter that saw 10% year-over-year revenue growth. Amazon has been consistently reporting year-over-year quarterly revenue growth in the low double digits recently and is expected to do so again in the upcoming Q3 report. The top line for the third quarter is expected to exceed $157 billion, which would translate to another 10% year-over-year gain.

For analyst Wlodarczak, Amazon presents a solid tale of strength and growth. He writes of the company, “Amazon has a deep moat around their core businesses driven by their unmatched scale and has what appears to be the largest organic revenue growth opportunity of any mega cap tech company (other than arguably NVDA (N/R)) driven primarily by their AWS cloud segment (which we expect to grow from 17% of revenue to ~35% in 5 years), extension of their e-commerce/fulfillment arms into new segments/internationally, continued rapid growth in their advertising business and proven ability to develop new successful products/revenue streams.”

Looking ahead, Wlodarczak goes on to explain why investors should continue to buy in on AMZN: “This is all enhanced by what we believe is the highest potential of their peers to materially boost operating margins driven by scale, leveraging robotics/AI and benefits from an increasing % of revenue from high margin cloud computing/advertising combined with what appears to be an attractive valuation.”

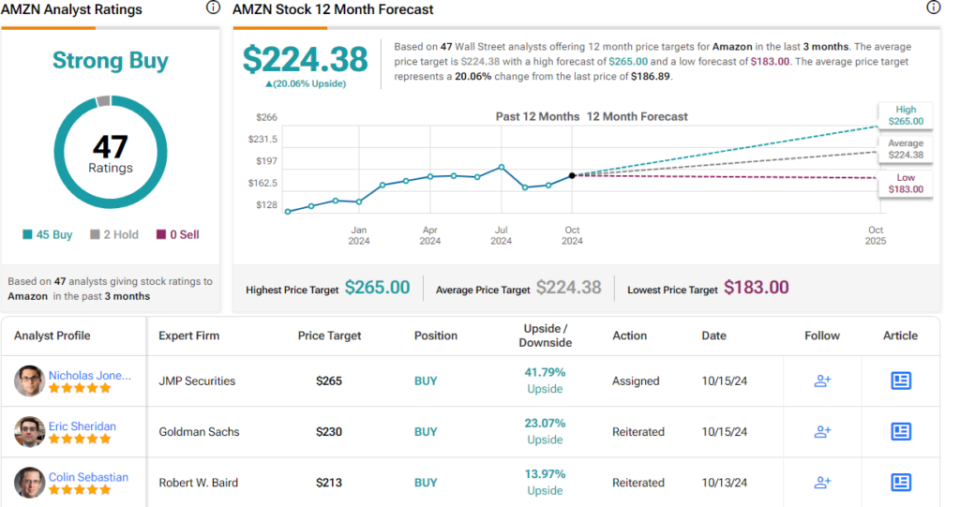

As expected, after comments like these, Wlodarczak rates Amazon stock as a Buy. His price target, set at $260, points toward a one-year upside potential of 39%. (To watch Wlodarczak’s track record, click here)

This major retailer/tech firm has picked up plenty of attention from Wall Street, and mostly all positive. The Strong Buy consensus is based on a lopsided Buy/Hold split of 45 to 2 among the analyst reviews, and the $224.38 average price target implies a 20% upside from the current trading price of $186.89. (See Amazon stock forecast)

Alphabet

The second Mag 7 stock we’ll look at is Alphabet, the parent company of Google, and the market’s fourth-largest public company, with a market cap of just over $2 trillion. Alphabet, which also owns YouTube and has been developing an ever-growing presence in the AI field, has built its success on its absolute dominance of the global internet search segment – and the advantages that brings in the field of digital advertising. Remember that Google and YouTube are the world’s leaders in online search and online video search, respectively.

In the last few years, the AI boom has begun to shift the tech landscape in ways that are still not fully clear. Alphabet has been moving to adopt the new technology, seeing it as a multiplier for online search, and as a powerful tool in online and cloud-based applications. The company is using AI tech in its multimodal large language models, which improve both Google’s online translation apps and its search engine functionality. These improvements in generating search results and translation matrixes are a direct response to increased competition from Microsoft’s Bing as well as ChatGPT and other generative AI platforms.

On the practical side, Alphabet has released its Gemini platform, its most up-to-date offering in AI. Gemini is based on a core of large language models, designed from the start to understand natural language content – in text, audio, images, video, and even in code. The platform uses AI to provide the maximum flexibility for the end user’s application, and Alphabet is working to integrate it into all of its products. That includes the Android operating system, which will make Gemini’s AI available on smartphones – and all of their apps. For Alphabet, the key challenge presented by AI will be maintaining market share in online search as the digital world switches its base to generative AI tools and apps.

For now, Alphabet is generating solid revenue and income numbers. The company brought in $84.7 billion in 2Q24, a total that was up nearly 14% from the prior-year quarter and was more than $445 million over the forecast. Alphabet’s bottom line of $1.89 per share was 5 cents over expectations. Analysts are expecting to see revenues of $86.23 billion when the company reports earnings for Q3 later this month.

Turning again to Pivotal’s Wlodarczak, we find the analyst taking an upbeat view of Alphabet’s stock, its position and prospects. He says, “If the status quo holds, GOOG appears to be in a very strong competitive position with a deep moat around their dominant core search business model (~90% market share ex China) and an obvious path to leverage 90%+ (ex China) global device presence (which we believe will dominate consumer AI assistant use), a strong AI platform and financial might to increase financial incentives to handset manufacturers for default AI placement. GOOG also holds a strong #3 position in cloud computing, which we believe has dramatic growth potential…”

Looking ahead, Wlodarczak adds, “This position is enhanced by the fact that GOOG appears to have the ability, leveraging their AI investment, to significantly reduce their cost structure (mainly through a material reduction in their ~180K employees) offset partially by the aforementioned potentially higher TAC to extend their search handset dominance to AI (if they are not prohibited in doing so by regulators/courts), which should help drive strong financial growth and help them generate a reasonable AI ROIC even if the development of AI revenue generating applications takes longer than expected.”

It should come as no surprise that the Pivotal analyst rates GOOGL shares as a Buy, while his price target, $215, suggests an upside of 30% on the one-year horizon.

For the Street generally, this is another stock with a Strong Buy consensus. The 39 recent reviews include 30 Buys to 9 Holds. Shares are priced at $165.16 and have an average target price of $201.57, implying a gain of 22% by this time next year. (See Alphabet stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.