(Bloomberg Opinion) — Southeast Asia’s largest lender happens to be its most tech-savvy. Why then is Singapore’s DBS Group Holdings Ltd. missing out on some of the region’s hottest deals in digital banking?

In recent years, technology has played a large role in the bank’s profitable pivot away from trade financing to corporate cash management. One of its application programming interfaces that hooks up with customers’ software – it has some 500 of them – allows merchants on Indonesian e-retailer PT Bukalapak.com to get paid in real time. The same technology allows drivers at ride-hailing company Gojek to get fares credited from their app wallets into bank accounts. But though DBS is the most aggressive of Singapore’s three home-grown banks, bigger international rivals are capturing prime deals in its backyard. The No. 1 challenger is Citigroup Inc.

This week, the U.S. bank won the mandate to issue the first co-branded credit card for Southeast Asian e-commerce. Alibaba Group Holding Ltd.’s Lazada operates online stores in Singapore, Indonesia, Malaysia, the Philippines, Thailand and Vietnam. Back in June, ride-share behemoth Grab Holdings Inc. announced a similar card partnership. That, too, was snagged by Citi.

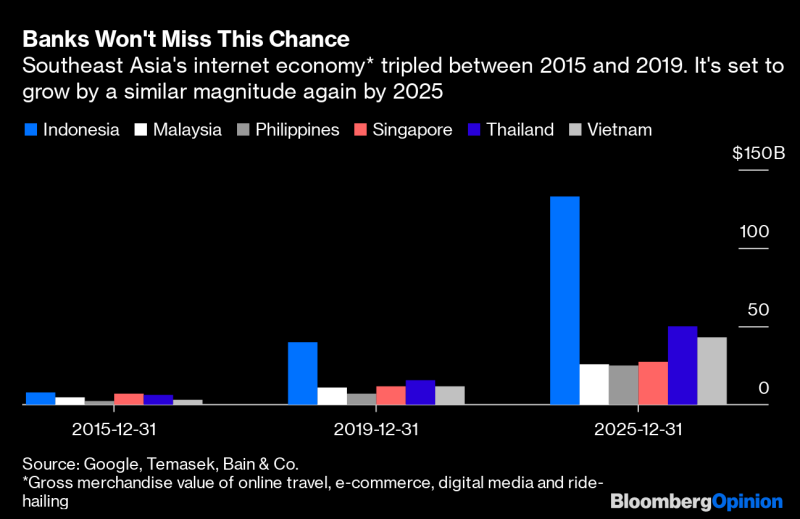

This matters intensely. The internet economy in Southeast Asia, a region of nearly 650 million people, is on track to exceed $100 billion this year before tripling by 2025, according to research released Thursday by Alphabet Inc.’s Google, Temasek Holdings Pte and Bain & Co. Financing. Online commerce, which sits at the intersection of consumer and transaction banking, has become a new battleground. Tech companies want to deal with banks that can wrap their traditional offering of cash management with services that are important to end-customers, such as simple user interfaces.

It isn’t so much that DBS is slackening but that far bigger competitors are moving onto its turf. The fact that Citi customers in Asia can pay for their Spotify subscriptions with card points made it into the U.S. bank’s annual report. JPMorgan Chase & Co. has invested $40 billion on technology in four years and is hawking new capabilities to Asian corporate clients.

Goldman Sachs Group Inc.’s foray into digital consumer banking may have been a money-losing proposition so far. But its credit card with Apple Inc. shows that Goldman, too, will eventually come for a slice of Southeast Asia’s banking services market. So will Japanese lenders, propelled by negative interest rates at home.

DBS’s lack of scale outside Singapore isn’t for want of trying. In 2013, nationalist politics in Indonesia thwarted its $6.5 billion acquisition of PT Bank Danamon, which eventually fell in the lap of Mitsubishi UFJ Financial Group. Since then, DBS has acquired Australia and New Zealand Banking Group Ltd.’s retail and wealth businesses in Singapore, Hong Kong, China, Taiwan and Indonesia. It’s open to more such “bolt-on” acquisitions where it can overlay physical assets with its digital strategy, CEO Piyush Gupta told Bloomberg TV last month.

More is definitely needed. DBS has less than S$24 billion ($17 billion) in assets in South and Southeast Asian markets – mainly comprising Indonesia, India and Malaysia’s offshore financial center at Labuan. It’s a fraction of the bank’s assets of S$355 billion in Singapore and S$90 billion in Hong Kong. Total income from South and Southeast Asia was under S$800 million last year, and after-tax profit was just S$1 million.

Meanwhile, Citi’s local regulatory filings suggest that about 28% of its $14.5 billion Asia revenue – or $4 billion – came from Southeast Asia, with Singapore, Indonesia, the Philippines, Thailand and Malaysia in the $500-million-plus annual revenue club. This is why I’ve previously argued that any calls by dissident shareholders for Citi CEO Mike Corbat to ditch its Asian consumer banking business should be rejected. That balance sheet is important to the corporate and investment bank, and for bagging deals like leading the startup Gojek’s financing round.

World trade is in the doldrums. Southeast Asia’s larger economies aren’t immune to a global slowdown, but they’re weathering it relatively better than China and India. The rise of consumer tech is where the opportunity lies. Even local lenders like Indonesia’s Bank Central Asia Tbk are doing online-payment partnership deals, such as with shopping app Shopee.

At the annual DBS investor day two years ago, analysts were pleasantly surprised to learn from Chief Financial Officer Chng Sok Hui that consumer and small-enterprise banking in Singapore and Hong Kong – 44% of the lender’s business – was already three-fifths digital. The expectation was that online prowess would give DBS an edge in its neighborhood. It isn’t panning out that well.

To make the most of its digital promise, DBS needs to bulk up in Southeast Asia. The outcome isn’t entirely in its hands. One test will be whether Indonesian President Joko Widodo’s recent promise to further open up the economy will make Singaporean banks more welcome. Whether Southeast Asia moves toward becoming a single economic area treating financial institutions the same across borders will also matter. Ultimately, politics will determine who gets to profit from financing the region’s coming $300 billion internet economy.

To contact the author of this story: Andy Mukherjee at [email protected]

To contact the editor responsible for this story: Patrick McDowell at [email protected]

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="For more articles like this, please visit us at bloomberg.com/opinion” data-reactid=”62″>For more articles like this, please visit us at bloomberg.com/opinion

©2019 Bloomberg L.P.