The Center for Retirement Research’s most recentundefined makes a strong case for shifting the focus of fiscal sustainability for state and local pension plans from full funding to stabilizing their pension debt as a share of the economy.

While full funding is tidy in the sense that, if the pension were to shut down, assets would be available to pay full benefits, it involves a significant opportunity cost in terms of forgoing public investment in infrastructure and education.

To assess the feasibility of shifting from full funding to stabilizing the debt, the analysis proceeds in two steps. The first looks at the future evolution of public plans under current contribution levels by projecting the annual cash flows for a nationally-representative sample of 40 state and local pension systems. The second estimates the contribution increases needed to stabilize the ratio of pension debt to the economy.

The projections under current contribution levels yield two important conclusions. First, despite the rising ratio of beneficiaries to workers, annual benefit payments as a share of the economy is already near its peak (see Figure 1). This surprising result can be attributed to two factors. The first factor is that most pension plans do not fully index their retiree benefits for inflation, which lowers the real value of average benefits over time. The second factor is that pension plans have gradually been reducing growth in average benefits in recent years due to further COLA restraints and to benefit reductions for new hires.

The other main conclusion, in terms of pension assets, is that the majority of plans do not face an imminent crisis in the sense that they are likely to exhaust their assets within the next two decades (see Figure 2). But a sizable share could exhaust their assets within 30 years under the low-real-return scenario. And even under the high-return scenario, more than 40% are at risk of depleting their assets over longer time horizons. Thus, adjustments will be necessary.

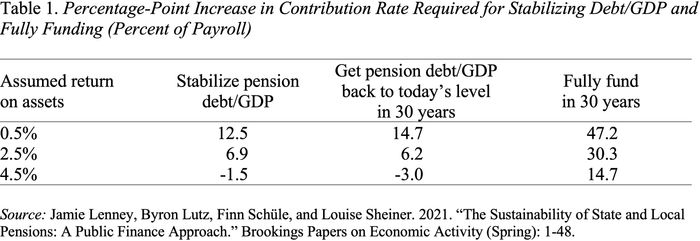

How large do those adjustments need to be? The required increase in the contribution rate to stabilize the debt-to-GDP ratio is 12.5 percentage points when assets yield 0.5%; 6.9 percentage points with a return of 2.5%; and contributions could be cut with a return of 4.5% (see Table 1). The numbers look very similar with a goal of getting the debt/GDP ratio back to today’s level in 30 years. To put these contribution changes into context, aggregate pension contributions increased by 10 percentage points between 2009 and 2019. The final column in Table 1 shows that the required percentage-point increase in contribution rates to fully fund these plans would be four or five times larger.

The research summarized in this brief is certainly not the last word on the topic. Indeed, other researchers have critiqued various aspects of the analysis. But, continuing with status quo or increasingly stringent full-funding policies also has costs. So, hopefully the basic idea presented in the brief is a step toward building a more sustainable framework for managing state and local pension plan liabilities.