(Bloomberg) — European shares look poised to replicate a largely range-bound session in Asia, as investors await key corporate earnings for fresh trading cues.

Most Read from Bloomberg

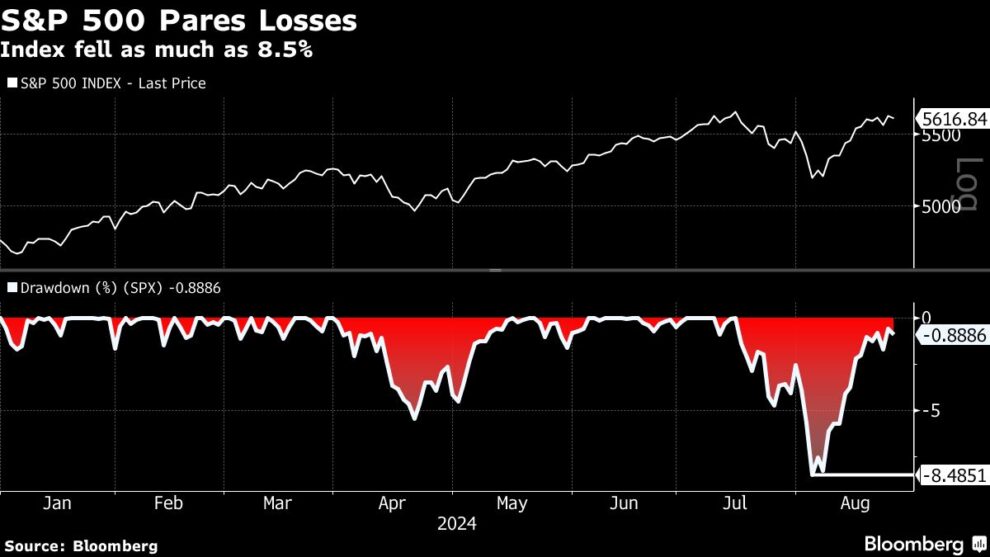

The Euro Stoxx 50 futures gained 0.1%, with their US peers virtually flat. A gauge of Asian equities fell 0.1%, snapping a three-day winning streak after rising over 11% from Aug. 5 through Monday. China and South Korea led the declines after some of the world’s largest tech names pushed the S&P 500 down.

Chinese consumption stocks were in the spotlight after PDD Holdings Inc. fell by a record. A warning of slow sales by Temu’s owner was the latest disappointment from the sector, where the country’s biggest consumer companies have reported revenue misses. The Hang Seng Tech Index declined much as much as 1.8%.

The mild losses in Asia pointed to consolidation after a strong run earlier this month that was driven by investors’ growing belief that the US central bank will start cutting interest rates in September. The caution also comes ahead of Nvidia Corp.’s keenly anticipated financial results due on Wednesday, as investors look for further clarity on demand induced by artificial intelligence.

“At some point investors in Asia will start to focus on fundamentals and earnings in the region instead of what the Fed is going to do next or who is going to be in the White House next year,” said David Chao, a global market strategist at Invesco Asset Management Singapore Ltd.

Japanese shares were one of the few bright spots in Asia, registering modest gains as small caps and domestic-oriented firms benefited from a firmer yen.

Back in China, the world’s second-largest economy showed some promising signs in its manufacturing sector, with industrial profits at the country’s large companies expanding 4.1% on year in July. For one, PetroChina Co. posted record earnings for the first half of the year as high drilling output and strong oil prices helped it weather weakening domestic fuel demand.

The looming prospect of lower US rates and a weaker greenback are also likely to have significant implications for China’s currency. Chinese companies may be enticed to sell a $1 trillion pile of dollar-denominated assets as the US cuts rates, a move which could strengthen the yuan by up to 10%, according to Stephen Jen.

Meanwhile, Beijing urged Canada to immediately correct the “wrong practices” of new tariffs against the Asian nation. Canada, an export-driven economy that relies heavily on trade with the US, has been closely watching moves by the Biden administration to erect a much higher tariff wall against Chinese EVs, batteries, solar cells, steel and other products.

Treasuries were steady in Asia after the 10-year yields rose two basis points to 3.82% Monday. The dollar was flat.

US inflation figures this week will likely reinforce that long-awaited rate cuts are coming soon, while a reading on consumer spending is seen indicating that the central bank has been successful at keeping the expansion intact.

Economists see the personal consumption expenditures price index excluding food and energy — the Fed’s preferred measure of underlying inflation — rising 0.2% in July for a second month. That would pull the three-month annualized rate of so-called core inflation down to 2.1%, a smidgen above the central bank’s 2% goal.

Fed Bank of San Francisco President Mary Daly said it’s appropriate to begin cutting rates, while her Richmond counterpart Thomas Barkin said he still saw upside risks for inflation, though he supported “dialing down” rates.

“Powell sealed the deal for a September cut at Jackson Hole — leaving intact our thesis for continued broadening/rotation,” said Ohsung Kwon at Bank of America Corp. “But don’t sleep on Nvidia earnings, a consistent driver of S&P returns and still a risk to markets if they disappoint.”

In corporate news, LG Electronics Inc. is considering an initial public offering for its India business, tapping a booming stock market to help hit a target of $75 billion in electronics revenue by 2030.

BHP Group Ltd., the world’s biggest miner, posted a full-year profit broadly in line with expectations, as revenue from iron ore and copper increased despite a deteriorating Chinese demand outlook.

In commodities, oil dropped after a three-day rally, with the threat of a halt in Libyan supply countered by a still-shaky demand outlook. Gold fell.

Key events this week:

-

Germany GDP, Tuesday

-

US Conference Board consumer confidence, Tuesday

-

Nvidia earnings, Wednesday

-

Fed’s Raphael Bostic and Christopher Waller speak, Wednesday

-

Eurozone consumer confidence, Thursday

-

US GDP, initial jobless claims, Thursday

-

Fed’s Raphael Bostic speaks, Thursday

-

Japan unemployment, Tokyo CPI, industrial production, retail sales, Friday

-

Eurozone CPI, unemployment, Friday

-

US personal income, spending, PCE; consumer sentiment, Friday

Some of the main moves in markets:

Stocks

-

S&P 500 futures were unchanged as of 2:50 p.m. Tokyo time

-

Nasdaq 100 futures were unchanged

-

Japan’s Topix rose 0.8%

-

Australia’s S&P/ASX 200 fell 0.2%

-

Hong Kong’s Hang Seng rose 0.1%

-

The Shanghai Composite fell 0.3%

-

Euro Stoxx 50 futures rose 0.2%

Currencies

-

The Bloomberg Dollar Spot Index was little changed

-

The euro was little changed at $1.1167

-

The Japanese yen fell 0.2% to 144.82 per dollar

-

The offshore yuan was little changed at 7.1243 per dollar

Cryptocurrencies

-

Bitcoin fell 0.5% to $63,161.32

-

Ether rose 0.3% to $2,697.63

Bonds

-

The yield on 10-year Treasuries advanced one basis point to 3.83%

-

Japan’s 10-year yield was unchanged at 0.880%

-

Australia’s 10-year yield advanced six basis points to 3.91%

Commodities

-

West Texas Intermediate crude fell 0.3% to $77.22 a barrel

-

Spot gold fell 0.2% to $2,512.79 an ounce

This story was produced with the assistance of Bloomberg Automation.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.