It’s been easy to hate banks as investments — not only were some of the biggest players bailed out by taxpayers in 2008, but bank stocks and the financial sector more generally have underperformed the broader market for years.

But over the past three months, the financial sector has turned from laggard to leader, rising 5.9%, versus a 3.5% advance for the S&P 500 index SPX, +0.29% , making it the best-performing S&P sector since the start of April, according to FactSet. From the beginning of 2018 through March of this year, the S&P 500 had risen 6%, versus a 7.9% decline for the financial sector.

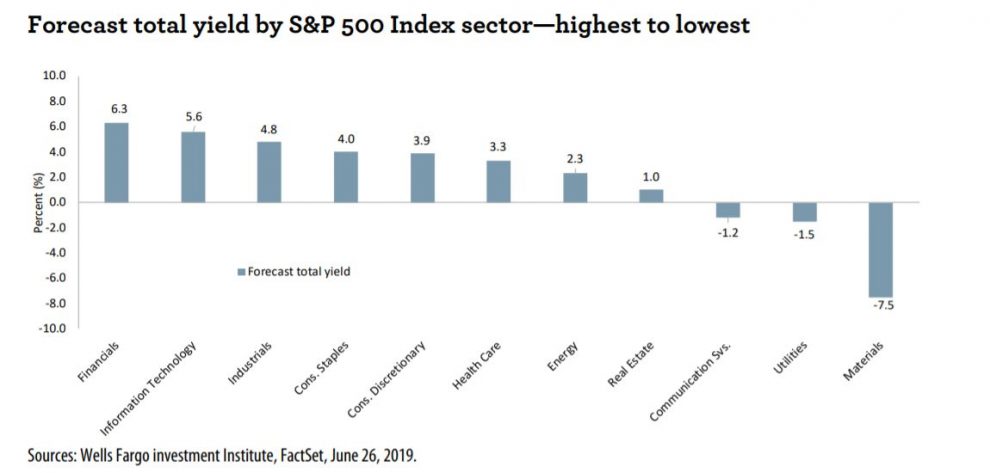

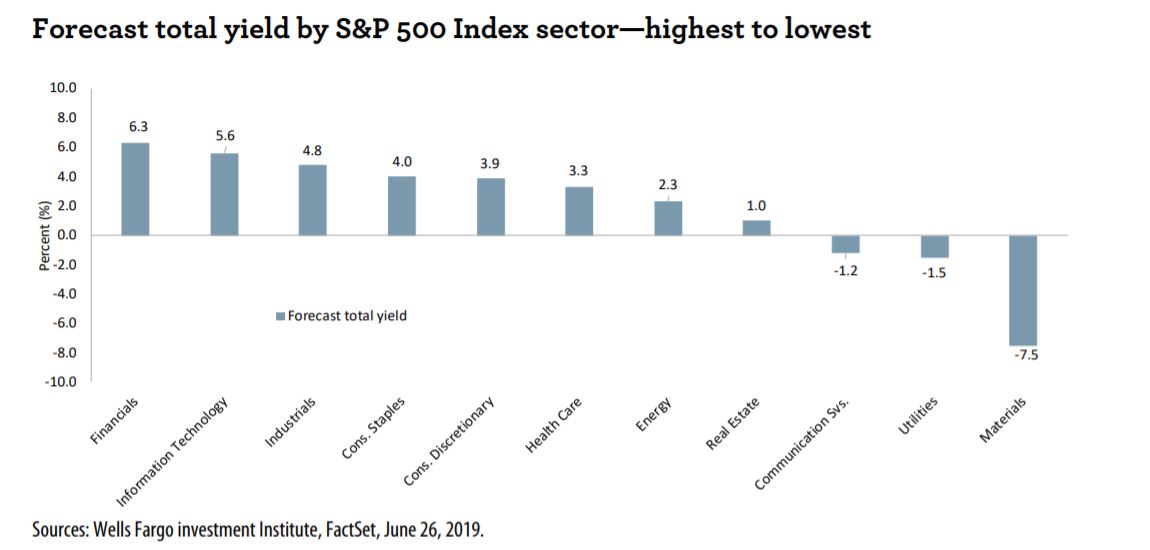

Scott Wren, senior global equity strategist at Wells Fargo, wrote in a Tuesday research note that financial stocks should continue to outperform the broader market. “The financials sector offers the most attractive forecast total yield over the next 12 months, compared to the other S&P 500 sectors,” he wrote, noting that this measurement includes both dividends and buybacks. “This is a particularly attractive feature in the current low-rate environment, in which the major stock indices are at (or near) what we consider to be ‘fair value.’”

Wells Fargo Investment Institute

Wells Fargo Investment Institute

Yields on government bonds and other fixed-income investments have fallen far enough that nearly half of S&P 500 stocks are expected to yield more income from dividends than the current yield of 1.98% for 10-year U.S. Treasury notes TMUBMUSD10Y, -1.08% making the stocks attractive investments even if you assume those stocks won’t appreciate in price.

Within the broader financial sector, Opppenheimer analyst Chris Kotowski is particularly bullish on large banks, writing in a note to clients that “the breadth, stability and quality of [large banks’] earnings has never been better,” even if the market has shown much greater love to other sectors during the current bull market. He pointed out that:

“In the past 12 months Citigroup Inc. C, -0.42% — perhaps the most despised name in a despised group — earned roughly as much as Mastercard Inc. MA, +1.42% and Visa Inc. V, +0.77% combined,” But it has only 24.6% of their combined market cap.

Bank of America Corp. BAC, -0.92% “earned more than Amazon Inc. AMZN, +0.63% Paypal Holdings Inc. PYPL, +0.99% Booking Holdings Inc. BKNG, +0.50% , Netflix Inc. NFLX, +0.22% , Salesforce.com Inc. CRM, +0.04% , Intuit Inc. INTU, +0.81% and Automatic Data Processing Inc. ADP, -2.66% combined. It has just 17.7% of their valuation.

Those are incredible numbers. Obviously investors place much higher value on companies that are seen as innovators and increasing their revenue rapidly, but these figures put into context the relative cheapness of bank stocks, with steady and stable earnings and plans to deploy excess capital through dividends and share buybacks.

FactSEt

FactSEt

“Among the 100 largest-market-cap stocks in the S&P 500, the big banks and investment banks account for 16.1% of the dollars of net income earned but just 7.6% of the market capitalization,” Kotowski wrote.

Fears that bank stocks will become a “value trap” that depreciates in value on negative sentiment, despite solid fundaments, are not warranted because earnings per share of the largest American banks are expected to “grow in the 6% to 9% range,” while these banks can use their hefty earnings to repurchase shares, which will support stock prices and return capital to shareholders in the form of dividends, he added.

Last week, the Federal Reserve approved capital plans by the nations’ top nine banks to pay out nearly $40 billion in dividends and to buy back $121 billion in stock, Kotowski wrote.

The relative success of the banking industry of late is particularly interesting in the context of falling interest rates, as the conventional wisdom is that lower rates make it difficult for banks to make money, as the spread between their own funding costs, and what interest they must pay to borrowers narrows.

But large banks have diversified sources of revenue, such as wealth management and investment banking services that can help buoy these companies fortunes. Not so for smaller banks, wrote Steven Alexopoulos, U.S. mid- and small-cap analyst for J.P. Morgan, in a Tuesday research note.

Regional banks “are at an unusual juncture,” when costs for attracting deposits are rising, while they are earning less on the loans they make because of the inversion of the yield curve, whereby short-term borrowing costs as measured by the three-year Treasury bill TMUBMUSD03M, -0.71% are higher than longer-term ones, as measured by the 10-year Treasury note.

The divergent fortunes of regional banks and large-cap institutions can be seen in their performance, with the SPDR S&P Regional Banking ETF KRE, -1.47% down 0.1% in the three months when the large-cap financial sector staged its turnaround, while falling 13.5% over the past 12 months.

Here are dividend yields and projected earnings-per-share increases, based on consensus estimates among analysts polled by FactSet, for the largest 10 U.S. banks by total assets:

| Bank Holding Company | Ticker | Total assets ($bil) | Dividend yield | Projected EPS change – 2019 | Projected EPS change – 2020 | Projected EPS change – 2021 |

| JPMorgan Chase & Co. | JPM, +0.11% | $2,737 | 2.81% | 11% | 6% | 7% |

| Bank of America Corp. | BAC, -0.92% | $2,377 | 2.04% | 9% | 10% | 8% |

| Citigroup Inc. | C, -0.42% | $1,958 | 2.54% | 13% | 14% | 10% |

| Wells Fargo & Co. | WFC, -0.96% | $1,888 | 3.77% | 10% | 8% | 9% |

| Goldman Sachs Group Inc. | GS, -0.43% | $925 | 1.64% | -9% | 9% | 7% |

| Morgan Stanley | MS, -0.27% | $876 | 2.73% | 4% | 9% | 9% |

| U.S. Bancorp | USB, -0.15% | $476 | 2.79% | 3% | 5% | 6% |

| PNC Financial Services Group Inc. | PNC, -0.15% | $393 | 2.72% | 6% | 7% | 7% |

| Capital One Financial Corp. | COF, -1.02% | $373 | 1.74% | -5% | 7% | 10% |

| Bank of New York Mellon Corp. | BK, -0.54% | $346 | 2.52% | -1% | 9% | 3% |

| Source: FactSet | ||||||