These membership retailers have their fair share of unique strengths, but one stands out more than the other as a stock to buy today.

Chances are, if you’re an American, you have a membership to either Amazon (AMZN 1.50%), Costco Wholesale (COST 0.33%), or both. Each retailer has generated tremendous long-term gains for its shareholders, with Amazon dominating the online marketplace and Costco thriving with its network of wholesale warehouses.

But which stock is the better buy right now? Let’s dive into their latest financial results, balance sheets, and future growth opportunities to find out.

The top and bottom lines

For the first category, let’s look at two essential financial metrics for any company: net sales and free cash flow.

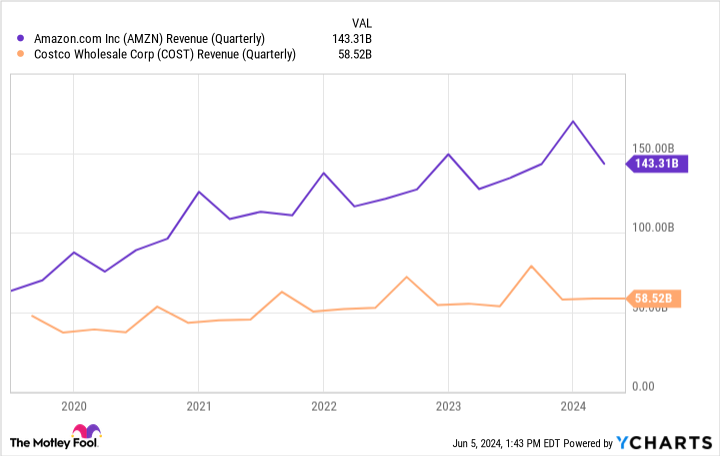

Amazon generated $143.3 billion in net sales for the first quarter of 2024, compared to $127.4 billion in the year-ago period, an increase of 12.5%. Looking ahead at Amazon’s second quarter of 2024, management guided for net sales between $144 billion and $149 billion, or an increase between 7% and 11%.

Comparatively, Costco recently reported net sales of $57.4 billion during its fiscal third quarter of 2024, which represented a year-over-year increase of 9.1%. It’s important to note that sales were positively affected by a shift in the company’s fiscal calendar by approximately 0.5% to 1%. While Costco’s management doesn’t have forward-looking revenue guidance, the company does release its monthly net sales results ahead of earnings reports, which totaled $19.64 billion for the retail month of May, a year-over-year increase of 8.1% from $18.16 billion.

AMZN Revenue (Quarterly) data by YCharts

Turning our attention to each company’s profitability, Amazon generated $46.1 billion in free cash flow over the trailing 12 months, a significant improvement from -$10.1 billion for the trailing 12 months ended March 31, 2023. For comparison, Costco generated $7.4 billion in free cash over the trailing 12 months, a 10% improvement compared to the trailing 12 months ended May 7, 2023.

AMZN Free Cash Flow data by YCharts

Overall, Costco’s recent financials are solid and stable; however, Amazon wins in this category as the stock’s revenue and profitability growth are more impressive.

Financial health and returning capital to shareholders

At a time when interest rates are relatively high, both Amazon and Costco can avoid snowballing debt due to high interest expenses. Instead, the companies can operate from a position of strength and, for Costco, return capital to shareholders through dividends, which allows shareholders to either reinvest their money into the company or collect cash for themselves.

Costco currently pays a regular quarterly dividend of $1.16 per share, equating to an annual yield of 0.6%, which may not impress income-seeking investors on the surface. However, the company is known for paying a frequent special cash dividend — five over the past 11 years — with the most recent coming in January 2024.

Amazon does not currently pay a dividend and is unlikely to follow other tech giants like Alphabet and Meta Platforms, which recently announced its plans to issue dividends for the first time. During Amazon’s most recent earnings call, CFO Brian Olsavsky stated that the company had no news to share regarding dividends. He emphasized that management’s top priority is to invest in growth opportunities and long-term initiatives. These investments focus on generative artificial intelligence (AI), expected to drive capital investments in 2024 higher than the previous year’s $48.4 billion.

So, despite Amazon’s slightly stronger cash position, this category goes to Costco due to its consistent track record of returning capital to shareholders and the high likelihood that it will continue to do so.

AMZN Net Financial Debt (Quarterly) data by YCharts

Growth opportunities

While both stocks have long outperformed, prospective buyers should focus more on each company’s future growth opportunities.

As hinted, Amazon sees its next growth phase in generative AI, with plans to implement it across nearly every sector of the company. One division already benefiting is Amazon Web Services (AWS), which helps businesses build AI products and services. As a result, AWS’ growth rate is “accelerating” to a projected $100 billion annual revenue run rate, up from $90.8 billion in 2023.

While the AI market is in its infancy, Statista, a global data and business intelligence platform, predicts exponential growth. Specifically, Statista puts the AI market at $184 billion in 2024, with an expected annual growth rate of 28.5%, resulting in a market volume of $827 billion by 2030.

Comparatively, Costco has two major growth drivers: international expansion and increasing membership fees. At the end of fiscal Q3 2024, the company had 876 locations, with 752 in North America. Management aims to open 25 to 30 net new locations each year, with the most potential for expansion in China. Since opening its first Chinese warehouse in 2019, Costco’s membership levels have soared to roughly 200,000 as of its fiscal second quarter of 2024 and it recently opened a seventh location. Notably, Amazon shuttered its online marketplace in China in 2019 and has yet to return.

When asked about raising membership prices during the company’s latest earnings call, Costco CFO Gary Millerchip stated it “is still a case of when we increase the fee rather than if we increase the fee.”

Overall, both companies are well positioned for future growth, and each is taking a different approach. Costco wants to grow slowly and steadily, while Amazon looks to expand at a breakneck speed. Given Costco’s safer growth, this category is a close call, but let’s award Amazon for the higher growth potential.

Is Amazon or Costco the better buy?

Amazon and Costco are exceptionally well-managed companies poised for long-term success and worthy of every investor’s portfolio. That said, at this moment, Amazon appears to be the better buy, especially when considering the valuation. Amazon trades at 42.8 times free cash flow, lower than its 10-year median of 62.9. For comparison, Costco currently trades at 50.5 times free cash flow and its 10-year median is 31.1 times free cash flow.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Collin Brantmeyer has positions in Amazon, Costco Wholesale, and Microsoft. The Motley Fool has positions in and recommends Amazon, Costco Wholesale, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.