Bloomberg News/Landov

Bloomberg News/Landov

How many first-time homebuyers are there in the housing market?

That’s an important question. A smaller share of first-timers suggests that the market may be too competitive or too expensive – and ultimately not very inclusive. A bigger share suggests market conditions may be a bit easier, and that more Americans are getting a shot at attaining upward mobility.

But it is surprisingly difficult to pin down exactly how many home purchases go to first-timers, and a new set of research reports from the New York Fed attempts to correct that.

The National Association of Realtors, the trade group that’s responsible for what may be the best-known measurements of the issue, publishes an annual survey of characteristics of home buyers and sellers. NAR conducts that survey on a monthly basis and those results are tracked in their existing-home sales release.

See: These startups will help you make a down payment — by taking a stake in your house

Another measure comes from the mortgage industry. Within the mounds of paperwork any borrower must fill out, there’s one form known as the Uniform Residential Loan Application. It asks whether the borrower has had “an ownership interest in a property in the last three years.”

The inclusion of that question in the application process dates back to 1992, when Congress passed legislation known as the Federal Housing Enterprises Financial Safety and Soundness Act. The legislation established a new regulator for Fannie Mae and Freddie Mac, and also set out targets for the two mortgage giants to ensure they were serving all would-be home buyers equally and fairly.

Many analysts who focus on the role of Fannie FNMA, -1.79% and Freddie FMCC, -2.25% in contributing to the housing bubble of the last decade point to the affordable housing goals of the 1992 legislation as the beginning of that slippery slope. Other analysts, of course, focus more on the role of lenders, or believe that there’s blame to go around.

Putting that thorny question to the side for a moment, the historic accident of the URLA’s treatment of a “first-time buyer” as someone who hasn’t owned property within the past three years is still with us.

Writing for the New York Fed, two researchers have found a way to use that institution’s Consumer Credit Panel, a data set constructed from a nationally representative random sample of Equifax credit report data.

“Using the CCP, we are able to create a cleaner identification of first-time homebuyers than the official measure because we can look at the entire history of a household’s credit file back to 1999,” the researchers wrote. “We define a first-time buyer as the first appearance of an active mortgage since 1999 with no indication of any prior closed mortgages on the borrower’s credit report.”

The first time a mortgage appears on a credit profile is a more appropriate indicator of a first purchase than the URLA data provide, and a more precise measurement than second-hand self-reported identifications as those made through real estate agents, as the NAR data provide. It does have one flaw, however: because it relies on credit profiles, it does not capture home purchases made with cash.

Related: 3 outside-the-box alternatives for home buyers in a tough housing market

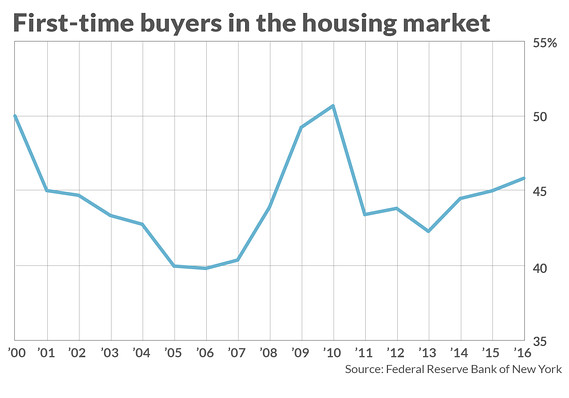

So what does the CCP data tell us about first-time buyers?

Their share of the total number of shares has been “relatively stable,” in the words of the researchers. It ranged from about 44% in 2001 to 40% in 2005 as home prices rose. After the bubble, when prices dropped, first-timers had more of a shot, and their share topped 50% in 2010. As of 2016, they made up 46% of purchases.

That shouldn’t be just a relief to anyone who’s been drawing grim conclusions about the economy based on NAR’s statistics, which have consistently shown first-timers having less than one-third of the market share. It should also serve as a reminder of how sensitive first-timers are to prices, a reality that should be top of mind for anyone designing policy to encourage homeownership.

Read: At the low end, homeowners are even more leveraged than they were during the bubble