These two attractively valued tech stocks could turn out to be smart long-term investments.

Technology stocks have been in impressive form on the market in the past year, recording gains of 33% as of this writing, thanks to the emergence of a major catalyst in the form of artificial intelligence (AI). Nvidia (NVDA 3.51%) has turned out to be one of the major beneficiaries of the proliferation of AI, with shares of the company rising an impressive 209% in the past year.

Nvidia’s stunning rally is justified by the terrific growth in the company’s revenue and earnings. Its revenue in fiscal 2024 (which ended in January) increased 126% year over year to $60.9 billion. Meanwhile, non-GAAP (generally accepted accounting principles) earnings were up 288% to $12.96 per share. Analysts are expecting Nvidia’s top line to nearly double once again in the current fiscal year to $120 billion.

So, there is a solid chance that Nvidia could remain a top tech stock in 2024 and beyond. However, Nvidia is now trading at 77 times trailing earnings and 50 times forward earnings, higher than the U.S. technology sector’s average of 47x. Nvidia’s ability to sustain its healthy growth could help it justify its expensive valuation, though it won’t be surprising to see savvy investors looking for cheaper tech stocks that could turn out to be winners in the future.

That’s why now would be a good time to take a closer look at Dell Technologies (DELL 5.01%) and DigitalOcean Holdings (DOCN -2.42%), two tech stocks that are trading at attractive valuations right now and seem set to grow at an impressive pace in the future.

1. Dell Technologies

Dell Technologies stock has shot up 172% in the past year as investors have been buying the technology specialist hand over fist on account of its improving AI prospects. However, Dell stock has retreated nearly 25% since hitting a 52-week high toward the end of May. Investors have pressed the panic button, as Dell’s financial performance wasn’t all that great last quarter, and its outlook for the current year fell short of expectations.

The good news, however, is that Dell is trading at just 1.1 times sales right now. That’s well below the U.S. tech sector’s average price-to-sales ratio of 8. Additionally, Dell’s trailing earnings multiple of 27 and forward earnings multiple of 17 make it look like an attractive bet in light of the potential acceleration in its growth.

Dell’s full-year revenue guidance of $95.5 billion would translate into an 8% improvement in its top line in fiscal 2025. That would be a significant improvement over the 14% drop in its revenue in fiscal 2024 to $88.4 billion. This impressive turnaround that Dell is forecasting this year can be attributed to the growing demand for its AI servers, as well as a recovery in the personal computer (PC) market.

Dell’s infrastructure business, which includes sales of servers and networking equipment, increased an impressive 22% year over year in the previous quarter to $9.2 billion. The company shipped $1.7 billion worth of AI servers in the first quarter of fiscal 2025, an increase of more than 100% on a sequential basis. More importantly, its AI server backlog increased 35% quarter over quarter to $3.8 billion, indicating that its infrastructure business could keep getting better.

On the other hand, Dell’s revenue in the client solutions group was flat year over year last quarter at $12 billion. However, this business seems primed for a turnaround thanks to a recovery in the broader PC market, driven by the growing adoption of AI-enabled PCs. Market research firm IDC forecasts a 2% increase in PC shipments this year following a decline of almost 14% last year.

Not surprisingly, Dell management pointed out on the company’s recent earnings conference call that it is witnessing “an improving demand environment” in PCs, a trend that’s likely to continue on account of additional catalysts such as an aging installed base of machines that will require an upgrade.

As a result, it won’t be surprising to see Dell stock regaining its mojo and rising once again as its growth accelerates. That’s the reason why investors would do well to add this tech stock to their portfolios while it is still cheap.

2. DigitalOcean Holdings

DigitalOcean Holdings provides a cloud computing platform that offers both platform-as-a-service (PaaS) and infrastructure-as-a-service (IaaS), which developers can use to build, deploy, and scale up applications. However, the stock’s performance has been poor so far this year, as it has declined close to 5%.

As a result, investors can get their hands on DigitalOcean stock cheaply, as it is trading at 4.7 times sales. The stock popped briefly after releasing its first-quarter results last month.

AI played an important role in that surge. Customers are warming up to DigitalOcean’s AI-focused cloud offerings. For instance, the demand for DigitalOcean’s cloud computing solutions, which are used for training AI models, is so strong that the company expects demand to exceed supply.

This also explains why DigitalOcean is witnessing an improvement in customer spending. Its average revenue per user (ARPU) increased 8% in Q1 to $95.13. The company has also raised its full-year revenue growth forecast to a range of $760 million to $775 million from the earlier range of $755 million to $775 million.

There is a good chance of DigitalOcean revising its full-year guidance higher as the year progresses, as management says that the company is “consistently selling through our available capacity as it comes online.” With the demand for cloud AI infrastructure set to increase at an annual rate of 31% through the end of the decade and DigitalOcean continuing to bring more capacity online to target this lucrative opportunity, there is a good chance that its growth could accelerate in the future.

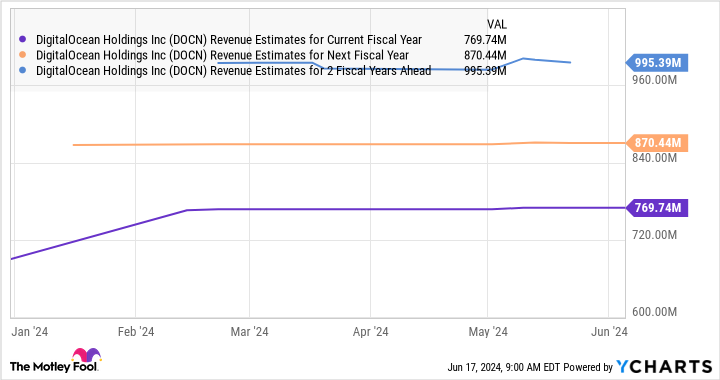

This is precisely what analysts are expecting, as seen in the chart.

DOCN Revenue Estimates for Current Fiscal Year data by YCharts

DigitalOcean’s 2024 revenue forecast points toward an 11% increase in its top line. It is expected to grow at a faster pace next year, followed by further improvement in 2026. However, DigitalOcean could deliver better growth than Wall Street expects, thanks to the company’s efforts to capture a bigger share of the cloud AI infrastructure market.

That’s why DigitalOcean Holdings could eventually turn out to be a smart buy for tech investors. It is not just cheaper than big names such as Nvidia, but also has a solid growth driver that could help deliver healthy gains in the long run.