The tariff dispute in which the U.S. currently is engaged with China and Mexico is not typical. Normally in trade wars, countries devalue their currencies, both as an offensive weapon as well as to lessen the impact of higher tariffs on their export sectors.

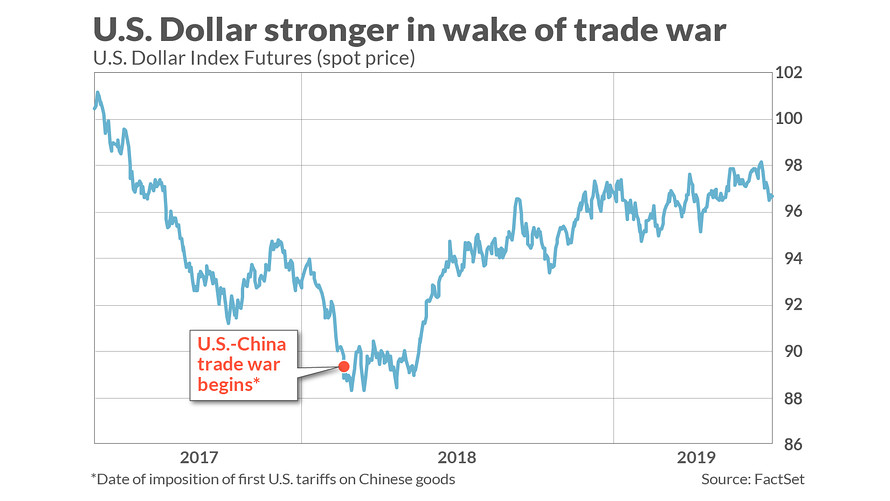

We’re not seeing that this time, at least with the U.S. dollar. DXY, +0.04% The greenback is more than 9% higher than where it stood when the trade war began in January 2018, when the first tariffs were imposed. In fact, the dollar index’s lowest level over the last 4 ½ years was registered a week after the first tariff. (See accompanying chart.)

To be sure, the dollar index reflects the greenback’s value against a basket of foreign currencies, not just those of countries engaged in the trade disputes. But the same pattern is seen in the dollar’s value against the Chinese yuan USDCNY, +0.0564% USDCNH, +0.0592% and the Mexican peso USDMXN, -0.0845% : the dollar currently is 10% and 5% higher, respectively, than where those two currencies stood in January 2018.

To assess the likely effect on the U.S. stock market of these recent trade disputes, it therefore is important to analyze the impact on corporate profits of the unexpectedly stronger dollar.

Conventional wisdom suggests that this impact will be unfavorable, since the foreign-currency prices of exported goods will rise along with the dollar, which in turn most likely will lead to fewer sales. Making this worry even bigger is the large portion — an estimated 50% — of the S&P 500’s SPX, +0.41% revenue that comes from outside the U.S.

Fortunately, there doesn’t appear to be a big cause for concern. Let me review the data, and then speculate about why the stronger dollar hasn’t had the adverse effect many had expected.

The table below tells the story, based on my analysis of data back to 1973 (courtesy of the Federal Reserve Bank of St. Louis and Yale University professor Robert Shiller).

|

Over the trailing 12 months the U.S. dollar index… |

S&P 500’s average EPS change over trailing 12 months |

S&P 500’s average EPS change over subsequent 12 months |

|

Falls |

+25.2% |

+11.3% |

|

Rises |

+12.9% |

+21.9% |

Initially, the data appear to support the conventional wisdom. During 12-month periods in which the dollar rises, earnings do appear to grow more slowly than during periods in which the dollar falls. But there’s less here than meets the eye, for two reasons.

First, given the variability in the year-by-year results, the difference between the 25.2% and 11.3% is not significant at the 95% confidence level that statisticians often use to determine if a pattern is significant. (It is only marginally significant at lower significance levels.)

Second, notice that the pattern reverses itself in the subsequent 12 months. That is, in the 12 months following periods in which the dollar rose, the S&P 500’s earnings per share rose at a faster pace, on average, than after years in which the dollar fell. (For the record, this subsequent pattern also is not significant at the 95% confidence level.)

What this means: Even if the differences in the table were statistically significant, the negative impact of a stronger dollar would be short-lived and soon corrected.

Why is the conventional wisdom wrong?

- Conventional wisdom is focusing only on the revenue side of the equation. But most of the large corporations that dominate the S&P 500 have both extensive operations overseas (expenses) as well as receive a big portion of their sales (revenue) from outside the U.S. A strong dollar means the expense side of the equation will be helped in dollar-denominated terms, while the revenue side will be hurt.

- Companies with lopsided foreign exchange exposure — with more or less revenue coming from overseas than expenses — almost certainly will hedge that exposure in the futures market or with other derivatives. To the extent those hedges are successful, of course, then the dollar’s fate on the foreign exchange markets should have little short- or even intermediate-term impact on earnings.

The immediate lesson to draw: A stronger dollar is not the cause for concern that many blindly assume it to be.

There is a broader lesson too. We should not assume — as the stock market nevertheless appears to be doing — that past trade wars are analogous to the trade dispute in which the U.S. is currently engaged with China and Mexico. While this dispute might prove to be as terrible as those previous were, we need to show that empirically rather than just assuming it’s true.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. Hulbert can be reached at [email protected]

More: Mark Mobius says U.S.-China trade fight turning ‘more strategic and critical’

Also read: There’s risk for emerging markets as China spars with U.S.