Billionaire investor Israel Englander of Millennium Management has been selling Nvidia stock over the last several quarters.

Each quarter, institutional investment firms managing over $100 million are required to file a form 13F with the Securities and Exchange Commission (SEC). I like to think about 13Fs as an itemized receipt outlining which stocks Wall Street is buying and selling.

While analyzing the filings from Millennium Management, a hedge fund run by billionaire investor Israel Englander, I came across something pretty interesting. During the third quarter, Englander trimmed Millennium’s position in Nvidia by a modest 12.6%. While this may not seem like much, consider that Millennium has been a net seller of Nvidia stock for four consecutive quarters now.

Below, I’m going to explore two other darlings in the artificial intelligence (AI) realm that Millennium has been buying lately as the fund appears to be taking a breather from Nvidia.

1. Microsoft

During the third quarter, Millennium Management scooped up 1.6 million shares of Microsoft (MSFT 1.00%) — increasing its position by 51.4%.

In my eyes Microsoft can be credited with kick-starting the AI revolution. Shortly after OpenAI released ChatGPT in November 2022, Microsoft swooped in and invested $10 billion into the start-up. Microsoft’s rationale was to leverage ChatGPT’s generative AI capabilities and integrate this technology throughout its ecosystem.

The biggest new product release out of Microsoft following its partnership with OpenAI is the introduction of a host of virtual assistants, called Copilot. According to Microsoft CEO Satya Nadella, “Nearly 70% of the Fortune 500 now use Microsoft 365 Copilot, and customers continue to adopt it at a faster rate than any other new Microsoft 365 suite.”

Do not underestimate Nadella’s words. Microsoft’s first-mover advantage in the AI landscape has allowed the company to not only develop AI-powered services faster, but sell them more quickly as well. I see the rapid adoption of Copilot by the world’s largest enterprises over the last two years as an extremely encouraging sign. And what’s even better is that Nadella subtly alludes to the idea that Copilot’s momentum is just getting started.

In this article, fellow Fool.com contributor Danny Vena notes that growth from Microsoft’s Azure cloud computing business “included roughly 12 points from AI services.” This metric is going to become critical for Microsoft over time.

It’s well known by now that Microsoft is a dominant force in the cloud space, primarily competing with Amazon and Alphabet. As time goes on, I encourage investors not only to look at the rate at which Azure is growing relative to the competition, but to really dial in on how much of its growth can be traced back to Microsoft’s AI efforts.

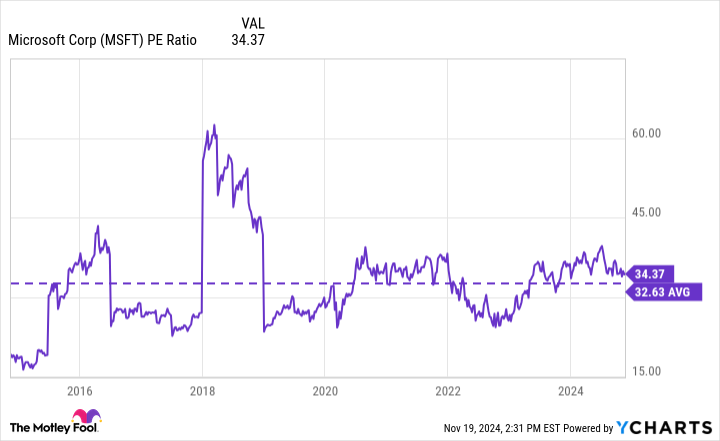

MSFT PE Ratio data by YCharts

In addition to Microsoft’s impressive penetration of the AI market so far, what may have also influenced Englander’s decision to buy the stock is valuation. Right now, Microsoft shares trade at a price-to-earnings (P/E) multiple of 34.4. Indeed, this is considerably higher than that of the S&P 500 — which has an average P/E ratio of 27.9. However, as the chart above indicates, Microsoft’s current P/E is essentially in line with the company’s 10-year average multiple.

Microsoft may actually be underpriced right now despite its premium to the broader market. Microsoft is a much larger and more sophisticated company today than it was a decade ago. Moreover, the AI narrative is just getting started; and if Microsoft’s current progress is any indication of what’s to come, I’d say the company’s long-run outlook is quite strong.

I think Microsoft is a compelling opportunity at the moment and think Millennium’s decision to buy the stock will prove wise.

2. Meta Platforms

Another AI stock that Englander doubled down on during the third quarter is Meta Platforms (META -0.70%). The table below breaks down Millennium’s activity in Meta stock over the last several quarters.

| Metric | Q3 2023 | Q4 2023 | Q1 2024 | Q2 2024 | Q3 2024 |

|---|---|---|---|---|---|

| Shares Owned | 2.3 million | 2.0 million | 2.5 million | 1.2 million | 1.3 million |

Data source: Hedge Follow.

The most obvious takeaway from the data above is that Millennium has been in and out of Meta Stock to varying degrees over the last several quarters. Most notably, the fund trimmed its position significantly between Q1 and Q2 of this year, only to begin adding again over the latest quarter.

Admittedly, Meta’s position in the AI realm has been difficult to gauge. Although the company has an enormous advertising operation, Meta’s Facebook and Instagram face fierce competition from the likes of Google, YouTube, TikTok, and even smaller social media platforms such as Pinterest and Snap.

Moreover, the company’s initial foray into AI was met with mixed results. While the prospects of Meta’s virtual and augmented reality business is still a question mark, the company’s generative AI large language model (called Llama) is starting to give alternatives built by Amazon, Google, and OpenAI a run for their money.

As I previously wrote, integrating AI into its products could result in higher engagement rates across its social media platforms. During the company’s third-quarter earnings call, Meta’s management validated my theory — citing that its AI applications have started already yielding more time spent on Facebook and Instagram.

The lucrative opportunity here is that if Meta can translate these rising engagement rates to more growth in its core advertising business, the company can reinvest that growth into additional AI projects and continue building a more diversified business overall.

While there is still a lot to prove, the tide finally seems to be turning for Meta. These dynamics could be influencing Englander’s decision to cautiously begin buying the stock again.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Pinterest. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.