These chip stocks are playing a key role in the proliferation of AI and are on track to enjoy robust long-term growth.

Shares of Nvidia (NVDA 0.69%) and Micron Technology (MU 1.82%) have delivered healthy gains on the stock market so far in 2024, though one of them has outperformed the other by a huge margin. While Nvidia stock’s year-to-date gains stand at a stunning 130%, Micron has clocked a relatively modest jump of 29%.

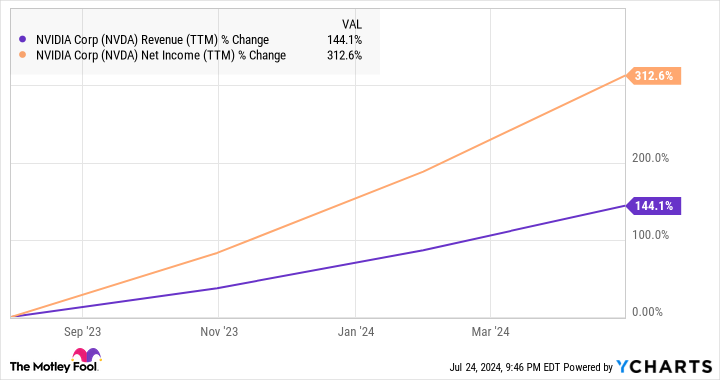

Nvidia’s revenue and earnings have been growing at a phenomenal pace in recent quarters thanks to its dominance in the artificial intelligence (AI) data center graphics card market. However, a closer look at Micron indicates that the memory specialist is witnessing a terrific turnaround in its fortunes thanks to AI.

So, if you had to choose one of these two AI stocks for your portfolio, which one should you be buying? Let’s find out.

The case for Nvidia

The AI chip market is seeing rapid growth as companies try to get their hands on powerful hardware to train and deploy AI models and services. According to one estimate, the market for AI chips could clock annual growth of almost 41% through 2032 and generate more than $1.1 trillion in revenue.

Nvidia is one of the best ways to capitalize on this massive end-market opportunity. The company has established a huge lead in the AI data center graphics processing unit (GPU) space with an estimated market share of more than 90%. This explains why Nvidia’s growth has been stunning in recent quarters.

NVDA Revenue (TTM) data by YCharts

More importantly, Nvidia’s AI-driven growth seems sustainable in the long run. That’s because the company wants to tighten its grip on AI-related niches beyond just hardware. For instance, Nvidia’s AI Foundry solution allows customers to build custom generative AI models for their use cases. This service is gaining traction among customers, with the likes of Accenture, Aramco, Uber, and others using the offering to develop AI applications.

Nvidia customers won’t need to invest in expensive hardware to develop their own AI models, as they can simply get down to developing and deploying applications. This could open a new growth opportunity for Nvidia as the demand for cloud-based AI services is estimated to be worth a massive $523 billion in 2031.

Meanwhile, governments are also adopting Nvidia’s AI solutions. The company is expecting $10 billion in government-related revenue this year. For comparison, its sovereign AI revenue was zero last year. Looking ahead, Nvidia’s government-related business could get bigger as nations accelerate spending on AI.

Given that Nvidia forecasts that its total addressable market stands at a massive $1 trillion, the company seems capable of sustaining its impressive growth in the long run. Investors who hold this growth stock in their portfolios would do well to continue holding it for the long run.

The case for Micron Technology

Though Micron Technology stock’s gains haven’t been as mindblowing as Nvidia’s in 2024, a closer look at Micron’s growth indicates that the market may be underestimating its AI-fueled growth potential.

In the third quarter of fiscal 2024 (ended on May 30), Micron reported a stunning year-over-year increase of 81% in revenue to $6.8 billion. AI played a central role in driving this outstanding growth with Micron’s high-bandwidth memory (HBM) chips being used by the likes of Nvidia in AI graphics cards.

Management remarked on the company’s recent earnings conference call:

Our HBM shipment ramp began in fiscal Q3, and we generated over $100 million in HBM3E revenue in the quarter, at margins accretive to DRAM and overall company margins. We expect to generate several hundred million dollars of revenue from HBM in fiscal 2024 and multiple billions of dollars in revenue from HBM in fiscal 2025.

Even better, the demand for Micron’s HBM chips is so strong that it has already sold out its production capacity for 2024 and 2025. More importantly, Micron is looking to push the envelope in the HBM market with more advanced chips that will not only be more powerful but also more power-efficient. That’s a smart thing to do as the HBM market could generate almost $86 billion in revenue in 2030 as compared to just $1.8 billion last year, clocking a compound annual growth rate of 68%.

So, Micron’s focus on maintaining its leadership in the HBM market could reap rich dividends in the long run and drive robust incremental revenue growth for the company. However, is Micron a better AI pick than Nvidia? Let’s find out.

The verdict

Both Nvidia and Micron are high-growth companies. However, one of them is available at a significantly cheaper valuation. While Micron is trading at 13 times forward earnings, Nvidia has a richer forward earnings multiple of 47.

Of course, Nvidia’s higher earnings multiple is justified thanks to its much faster growth, which is why growth-focused investors can still consider buying the stock. But those looking for a mix of growth and value may be tempted to buy Micron Technology as this AI stock could soar impressively because of its recent eye-popping growth.

As such, investors could choose either of these AI stocks for their portfolios or may even consider buying both. Nvidia and Micron are likely to remain key players that could drive the AI market’s growth for a long time to come.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Accenture Plc, Nvidia, and Uber Technologies. The Motley Fool recommends the following options: long January 2025 $290 calls on Accenture Plc and short January 2025 $310 calls on Accenture Plc. The Motley Fool has a disclosure policy.