The past two years have been absolutely stunning for semiconductor stocks, with the PHLX Semiconductor Sector index rising 81% during this period. Artificial intelligence (AI) played a central role in this remarkable surge.

Nvidia (NVDA -2.69%) was one of the biggest beneficiaries of this rally, gaining close to 702% in the past two years as companies and governments have been buying its AI chips hand over fist. The company on which Nvidia relies for manufacturing its AI chips has clocked relatively smaller gains of 142% in the last two years.

Taiwan Semiconductor Manufacturing (TSM -3.63%), popularly known as TSMC, is the world’s largest semiconductor foundry. Fabless chipmakers, such as Nvidia, which design their chips but don’t manufacture them, utilize TSMC’s fabs for manufacturing. However, there’s more to TSMC than just Nvidia.

Below, I’ll examine the prospects and the valuations of these two companies and check which one is the better semiconductor stock to buy right now following the remarkable gains in the past two years.

The case for Nvidia

The biggest reason to buy Nvidia stock right now is its dominant position in the AI chip market. It has built an almost monopoly-like position in AI chips, with some estimates putting its share at more than 90%.

This dominance explains why Nvidia’s rivals are nowhere near it when it comes to AI chip sales. For instance, it sold $27.6 billion worth of data center compute chips in the third quarter of fiscal 2025, an impressive increase of 132% from the same period last year. Rival Advanced Micro Devices, by comparison, is expecting to sell $5 billion worth of data center GPUs (graphics processing units) in 2024.

Nvidia’s revenue from AI GPU sales was more than 5x the amount AMD expects to generate from this segment for the entire year. On the other hand, Intel‘s data center and AI revenue in the previous quarter stood at $3.3 billion, up just 9% from the year-ago period. Nvidia, therefore, is leagues ahead of its rivals in the AI chip market.

That’s not surprising, considering Nvidia managed to corner a big chunk of TSMC’s advanced chip-packaging capacity. According to Taiwan-based daily DigiTimes, Nvidia reportedly secured 60% of TSMC’s Chip on Wafer on Substrate (CoWoS) packaging technology for 2025. DigiTimes also says that TSMC is planning to more than double its CoWoS capacity next year.

There’s a good chance Nvidia could deliver another year of stellar growth in 2025 because TSMC’s capacity expansion should ideally allow the company to fulfill more demand from customers. Reports indicate Nvidia may have sold out its Blackwell supply for almost the entirety of 2025. This is where TSMC’s increased production capacity should come in handy.

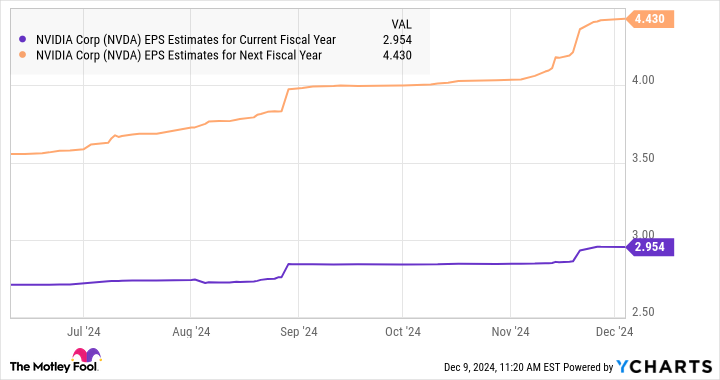

The good part is that Nvidia is going all out to significantly ramp up the production of its Blackwell processors, which is why its margins are going to remain a tad constrained in the short run. However, as the chart below shows, Nvidia remains on track to deliver a big jump in its bottom line in the next fiscal year (which will begin toward the end of January 2025).

NVDA Earnings-Per-Share (EPS) Estimates for Current Fiscal Year data by YCharts.

That estimate could keep moving higher as the production of its Blackwell processors ramps up and margin concerns ease, indicating that Nvidia could well be on its way to delivering another solid year in 2025.

The case for TSMC

TSMC stock may lag behind Nvidia as far as its performance on the market is concerned, but a closer look at the company’s business model tells us that it’s a more diversified semiconductor stock. As mentioned, fabless chipmakers turn to TSMC to get their chips manufactured, which means that it plays a bigger role in the AI chip market.

That’s because TSMC doesn’t only manufacture chips for GPU companies such as Nvidia, but it also produces custom chips for the likes of Broadcom and Marvell Technology, smartphone chips for Qualcomm and Apple, and central processing units (CPUs) and GPUs for AMD. This puts TSMC in a position to capitalize on multiple secular growth opportunities within the semiconductor space.

For instance, the demand for custom AI chips, or application-specific integrated circuits (ASICs), is expected to increase at an annual rate of 32% for the next six years. Broadcom and Marvell are the two players dominant in this market, and both of them have reportedly been placing more orders with TSMC to meet the rising demand.

On the other hand, the demand for generative AI-enabled smartphones and computers is going to be a catalyst for companies such as Qualcomm, Apple, and AMD. Qualcomm, for example, saw a jump in sales of its smartphone processors, and it’s expected to remain the dominant player in the generative AI market. Similarly, Apple’s smartphone sales are also picking up and should head higher next year.

Given that Apple is TSMC’s largest customer, the former’s solid position in the smartphone space puts it in a terrific place to make the most of the growth of the generative AI smartphone space. These catalysts are the reason why analysts expect TSMC’s earnings to increase by 36% this year, followed by impressive growth over the next couple of years, as well.

TSM EPS Estimates for Current Fiscal Year data by YCharts.

The verdict

Though TSMC looks like a more rounded semiconductor stock, considering the multiple verticals it serves, it can’t be denied that Nvidia is growing at a much faster pace. However, investors will have to pay a much richer multiple to buy Nvidia right now. This is evident from the following chart:

NVDA P/E Ratio data by YCharts.

Of course, investors with a higher risk appetite can consider buying Nvidia, as it seems capable of justifying its valuation. However, those looking for a relatively cheaper semiconductor company that’s growing at a healthy pace can consider TSMC, as the critical role it plays in the industry should help it sustain its impressive growth for a long time to come.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Apple, Intel, Nvidia, Qualcomm, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and Marvell Technology and recommends the following options: short February 2025 $27 calls on Intel. The Motley Fool has a disclosure policy.