TSMC is a much steadier business than Nvidia.

Nvidia (NASDAQ: NVDA) has captured the heart of the artificial intelligence (AI) investment trend by providing investors with jaw-dropping growth rates and incredible dominance within the graphics processing unit (GPU) industry. However, challenges are starting to arise within its business (even though it’s still dominant), with competitors building up their AI offerings and customers starting to design their own AI chips to train software models.

All of this leads me to believe there’s another company that’s a better AI investment, Taiwan Semiconductor Manufacturing (TSM -1.29%). Regardless of which AI company you’re talking about, it’s likely a TSMC customer because TSMC is the world’s largest contract chip manufacturer. This means it acts as a fabrication shop for all things chip-related. With massive demand across the board, it’s set to benefit whether Nvidia continues its dominance or others knock it from its perch.

TSMC’s new product will be an important innovation

TSMC has sat atop the semiconductor throne for a while. It has competitors, but none offer the scale and technology that it does. It can produce the world’s smallest and most powerful chip, which has a distance between traces of 3 nanometers (nm). It also has a 2nm chip in development that will significantly improve on the energy efficiency of the 3nm chip, which is fantastic news for companies building out their AI computing power.

The GPUs in these data centers are energy-hungry and cost a lot to run. If customers can outfit them with products that have similar performance but improve energy consumption by 25% to 30%, they will be a massive hit. Pre-production demand has already surpassed that of previous-generation chips (3nm and 5nm), so this is a huge catalyst that will be realized once TSMC’s 2nm chips enter production in 2025.

This demand adds to management’s projection that AI demand will grow at a 50% compounded annual growth rate (CAGR) through 2028 and will account for more than 20% of its revenue by then. Over the long term, management sees its revenue growing by a CAGR of 15% to 20%, which is a fantastic rate by all measures.

But that pales in comparison to what Nvidia is seeing, so why would investors want to pick TSMC over Nvidia? It all has to do with steadiness.

TSMC is a more consistent company

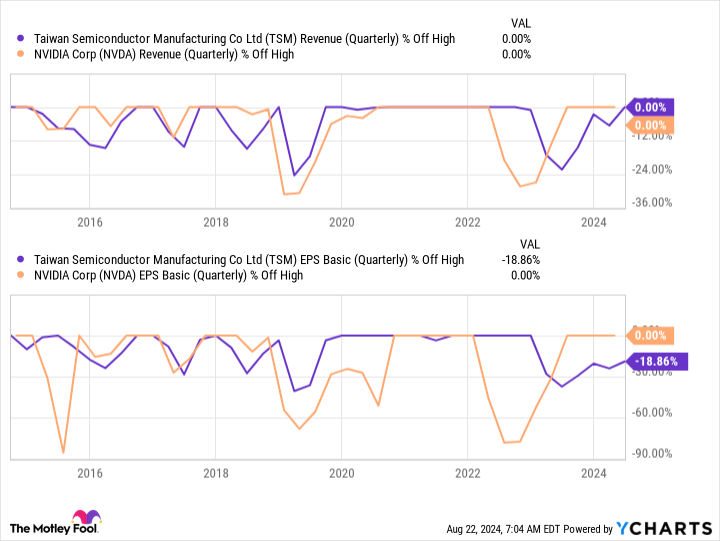

Both Nvidia and TSMC are cyclical businesses, but Nvidia’s volatility during a cycle is far greater than that of TSMC. Take a look at the chart below, which graphs the percentage of each company’s revenue and earnings per share (EPS) that fell from all-time highs.

TSM Revenue (Quarterly) data by YCharts

As you can see, Nvidia’s dips are far deeper than TSMC’s, which shows its decline at the bottom of a cycle is far greater. This likely has to do with TSMC’s product breadth, as its chips go into far more products than just GPUs.

Nvidia is a one-trick pony, even if that trick is amazing.

While some investors are OK with Nvidia’s booms and busts, I’m not. Recognizing your appetite for risk is a huge part of investing, and if you’re a bit concerned about how Nvidia will perform due to its massive run-up already, then TSMC is a great substitute to capitalize on the same tailwinds that are propelling Nvidia higher.

Keithen Drury has positions in Taiwan Semiconductor Manufacturing. The Motley Fool has positions in and recommends Nvidia and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.