This buy now, pay later company is growing nicely and could benefit from tailwinds that could make it profitable in the near future.

As consumers grapple with rising credit card debt balances and elevated interest rates, recent interest rate cuts from the Federal Reserve offer hope for more affordable borrowing costs.

Leading the charge in this space is Affirm (AFRM -4.81%), a standout in the buy now, pay later (BNPL) industry. With its expansion of partnerships and growing market presence, Affirm has grown nicely amid an uncertain economic environment over the past couple of years. The company has also demonstrated resilience, with its consumer credit portfolio holding strong.

BNPL continues to grow in popularity, and lower interest rates could spur more demand for these loan options, and analysts are taking notice. Recently, Affirm has enjoyed a wave of upgrades and price target raises from banks, including the following:

- Wedbush upgraded it to neutral with a price target of $45.

- Wells Fargo upgraded it to overweight with a price target of $52.

- Morgan Stanley upgraded to equal-weight with a price target of $37.

- BTIG Research upgraded it to buy with a price target of $68.

- Susquehanna maintained a positive rating and raised its price target to $57.

- JPMorgan maintained its buy rating and raised its price target to $56.

Here’s what has analysts so bullish on Affirm and what you need to know if you’re considering adding the stock to your investment portfolio today.

Affirm’s strategic partnerships have supported its strong growth

Affirm has benefited from growing demand for BNPL and important partnerships with large e-commerce providers. Last year, it partnered with Amazon Pay to become the first BNPL provider to offer payment options through the retail giant; this partnership also includes Amazon’s business-to-business stores.

In August, the company announced a partnership with Hotels.com, where guests can book accommodations and pay over time. This builds further on Affirm’s partnerships with travel providers, including Expedia and its subsidiary, Vrbo. Its product was also recently integrated into Apple Pay, enabling customers to access its flexible payment plans through their iPhone or iPad.

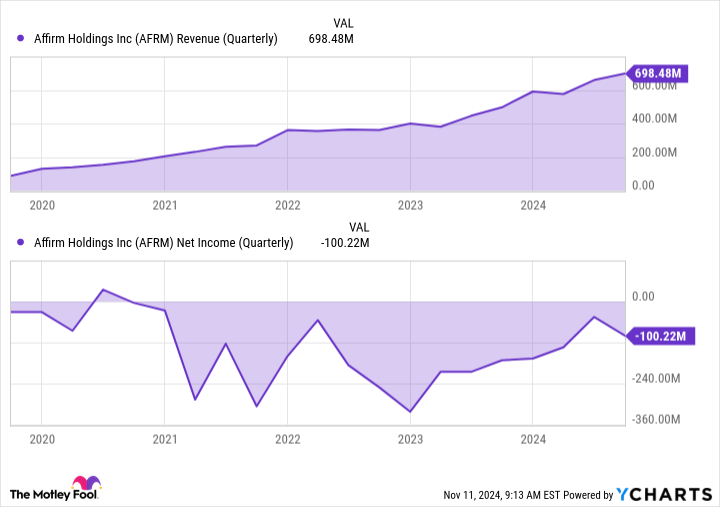

Its gross merchandise volume (GMV) grew 35% from last year, reaching $7.6 billion. Its revenue was $698 million, growing 41% from last year. Its operating expenses also increased, although not as quickly as its revenue; its net loss in the quarter of $100 million was an improvement from last year when it lost $171 million.

AFRM Revenue (Quarterly) data by YCharts

In the company’s letter to shareholders, it estimates that the U.S. BNPL GMV as a percentage of U.S. e-commerce was around 7.4%, up about one percentage point from a year ago. Affirm estimates that it represents around 34% of the BNPL market, which has been helped by those partnerships noted above.

What’s next for Affirm?

One area where investors have expressed caution is Affirm’s credit quality. However, it has held up quite well. In its first quarter (ended Sept. 30), 30+ day delinquencies of 2.8% were slightly higher from 2.4% in the prior quarter. However, these metrics have been relatively stable, and Affirm credits it to the shorter-term nature of its loans.

Affirm’s credit quality has held up, and top-line growth has been solid. Now, the company could benefit from the Federal Reserve lowering interest rates. The central bank has shown confidence that inflation is getting closer to its target and has dropped the federal funds rate, its benchmark interest rate, by 0.75% since its September meeting.

Lower funding costs could be a good thing for consumer lenders across the board. For Affirm, lower funding costs could encourage more borrowers to utilize its product. That, coupled with its more frequent appearance as a payment option on Apple and popular e-commerce sites, could help spur more demand for its installment loans.

Image source: Getty Images.

Is Affirm a buy today?

Despite its solid growth, Affirm continues to lose money. However, analysts think its growth and tailwinds from lower rates could help push it to profitability. According to Wells Fargo analysts, Affirm has “clearly demonstrated its right to win incremental e-commerce checkout share for years to come,” and that profitability is “on the horizon.”

The company’s credit quality has held up quite well, and it continues to display solid growth thanks to its partnerships and the growing popularity of BNPL options. With the stock priced at 5.7 times sales and 4.7 times next year’s projected sales, I think Affirm is a good buy for investors who don’t mind tolerating a little risk.

Wells Fargo is an advertising partner of Motley Fool Money. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. JPMorgan Chase is an advertising partner of Motley Fool Money. Courtney Carlsen has positions in Apple and Morgan Stanley. The Motley Fool has positions in and recommends Amazon, Apple, and JPMorgan Chase. The Motley Fool has a disclosure policy.