The streaming media leader remains a divisive investment.

Roku (ROKU 2.25%) minted a lot of millionaires in its first four years as a public company. The streaming device and software maker went public at $14 on Sept. 28, 2017, and it soared 3,325% to its all-time high of $479.50 on July 26, 2021. A $30,000 investment in its IPO would have blossomed to $1.03 million.

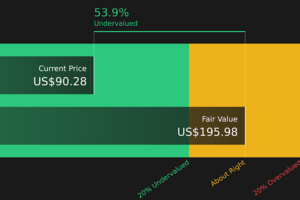

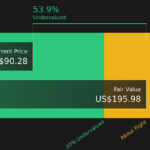

But today, Roku only trades at about $64. That same investment would have withered to roughly $137,000 as the company disappointed its investors with its slowing growth, shrinking moat, and persistent losses. Rising interest rates also squeezed its valuations.

Image source: Getty Images.

However, Roku’s 357% return since its IPO would still have beaten the S&P 500‘s 129% rally during the same period. So could Roku’s stock perk up again and generate millionaire-making gains from a fresh $30,000 investment today?

Why did the bulls lose interest in Roku?

Roku is the leading producer of streaming media devices in North America, but it faces stiff competition from Apple TV, Amazon‘s Fire TV, Samsung’s smart TVs, and other similar devices. Roku currently sells its hardware players at a loss to tether more viewers to its higher-margin platform business, which generates ad revenues from its display ads on Roku OS and its ad-supported streaming videos.

Roku experienced a major growth spurt throughout the pandemic’s height as people stayed home, bought more streaming devices, and consumed more streaming content. However, its growth cooled off in 2022 and 2023 as those tailwinds dissipated, more competitors fragmented the market, and the macro headwinds curbed consumer spending and drove more companies to rein in their digital ad campaigns.

Roku’s numbers of active accounts and streaming hours have risen constantly since its IPO, but its average revenue per user (APRU) peaked in 2022 and fell in 2023. As a result, its total revenue growth slowed down significantly over the past two years.

|

Period |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

|---|---|---|---|---|---|---|---|

|

Active Accounts (Millions) |

19.3 |

27.1 |

36.9 |

51.2 |

60.1 |

70.0 |

80.0 |

|

Streaming Hours (Billions) |

14.8 |

24.0 |

37.8 |

58.7 |

73.2 |

87.4 |

106.0 |

|

ARPU (TTM) |

$13.78 |

$17.95 |

$23.14 |

$28.76 |

$41.03 |

$41.68 |

$39.92 |

|

Revenue Growth |

29% |

45% |

52% |

58% |

55% |

13% |

11% |

Data source: Roku. YOY = Year over year. TTM = Trailing 12 months.

As Roku’s revenue growth decelerated, it ramped up its investments in original Roku Channel content, new live sports contracts, and loss-leading smart TVs. That mix of slower sales and rising expenses drove away a lot of Roku’s early investors.

Is Roku’s business finally stabilizing?

But in the first nine months of 2024, Roku’s number of active accounts grew 13% year over year to 85.5 million, and its total streaming hours rose 21% to 92.9 billion. Its trailing 12-month ARPU stayed flat at $41.10, but its total revenue still rose 16% year over year as its platform and device segments grew. It expects its revenue to rise 16% for the full year — and that acceleration counters the bearish notion that Roku is running out of steam.

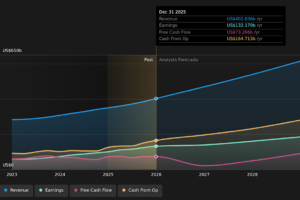

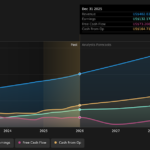

From 2023 to 2026, analysts expect Roku’s revenue to increase at a compound annual growth rate (CAGR) of 14%. Its business is certainly maturing, but it’s also cutting costs as its revenue growth cools down. That’s how it’s kept its adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) and trailing 12-month free cash flow (FCF) positive over the past five consecutive quarters.

Analysts expect Roku’s adjusted EBITDA to soar from just $4 million in 2023 to $448 million in 2026. With an enterprise value of $9.1 billion, Roku looks reasonably valued relative to those expectations at 2 times next year’s sales and 31 times its adjusted EBITDA.

We should take those estimates with a grain of salt, but they could be achievable if it continued to lead the free ad-supported streaming video market, which Grand View Research predicts will expand at a CAGR of 23% from 2024 to 2030.

But could Roku generate more millionaire-maker gains?

If Roku matches Wall Street’s expectations through 2026, grows its revenue at a steady CAGR of 14% over the following six years, and maintains the same forward valuations, its stock could potentially rally about 150% to $160 by the end of 2031. That would be a decent seven-year gain, but it would still be far below its all-time high. It also probably wouldn’t make its new investors millionaires unless they invest more than $400,000. Therefore, Roku won’t head off a cliff anytime soon — but investors shouldn’t expect it to repeat its millionaire-making run from 2017 to 2021.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Leo Sun has positions in Amazon and Apple. The Motley Fool has positions in and recommends Amazon, Apple, and Roku. The Motley Fool has a disclosure policy.