Does President Donald Trump hold the key to the stock market, able to make it rally whenever he wants? Despite claims that he does, I’m skeptical.

That’s because, powerful as Trump is, the odds are overwhelmingly against him being a successful market timer. One of the hallmarks of the stock market’s efficiency is that prices at any given time reflect all publicly available information up to that point.

In Trump’s case, all publicly available information includes how investors up until now have responded to his market-moving comments. There’s no proof that the market will react to future presidential tweets the same way it has in the past.

The market learns, in other words. This is exactly what appears to have happened in recent months. Presidential tweets that once sent the market soaring now elicit little more than a collective shrug. This suggests skepticism about Trump’s future ability to time the market’s short-term swings.

What about his ability to time the market over the longer-term? For example, some argue that Trump is trying to manipulate the stock market so that it will be at an all-time high by Election Day in 2020. If so, he would be just like every other U.S. president in the modern era, each of whom has also wanted to goose the stock market into an election-year rally.

History is not on Trump’s s side. Consider the stock market’s average returns over the 12 months prior to all presidential elections since 1971. As you can see from the table below, the Dow Jones Industrial Average’s DJIA, +0.74% return over this period is lower than in the comparable periods of the other three years of the so-called Presidential Cycle. (I chose to begin my analysis in 1971, which is when Nixon took the U.S. off the gold standard. This opened the floodgate for more government intervention in the economy.)

|

Year of Presidential Cycle |

Average DJIA 12-month return ending on 10/31 of year |

|

1 |

7.5% |

|

2 |

6.3% |

|

3 |

14.3% |

|

4 |

5.0% |

The challenge Trump faces is the one we all face in the market: The stock market’s short-term gyrations amount to little more than statistical noise. That’s just another way of saying that luck plays the predominant role in explaining the market’s shorter-term swings.

How big a role? One way of answering this question was suggested by Michael Mauboussin, the author of “The Success Equation: Untangling Skill and Luck in Business, Sports, and Investing.” Mauboussin is director of research at BlueMountain Capital Management; prior to joining BlueMountain, he was in charge of global financial strategies for Credit Suisse and was chief investment strategist at Legg Mason Capital Management.

Mauboussin argued that, as luck plays a bigger role in performance, the faster one period’s winner will become merely average in the next. This process is known in statistical circles as “regression to the mean.” An obvious example is a coin toss: even after the first toss comes up heads, the odds of the second toss coming up heads are no different than those that exist when the first toss comes up tails. Regression to the mean is immediate, in other words — and that is the paradigmatic definition of pure luck.

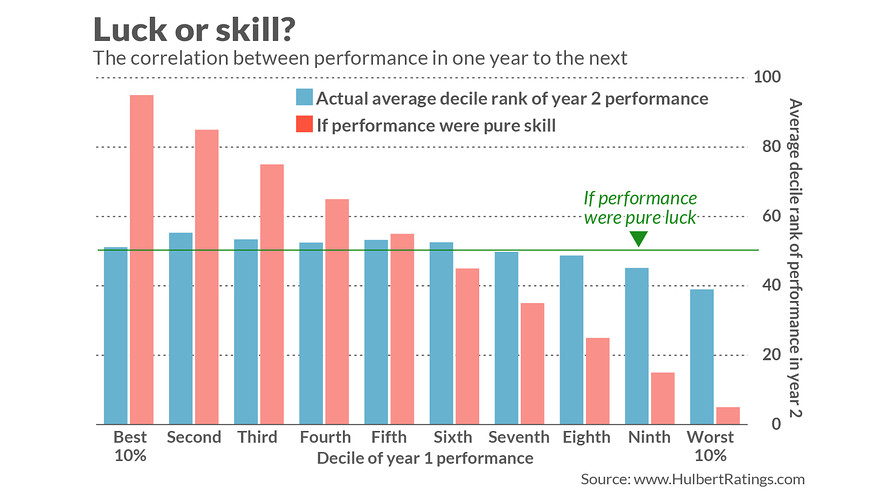

How fast does investment performance regress to the mean? To find out, I constructed a subset of investment newsletter portfolios that at any point since 1980 were in the top 10% for performance in a given year. I then measured their average rank in the years immediately following their winning years. If performance were a matter of pure skill, then their average percentile rank in year two would be 95. In fact, however, it was just 51.4 — statistically similar to the 50.0 it would be if performance were a matter of pure luck.

I reached similar results when I focused on those newsletters whose first-year ranks were lower than in the top 10%. As you can see from the chart below, their expected ranks in the second year were very close to the 50th percentile, regardless of their performance in the first year.

The only exception came for newsletters in the bottom 10% for first-year return, whose average second-year percentile ranking was 39.0 — significantly below what you’d expect if performance were a matter of pure luck. In other words, it’s a decent bet that one year’s worst adviser will be a below-average performance in the subsequent year too.

But that’s a thin reed indeed on which to base hope for successful market timing. All you can conclude from this is that you shouldn’t follow advisers who are at the bottom for trailing 12-month performance.

The market’s short-term swings are notoriously difficult to time. If someone figured out how to nevertheless do so — even Trump — chances are that the market would get wise to his success and cause his performance to regress to the mean.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at [email protected]

More: President Donald Trump: You’re doing it wrong if your ‘409K’ is up only 50%

Read: Americans own a lot of stock right now — and that’s a bad sign