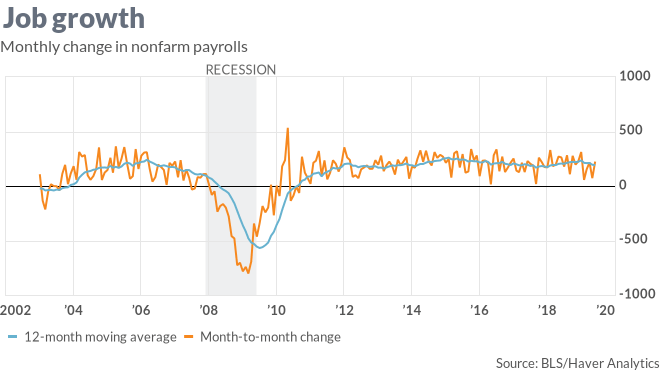

That sound you heard on Friday was either a collective sigh of relief or the air leaking out of the stock market on news that the U.S. economy created 224,000 new jobs in June, part of a solid reading on the employment situation in the United States.

The urgency for a 50-basis-point rate cut from the Federal Reserve at the end of this month, on which stocks seemed to be pinning their hope, was alleviated by the rebound in June job creation after a disappointing 72,000 increase in May.

The recent swings in the monthly jobs numbers got me thinking about the performance of employment at business-cycle peaks and its reliability as a coincident indicator. So I decided to look at the data.

Where we are, not where we are going

Most of the time, the peak in employment coincides pretty closely with the peak of the business cycle, as determined by the National Bureau of Economic Research’s business cycle dating committee. After all, employment is widely acknowledged to be a coincident indicator. It’s a good measure of where we are, not where we are going.

Nonagricultural employment, as measured by the monthly survey of businesses, is one of four metrics, along with industrial production, personal income less transfer payments, and manufacturing and trade sales, that comprise the Conference Board’s Index of Coincident Indicators.

The NBER’s business cycle dating committee takes those same metrics into account when it determines the official dates of business cycle peaks and troughs.

| Business-cycle peak | Employment peak | Payrolls at business-cycle peak |

| Feb. 1945 | Nov. 1943 | -2 |

| Nov. 1948 | Sept. 1948 | -53 |

| July 1953 | July 1953 | 17 |

| Aug. 1957 | Aug. 1957 | 5 |

| April 1960 | April 1960 | 359 |

| Dec. 1969 | March 1970 | 155 |

| Nov. 1973 | July 1974 | 313 |

| Jan. 1980 | March 1980 | 128 |

| July 1981 | July 1981 | 111 |

| July 1990 | June 1990 | -33 |

| March 2001 | Feb. 2001 | -43 |

| Dec. 2007 | Jan. 2008 | 110 |

Looking at the dozen business cycle peaks starting in 1945, four coincided with the peak month in total employment. There were three instances where employment was on the wane a month or two before the cycle peak, which is close enough for government work.

What jumped out at me from the table I constructed of business-cycle peaks, employment peaks and the monthly change in nonfarm payrolls in the cycle peak month were the exceptions and quirks.

For example, one glaring miss was the 1973-1975 recession. (Until the Great Recession of 2007-2009, the 1973-1975 downturn was the post-war poster child for long, deep recessions.) The NBER designated November 1973 as the cycle peak. Employment kept rising, topping out in July 1974, a lag of eight months.

The performance of employment at the 1960 business cycle peak underscores the notion that employment is always up before it turns down! The business-cycle peak in April 1960 coincided with a monthly increase in nonfarm payrolls of 359,000. The following month, employment plunged by 338,000 and posted monthly losses until March 1961, one month after the cycle trough.

How accurate is the signal?

My point in constructing the table was not to suggest that the job market is flailing — hiring is slowing, not collapsing — or that a recession is imminent. It was merely to examine how accurate a predictor of turning points in the economy employment is.

The NBER puts a lot of faith in employment in designating cycle peaks and troughs. Here is what the committee had to say in its Dec. 1, 2008, announcement that a peak in economic activity had occurred in December 2007:

“Because a recession is a broad contraction of the economy, not confined to one sector, the committee emphasizes economy-wide measures of economic activity. The committee believes that domestic production and employment are the primary conceptual measures of economic activity.”

Domestic production, or gross domestic product, is a quarterly figure released one month after the quarter ends, revised twice at monthly intervals and then reassessed for annual benchmark revisions. Which is why the NBER does not use the standard definition of recession as two consecutive quarterly declines in real GDP, and instead relies on monthly indicators in assessing when “a significant decline in economic activity” occurs.

Incomes just as important

The committee stresses that it does not rely solely on output, or GDP, but gives equal weighting to gross domestic income, which often varies from the output measure.

Employment represents one of the best readings on the current state of the economy. Why? Because for most families a job and a salary are the means for spending. And consumer spending accounts for about 70% of GDP. So as the consumer goes, so goes the nation.

It is not a mistake for the Fed, economists and financial markets to focus on employment as a contemporaneous read on how well the economy is doing. However, month-to-month gyrations can be misleading, especially when outliers such as May’s soft job numbers aren’t supported by weekly jobless claims or other relevant statistics.

That said, we all need to lighten up when it comes to relying on a single report for a single month.