The stock has been a massive winner for investors over the past 10 years. Is it simply too late to buy?

There’s no denying that investing in Nvidia (NVDA 9.32%) stock has been a boon to long-term shareholders. The stock has gained nearly 23,000% since 2014, and its growth has recently accelerated. Shares are up 112% so far this year (as of this writing), nearly 10 times the gains of the S&P 500, adding to its relentless run.

Several catalysts have conspired to send the stock higher over the past decade. Nvidia’s graphics processing units (GPUs) have long been the gold standard for serious gamers. However, Nvidia adapted its high-end chips to speed data through the ether to become the go-to for data centers and cloud computing. GPUs have also proven their mettle at handling artificial intelligence (AI), and adoption is spreading like wildfire, igniting the stock’s recent rally.

What does this mean for investors who have been on the sidelines during Nvidia’s blistering run? Is there additional upside for this market darling, or has that train already left the station? Let’s examine the evidence.

Image source: The Motley Fool.

A long track record of performance

Without further investigation, it might be easy to conclude that you’ve already missed your chance with Nvidia, but investors have been making that same mistake for years. One of the keys to the company’s continuing success is the ability to find new and innovative ways to adapt its technology. Nvidia’s earlier work with machine learning and other branches of AI set the stage for the company’s current success with the explosive demand for generative AI.

Nvidia’s secret sauce is its mastery of parallel processing, or the ability to run a multitude of mathematical computations simultaneously. The company pioneered this technology to generate lifelike images in video games, but it proved equally adept at data center and cloud computing applications and possessed the raw computational horsepower required for the rigors of AI.

More relevant to the question at hand is that these markets all have potential upside, which could drive Nvidia stock even higher.

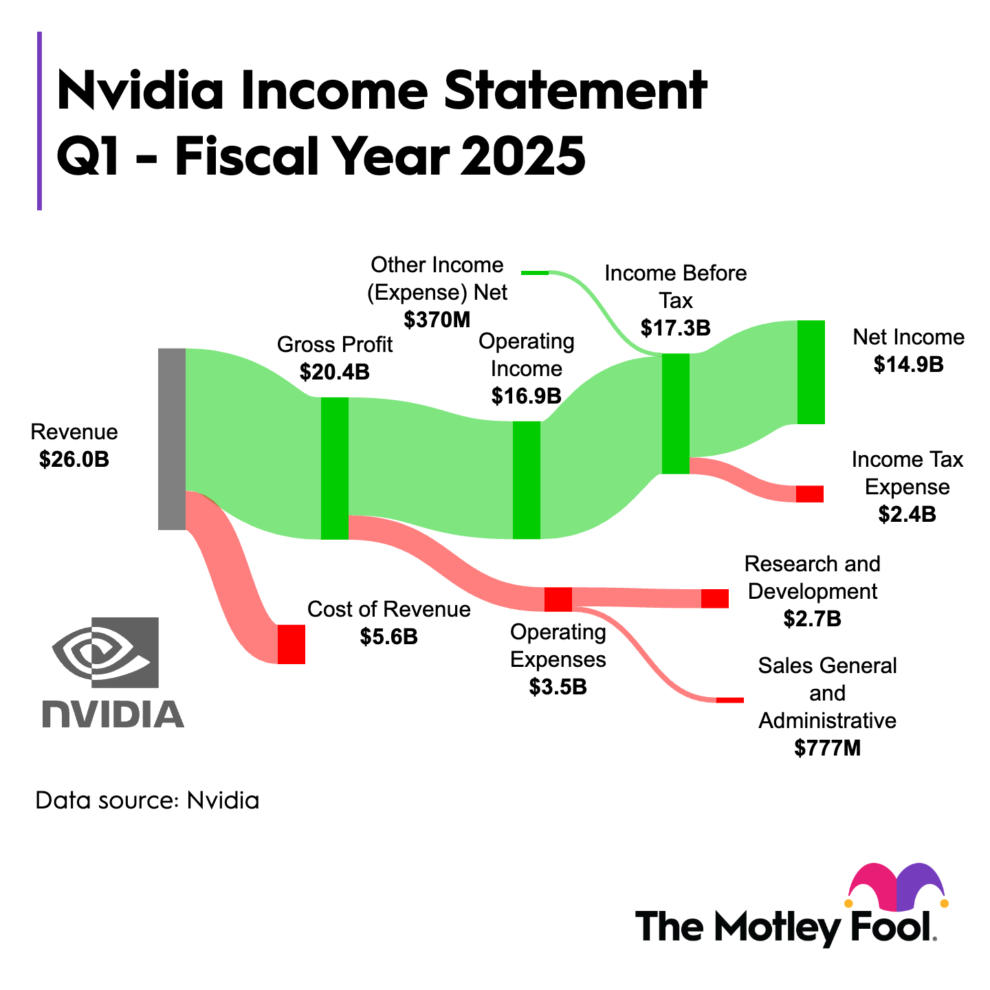

The company’s recent financial report provides plenty of evidence to support that contention. In its fiscal 2025 first quarter (ended April 28), Nvidia generated record quarterly revenue of $26 billion, up 262% year over year. The results were primarily driven by its data center segment, including AI, which produced record revenue of $22.6 billion, up 427%. The bounty continued to the bottom line, as diluted earnings per share (EPS) of $5.98 soared 629%.

For investors worried that the rally is on its last legs, Nvidia’s outlook should dispel concerns. For the second quarter, management is forecasting record revenue of $28 billion, which would represent year-over-year growth of 107%. Management even announced a stock split to make the skyrocketing share price more affordable. While investors shouldn’t expect those triple-digit increases to continue, this clearly shows that Nvidia’s growth is far from over.

More room to run

Nvidia’s two biggest opportunities are generative AI and data centers.

The adoption of generative AI, while robust, is still in the early stages. Estimates vary wildly regarding the opportunity, but one of the more conservative takes suggests the generative AI market will grow to between $2.6 trillion and $4.4 trillion in the coming years, according to global management consulting firm McKinsey & Company. As the leading provider of processors used for AI, Nvidia stands to benefit from this secular tailwind.

Furthermore, the data center industry is in the midst of one of the biggest upgrade cycles ever. Bank of America analyst Ruplu Bhattacharya estimates that the market will grow at a compound annual rate of 50% over the next three years. Nvidia controls an estimated 92% share of the market for GPUs used in data centers, which suggests a long and lucrative road ahead.

These two markets should continue to fuel Nvidia’s growth. This helps illustrate the vast opportunity ahead and why it isn’t too late to buy Nvidia stock, even at a new, all-time high.

What about the valuation?

There’s no denying Nvidia’s steep valuation. It’s currently selling for 89 times earnings — but that requires context.

The company has already generated four consecutive quarters of triple-digit growth and is guiding for another. The forward-looking numbers are much more reasonable, as Nvidia has a forward price-to-earnings (P/E) ratio of 39, though it’s still higher than the multiple of 27 for the S&P 500.

But while the valuation might seem unreasonable at first glance, this really isn’t an apples-to-apples comparison. As noted, Nvidia has outperformed the S&P by a factor of 10 over the past decade, so it’s earned that premium valuation.

Considering its track record of performance, its dominant place within the industry, and the magnitude of the opportunity ahead, it’s easy to understand why Nvidia stock is still a buy.

Bank of America is an advertising partner of The Ascent, a Motley Fool company. Danny Vena has positions in Nvidia. The Motley Fool has positions in and recommends Bank of America and Nvidia. The Motley Fool has a disclosure policy.