The legendary investor is moving his capital into two different emerging categories. One stock is already up big for him.

Stanley Druckenmiller has sold out of Nvidia (NVDA 0.80%). Saying he regrets selling the stake too early for his Duquesne Family Office, one of the best investors ever confirmed he has gotten out of the high-flying artificial intelligence (AI) stock at around $80-$95 earlier this year. While he is now watching from the sidelines, Druckenmiller was along for much of the 500% gains in Nvidia over the last three years, generating hundreds of millions in gains for his portfolio.

So, what is he buying next? We can see through his 13-F filing with the SEC that he has made two large bets for his portfolio this summer. Here’s what Stan Druckenmiller is buying instead of Nvidia right now.

1. Coherent: A new way to bet on AI?

Duquesne’s largest position today is Coherent (COHR -0.90%), making up close to 10% of the portfolio. The company is a provider of photonics, lasers, and materials for the industrial market. In fact, it serves many different market segments, including manufacturing, communication products for internet and cloud providers, computer chips, and instrumentation for life sciences research.

All four of these sectors are enjoying big tailwinds, especially in North America, where Coherent generates over half of its revenue. One could argue it is a new way to play the growth in AI spending, given the importance of manufacturing, the cloud, and semiconductors to this rapidly growing sector. Perhaps this is why Druckenmiller is buying the stock.

Over the last 12 months, Coherent has generated $4.7 billion in revenue. Revenue was up 9% last quarter. However, if we look under the hood, the Communications segment (i.e., AI datacenters) grew revenue by 19% and now makes up the majority of Coherent’s sales. This can accelerate revenue growth over the next few years if this trend continues.

Right now, Coherent isn’t generating much in profits due to its reinvestment for growth. It does have solid gross margins closing in on 40% last quarter, which should lead to decent bottom-line margins at scale. If Coherent keeps scaling its revenue due to the tailwinds in its end markets, the stock will likely do well for those who hold for the long term.

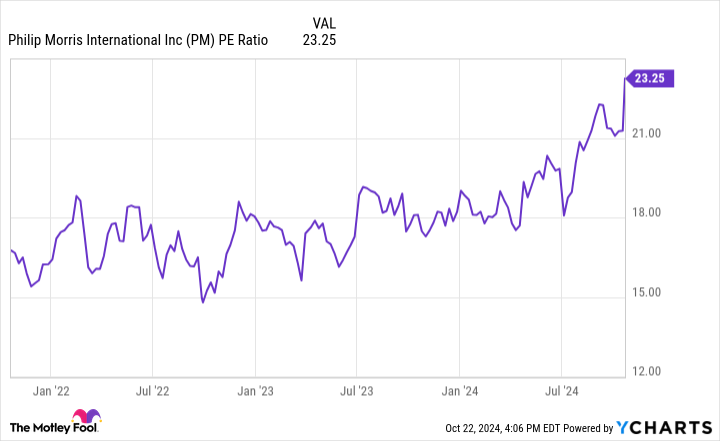

PM PE Ratio data by YCharts

2. Philip Morris International: A resurgent nicotine market

Druckenmiller’s other bet is not focused on technology, so this may be for those wary of high-tech industries that are hard to understand. In fact, this stock is understandable for everyone.

Philip Morris International (PM -2.21%) is one of the world’s largest tobacco companies. It is the most successful of the legacy tobacco companies to push into less harmful nicotine products like nicotine pouches and heat-not-burn tobacco units. Druckenmiller owns the underlying stock as well as call options, making it a new position last quarter.

So far so good with this investment. On Oct. 22, Philip Morris reported strong quarterly earnings. Shipment volume was up 2.9% year over year, revenue grew 11.6%, and profit margins expanded. Unlike other tobacco companies, Philip Morris is actually growing volumes due to its heavy exposure to these fast-growing new products like Zyn nicotine pouches.

This growth is showing no signs of slowing down, either. Along with pricing power implemented on traditional cigarette products, Philip Morris International has a ton of room to grow its volume and profits over the next few years. The stock currently has a price-to-earnings ratio (P/E) of 23, which is below the S&P 500. It should be able to grow earnings much faster than the market average.

Plus, the stock comes with a dividend yield of 4.11%. No wonder Druckenmiller added the stock to its portfolio last quarter. This is a blue chip stock with a lot of upsides over the next decade.

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool recommends Coherent and Philip Morris International. The Motley Fool has a disclosure policy.