The tech market has yet to bottom out, and investors should be avoiding the mega-caps at all costs, but there are emerging stars from AI and gaming to semiconductors that underpin the new tech trends–and they’re undervalued, not overvalued.

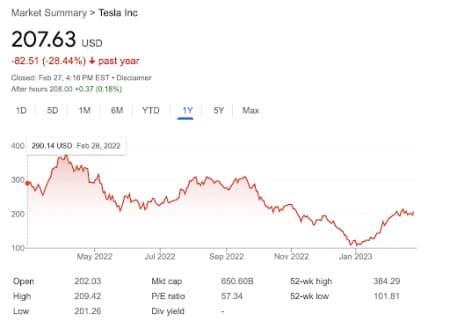

Tesla (NASDAQ:TSLA) is tanking. In the past 12 months, the stock has shed nearly 30%, with Elon Musk trying to explain away the nosedive for months.

The tech market is a sea of red right now, and it’s dragging Wall Street down with it.

Shopify (NYSE:SHOP) has lost nearly 42% in the past year.

Coinbase (NASDAQ:COIN) has tanked nearly 70% in the same time period.

Even Meta (NASDAQ:META) has shed almost 20%.

This is now a time of reflection, where investors should be looking deeper into the less obvious corners of the tech world, where brilliant things are being accomplished, and where valuations are still very low.

There is only downside in the mega-cap tech stocks, but we see all kinds of upside in some lesser-known stocks in the AI, gaming, and semiconductor playing fields.

#1 Chatbot GPT trailblazer BigBear.ai (NYSE:BBAI)

Chatbot GPT is the hottest AI buzzword right now, and any software company associated with it has been surfing these tailwinds. Chatbot GPT itself is privately owned and reached some 100 million monthly active users in January–only two months after it launched. That makes it the fastest-growing consumer application in the world–in history.

Microsoft has dumped billions of dollars into OpenAI’s ChatGPT, and that fact has led investors to start scrambling for any company that is working on AI tech.

BigBear.ai is one of them, and it’s up over 300% year-to-date.

An emerging leader in AI analytics and cyber engineering solutions, BigBear is one of the most exciting stocks in a space that has overtaken the crypto craze.

This new entrant is still in the red. While it’s been growing its revenue base, with up to $170 million projected for 2022, earnings closed out Q3 last year with $16 million in net losses. But what investors are looking at is what comes next …

One of the key attractions for investors in recent days and weeks has been BigBear’s $900-million contract with the U.S. Air Force, announced in January.

Other stocks in this space that have also been riding 2023’s AI craze include SoundHound (NASDAQ:SOUN) and C3.ai (NYSE:AI), the latter of which has gained over 100% so far this year.

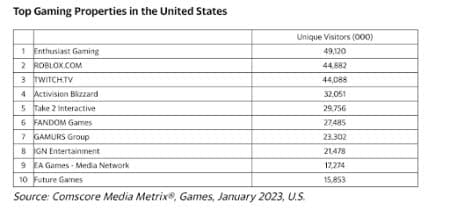

#2 Enthusiast Gaming (NASDAQ:EGLX), #1 in the U.S. for unique visitors this year

Online gaming is another craze taking over in 2023. This is quietly turning into a $50-billion subscription business, and Enthusiast stands out—not least because it was just ranked number one in the United States for unique visitors.

In this super fast-growing gaming segment, it’s all about traffic, and Enthusiast just won Comscore’s top ranking for unique visitor traffic.

Enthusiast Gaming operates an online network of approximately 50 gaming-related websites, 700 YouTube channels, a gaming development studio, not to mention the 500 or so gaming influencers it manages on Twitch and Youtube. It even owns and manages its own esports teams for the biggest names in gaming: Call of Duty, Madden NFL, Fortnite, Overwatch, Super Smash Bros., Rocket League, and Valorant.

For this segment, fans, fans, and more fans (in other words, traffic) is how gaming is monetized in a single “gaming house”. Enthusiast has created this house, with a massive base of people for advertising, subscriptions, ticket sales, broad-spectrum e-commerce, in-app purchases, premium content, NFTs, the metaverse, and even crypto.

And this new, pure-play entrant has hit the ground running, with RBC Capital Markets recently reaffirming their ‘Buy’ rating and a price target of C$3.50. That’s quite a lot of upside for a company now trading under $1.00.

Earnings, too, look strong, with Enthusiast’s Q3 2022 revenue coming in at $51.12 million, up from $37.06 million for the same quarter the previous year.

#3 Himax Technologies (NASDAQ:HIMX), the outlier in the chip war

Semiconductors are some of the best places to be as an investor right now, but they aren’t all equal. The chip war has only just gotten started, and a handful of countries dominate this crucial industry.

Himax is a leading Taiwanese semiconductor company that could end up being a multi-bagger. It’s one of the most profitable small-caps out there, and it’s smart. It’s trading cheaply relative to earnings. Indeed, as of mid-February, it was trading at a PE multiple of 6X.

Himax has a ROCE (return or pre-tax profit generated from capital employed) of 26%, compared to an average of 15% for the rest of the semiconductor industry. It looks undervalued at this point, likely because while it has the ability to compound returns by continually reinvesting capital and increasing rates of return, it’s only returned 14% to shareholders over the past five years. So no one’s paying attention–yet. That makes Himax the undervalued outlier in a booming segment that is the center of a global supply war.

Computer chips aren’t just vital for our daily electronics … They are the critical input for data centers, cars, and critical infrastructure. They are, in short, the new oil, and their supply is the stuff of geopolitics and national security.

American ally Taiwan produces more than 90% of the world’s most advanced semiconductor computer chips, and Himax is a very strong outlier in a space that has been difficult to navigate.

So, will 2023 bring relief to battered tech stocks? JPMorgan strategists write that value stocks have been market darlings last year because of high inflation and rising interest rates, but that in 2023, the pace of tightening may halt, and investors may move back into growth stocks. Two sub-sectors in tech that are drawing a lot of attention right now are chip-producers and video-game makers.

Take for example AMSL (NASDAQ:ASML) The Netherlands-based maker of high-tech semiconductor-producing devices. ASML’s machines help the world’s largest chipmakers to continue producing smaller and better chips, a process that has been improving since the 1960s. As mentioned above, companies that have a global competitive advantage in the chip-industry are not just investor’s darlings but have become targets of national interest. ASML is no exception here, as it even draws attention directly from the White House which looks to prevent the company from selling its much-coveted machines to its rival China.

For a company that the BBC once described as relatively obscure”, it has managed to not only become a leader in chip-making machines, it has as a matter of fact become Europe’s most valuable tech firm.

Just like ASML and Himax Technologies, chipmaker Taiwan Semiconductor Manufacturing, better known as TSM (NYSE:TSM) has been in the spotlights last year. Often dubbed as the most advanced chipmaker in the world, the company has received offers from various countries to open new production facilities as governments around the world are starting to realize the importance of domestic chip manufacturing.

According to a recent Bloomberg article, Washington has offered some $50 billion in tax incentives to woo chipmakers, and countries such as Japan have come up with similar incentives to attract tech companies such as TSM. Last week, the Taiwan-based company revealed plans to open a second chipmaking plant in Japan in southwestern Kumamoto prefecture, with total investments nearing $7.4 billion. TMC’s second plant is set to come online in the late 2020s according to Bloomberg.

Moving over from hardware to software, the most interesting stocks from an investor perspective are videogame makers such as TakeTwo and EA Sports (NASDAQ:EA). The latter, which has produced well-known series of games such as FIFA, the Sims and Battlefield has disappointed investors throughout 2022 as delays and cancellations have had an impact on earnings. As a result, the stock has fallen to a new 52-week low following its earnings report earlier this month.

Cowen analyst Doug Creutz, who has an outperform rating on the stock, lowered his target price to $136 from $158, and said that the disappointment was “across the board.”

However, despite poor earnings and delays, the pipeline for 2023 continues to look strong, with big releases such Star Wars Jedi Survivor, FIFA Mobile and EA Sports PGA tour coming up.

EA’s rival Take-Two Interactive (NASDAQ:TTWO) has in many ways followed a similar pattern. Both video-game developers recently lowered their outlook and reported weaker earnings, but in a few ways, Take-Two is looking better than its peer. To start with the negative news, the company sees lower spending for some of its pricier content as consumers are starting to become more cautious about spending on entertainment such as streaming services and video-games. Take-Two’s acquisition of Zynga, the well-known producer of mobile video games has put it on a much faster track to growth, but has weighed on its finances.

While both stocks have become ‘cheaper’ over the course of last year, Take-Two is looking like the high-risk, high-reward option of the two, as much of the company’s success this year will depend on a few large releases.

When it comes to video-games, the most steady stock is perhaps Microsoft (NASDAQ:MSFT)

Microsoft’s acquisition of Activision Blizzard solidified it as a major player in the video game industry. With the move, it became the third-largest gaming company by revenue, trailing only Tencent and Sony. The acquisition has given it access to some of the most popular video game franchises like Call of Duty and Candy Crush.

Additionally, with its strong ecosystem around Xbox Game Studios and Xbox Game Pass, Microsoft is well-positioned to take advantage of the growing trend towards subscription-based services in the gaming industry. Overall, Microsoft’s influence on the video game industry makes it an attractive investment opportunity for investors looking for exposure to this sector.

The most headline-worthy trend in tech right now is undoubtedly AI. ChatbotGPT, the famous artificial intelligence chatbot that allows users to converse with various personalities and topics has been one of the most interesting tech developments recently. It’s no surprise then that big tech companies such as Nvidia (NASDAQ:NVDA) are realizing the earnings potential of AI-as-a-service. The blue-chip tech company which has seen its share price fall more than 50% in 2022, before recovering again at the end of last year, is eyeing new avenues of growth, and AI is certainly one of its best bets.

Nvidia newest H100 GPU is supporting much stronger AI-workloads, and is therefore poised to become the leading platform for deep-learning and large-scale AI networks. As the AI sector’s demand for data computing grows, Nvidia wants to provide developers with more firepower.

Given its exciting pipeline of AI-focused enterprise products and services, the company has given investors reason to be bullish again in 2023.

By. Tom Kool

Read this article on OilPrice.com