Investors should start bracing themselves for an earnings recession, with first-quarter numbers for the S&P 500 expected to suffer the first decline in nearly three years, as macroeconomic headwinds continue to pull down analyst estimates.

Although some say low investor expectations and the stabilization of the macro outlook suggest the recent stock market rally can continue toward fresh highs, others are worried that macro uncertainties and risks to the earnings outlook for the rest of the year have yet to be fully appreciated.

RBC Capital’s Head of U.S. Equity Strategy Lori Calvasina said that based on early reports, earnings sentiment appeared to bottom in January, while Stifel Nicolaus strategist Barry Bannister said it was “too soon” to call an earnings recovery as consensus expectations for the year are still falling.

Meanwhile, the outlook for the first-quarter continues to get more negative, and the second-quarter outlook turned slightly negative for the first time on Wednesday.

John Butters, senior earnings analyst at FactSet, said that as of April 5 more companies are cutting earnings guidance than usual, leading analysts to make bigger cuts to their forecasts. He said 74% of the S&P 500 SPX, +0.00% companies that have issued earnings guidance have lowered expectations, above the five-year average of 70%. As a result, the average analyst EPS estimate has been lowered by 7.3% during the first quarter, compared with the five-year average decline of 3.2%.

| Index/sector | Blended Q1 EPS % growth estimate (decline) as of April 11 | Blended Q1 EPS % growth estimate (decline) as of Dec. 31 | Blended Q2 EPS % growth estimate (decline) as of April 11 |

| S&P 500 | (4.6) | 3.4 | (0.3) |

| Communication services | (1.6) | 2.3 | 3.0 |

| Consumer discretionary | (6.1) | (0.7) | 2.4 |

| Consumer staples | (5.1) | 0.6 | (1.1) |

| Energy | (23.6) | 20.3 | (0.4) |

| Financials | (4.0) | 1.7 | 2.7 |

| Health care | 3.8 | 8.3 | 2.4 |

| Industrials | (1.7) | 5.2 | 2.2 |

| Information technology | (10.6) | (2.7) | (9.0) |

| Materials | (12.6) | 4.4 | (4.2) |

| Real Estate | 2.0 | 3.7 | 2.0 |

| Utilities | 3.6 | 4.6 | 2.5 |

| FactSet | |||

Among headwinds mentioned by some early reporters and those revising first-quarter and full-year guidance ranges include the ongoing trade dispute with China and the threat of a new battle with Europe, adverse weather conditions, the government shutdown, rising raw materials costs, dollar strength and slowing global growth.

See: Ominous storm clouds warn of worldwide recession

“Bottom line, this earnings season is make or break for this market, because we need earnings growth to resume if the S&P 500 is going to continue to grind higher and test the former all-time highs, and 3,000 in the S&P 500,” according to analysts at Kinsale Trading LLC, in the firm’s “The Sevens Report.”

Read more: 5 things JPMorgan CEO Jamie Dimon is worried about for America and his bank.

Earnings reporting season unofficially kicks off on Friday with the banks, with J.P. Morgan Chase & Co. JPM, +0.84% and Wells Fargo & Co. WFC, -0.10% scheduled to reveal results before the open. The busiest period will start the week of April 22 and run through May 3, when “an avalanche of results from various sectors” are released, analysts at Kinsale Trading wrote.

Don’t miss: Bank earnings preview: The Fed’s moves are squeezing profits once again.

FactSet publishes a “blended growth” estimate for the year-over-year percentage change in earnings per share for the S&P 500, that represents a blend of results already reported and the average analyst estimates of coming results.

With 25 of 505 S&P 500 companies having reported results as of Wednesday afternoon, the blended growth estimate is a negative 4.6%, with 8 of 11 sectors expected to show a year-over-year EPS decline. That’s a big swing lower from expectations for growth of 3.0% estimated as of Dec. 31.

That puts earnings on track to suffer the first decline since the second quarter of 2016, when they fell 2.6%, and the biggest decline since the first quarter of 2016’s 6.6% drop, according to FactSet data.

Also read: S&P 500 earnings outlook cut down again, toward first decline in 3 years.

The sectors currently expected to see the biggest EPS declines are energy at 23.6%, materials at 12.6% and information technology at 10.6%, according to FactSet. The three sectors expected to show EPS growth are health care at 3.8%, utilities at 3.6% and real estate at 2.0%.

But perhaps more important for the outlook for the stock market is that the blended EPS growth estimate for the second quarter slipped into negative territory on Wednesday, to -0.3% from a rise of 3.4% as of Dec. 31.

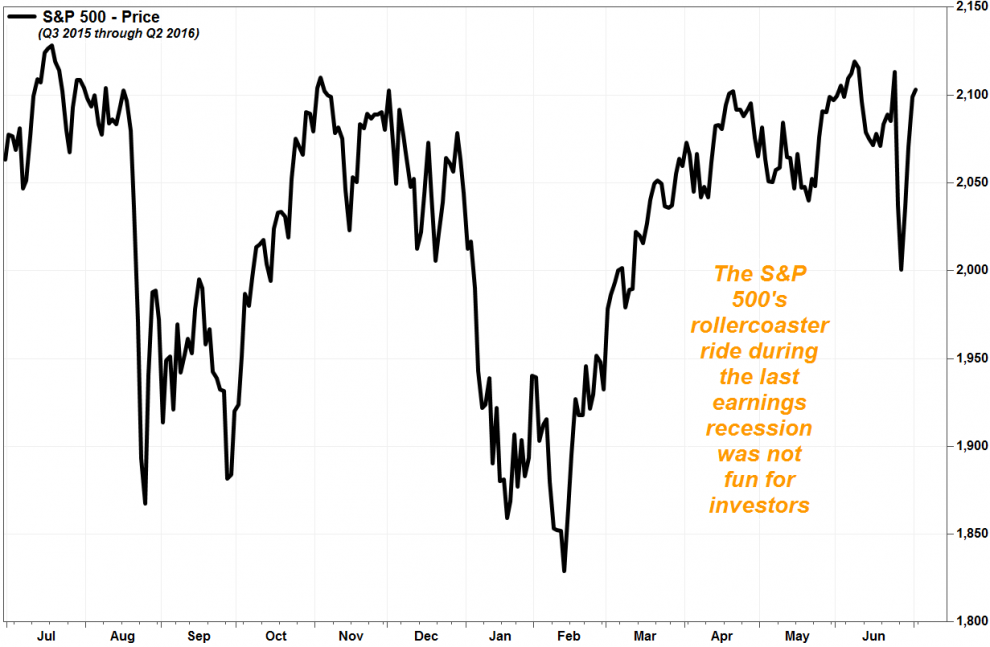

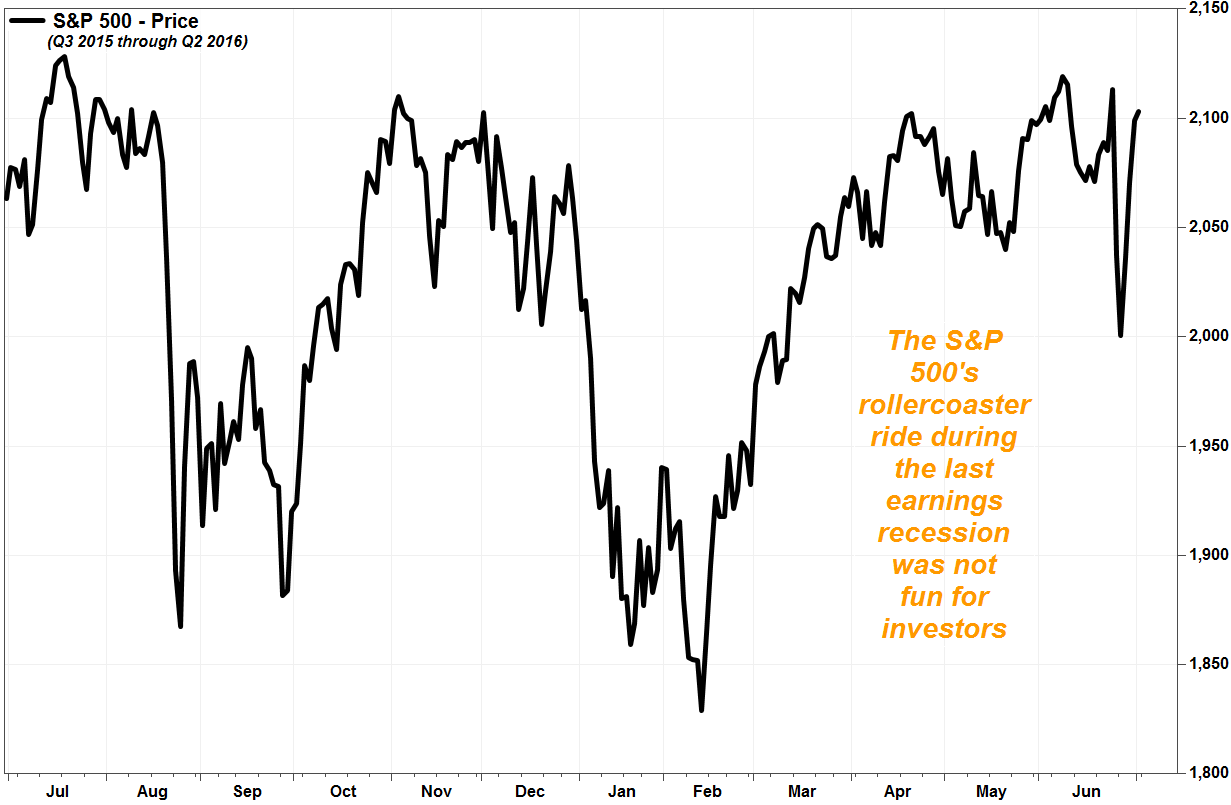

A recession is generally defined as at least two consecutive quarters of declines. The last earnings recession stretched from the third quarter of 2015 through the second quarter of 2016. The resulting S&P 500 roller coaster was not a particularly fun ride for investors. Read more about the last earnings recession.

FactSet, MarketWatch

FactSet, MarketWatch

Investors don’t seem too worried about a potential earnings recession at the moment. The S&P 500 tumbled 14% during the last three months of 2018, as investors anticipated an earnings decline, then rallied 13% during the first quarter. Since then, as the second-quarter outlook turned negative, the index has gained 1.9%.

Here are some things investors can expect companies to touch on as they report results:

Trade tensions are expected to feature prominently again this earnings season and investors can brace for fresh news of cost cutting, job losses and price increases as companies scramble to deal with tariff costs and restrictions.

On Tuesday, the International Monetary Fund cut its global growth forecast for the third time in six months, citing trade conflict among other items.

“The balance of risks remains skewed to the downside,” the IMF said. “Failure to resolve differences and a resulting increase in tariff barriers above and beyond what is incorporated into the forecast would lead to higher costs of imported intermediate and capital goods and higher final goods prices for consumers.”

See related: IMF worries financial conditions could change abruptly.

The report came as Congress works to pass the United States-Mexico-Canada Agreement, or USMCA, a treaty that aims to replace the North American Free Trade Agreement, known as NAFTA. At the same time, the administration of President Donald Trump is struggling with a separate trade deal with China, and has threatened tariffs on $11.2 billion worth of European Union goods.

Read: Opinion: Why the toughest part of a U.S.-China trade deal still lies ahead.

There’s a lot at stake, according to Jason Pride, Chief Investment Officer of private wealth for Glenmede.

“The U.S. and China combined constitute about 40% of world GDP,” Pride wrote in a note. “In an environment of increasingly intertwined economic relationships, businesses are eager for more clarity on the “rules of the game” on trade between these two economic behemoths. The upside from a trade deal may be increased business confidence to invest in growth, due to a solid groundwork on terms of trade.

FactSet

FactSet

The impact of the trade talks is being felt by a wide range of companies, which have seen input costs rise, forcing them to make decisions to offset the blow. Farmers have lost trading partners to foreign competitors, while other companies have had to forgo expansion plans or lay off workers.

A report by think tank the Cato Institute late last year identified more than 200 companies that were being hurt by tariffs, including aluminum manufacturer Alcoa Corp. AA, -2.26% aerospace giant Boeing Co. BA, +1.43% agricultural equipment maker Caterpillar Inc. CAT, +0.97% Coca-Cola Co. KO, +0.15% Ford Motor Co. F, +0.64% General Motors Co. GM, +0.20% General Electric Co. GE, -0.44% alongside many small and medium-size businesses with less financial flexibility that their bigger rivals.

“The president has tweeted that “trade wars are good and easy to win’,” said the report. “These businesses, whose numbers will grow exponentially if Trump follows through on new tariff threats, would beg to differ.”

Trade policies have had a destabilizing impact on markets, too, according to JPMorgan strategists.

“According to simple estimates (comparing earnings, impact of fiscal spending, price growth, multiples, and rates) the concerns over trade policies might have erased up to ~10% of S&P 500 value over this past year,” they wrote this week.

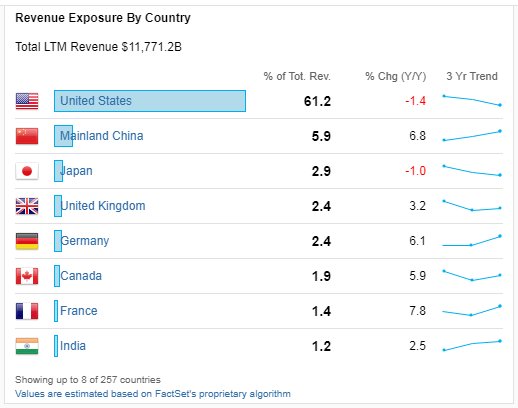

About 39% of S&P 500 revenue over the past 12 months was derived outside of the U.S., according to FactSet, with China the largest source of international revenue.

See related: Why a European slowdown poses a bigger risk to the stock market than China.

But trade is only part of the problem.

On Tuesday, irrigation equipment maker Lindsay Corp. LNN, -0.91% saw its shares tumble after it missed earnings forecasts for its fiscal second quarter, and blamed it on the negative impact the U.S.-China trade dispute is having on farmer sentiment.

“Impacts of the recent widespread flooding in the Midwest are unknown at this time, and we don’t expect to see meaningful improvement in farmer sentiment while the U. S-China trade uncertainty persists,” said Chief Executive Tim Hassinger.

And while the Federal Reserve’s decision in March to stop raising interest rates this year helped fuel the stock market’s gains, the reason for stopping—uncertainty over the growth outlook—may have reduced some spending plans.

Water solutions company Pentair PLC PNR, +1.91% saw its shares plummet this week after slashing its profit and sales outlook, citing not only bad weather and but also a slowing economy.

“To start 2019, in addition to the adverse impact from weather, we have seen moderating growth in several of our end markets,” said Chief Executive John Stauch. “We are also experiencing higher than anticipated inventory levels in some of our key distribution channels.”

Want news about Europe delivered to your inbox? Subscribe to MarketWatch’s free Europe Daily newsletter. Sign up here.