Super Micro Computer investors have had a roller-coaster ride in 2024.

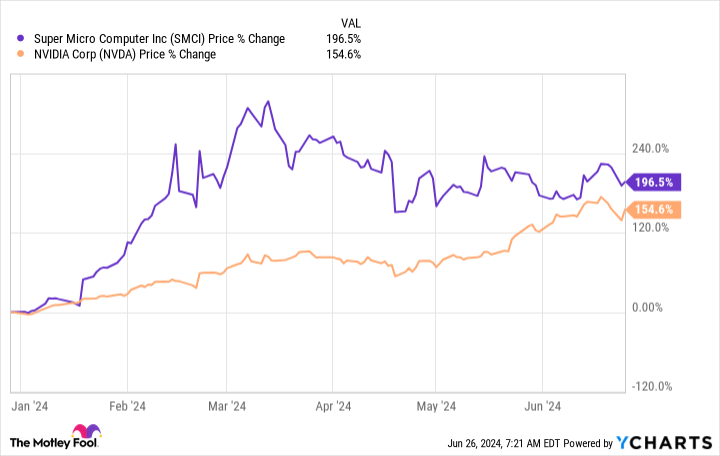

Super Micro Computer (SMCI -7.98%) was one of the most prominent artificial intelligence (AI) investments of the year, rocketing over 300% higher from the start of the year to mid-March. Since then, the stock declined around 30% and has stayed fairly steady since the end of March.

So, should investors consider an AI stock that has been successful but has been sitting dormant for a while? After all, it was one of the best-performing stocks in the market to start the year.

Supermicro is in a far more competitive space than Nvidia

Super Micro Computer (often called Supermicro) builds servers and data center components. This industry is clearly benefiting from the AI arms race, which is essentially the same trend driving Nvidia higher. As a result, investors saw this as a second chance to get in on Nvidia after they missed the move in 2023 (even though Nvidia is up over 150% in 2024 so far).

If you had that idea on New Year’s Day and put it into action the following trading day, you’d still be beating Nvidia. But with Nvidia’s steady rise, that may not last for long.

But why has Supermicro been so stagnant for so long? A lot of it has to deal with high expectations. After Nvidia posted multiple consecutive quarters of revenue tripling, investors expected Supermicro to post similar figures, as it is affected by the same trend.

However, that was a flawed analysis, as the industry that Supermicro competes in is far more competitive. With competition from heavy hitters like Dell and Hewlett Packard, Supermicro has its work cut out for it. The primary differentiating factor for Supermicro is how customizable it makes its servers, as they can be tailored for any workload or size.

This still makes Supermicro a top pick in the space, but it doesn’t make it the cheapest.

Another factor for Supermicro comparatively slower growth is that the largest customers may be building some of their servers in-house. While they still source some components from Supermicro, it’s not the same as if they were buying everything from the company.

With all of these factors adding up to not meeting the incredibly high expectations, reality set in, and investors sold off the stock from its highs. But have they gone too far?

The stock is still valued highly

In its earnings report for the fiscal third quarter of 2024, ending March 31, management reiterated its long-term goal of generating $25 billion in annual revenue. Considering its guidance for fiscal year 2024 revenue of $14.7 to $15.1 billion, Supermicro still has a ways to go.

But what if it did achieve that goal?

If Supermicro could generate $25 billion in annual revenue at its current profit margin (10.5%), then it would produce a hypothetical $2.63 billion in annual earnings.

Now, if we divide its current market cap by that earnings figure, we would get its price-to-earnings (P/E) valuation. That calculation yields a P/E of 18.8, which isn’t a bad price for a stock. At the height of Supermicro’s price in mid-March, that calculation yielded a P/E of 25.6, which is far higher.

So, is this a price worth paying? I’d say no. For this projection to hold water, everything must go right and be sustained. Any deviation to the downside renders this analysis void and would make it a bad investment. With so little margin for error, I will pass on Supermicro stock, even though the company may continue to succeed.

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.