Nvidia’s recent stock split hasn’t changed its fundamental value, but three other things could drive its share price higher.

Nvidia (NVDA -0.71%) stock has more than tripled over the past year alone, to trade at just over $1,208 as of the market close on Friday, June 7. That price made it somewhat inaccessible to smaller investors, because buying one full share might have taken up a disproportionate amount of their portfolio.

To solve that problem, Nvidia executed a 10-for-1 stock split (effective on June 10), which increased the number of shares in circulation tenfold, in order to organically reduce the price per share by 90%. As a result, investors can now buy one share in Nvidia for just $120 or so.

Some Wall Street analysts think the stock split will send Nvidia shares higher in the short term because it attracts a broader investor base, but it’s important to remember that it hasn’t changed the fundamental value of the company. Here are three better reasons to buy Nvidia stock.

1. Lightning-fast revenue and earnings growth

Nvidia’s financial results are the core reason for its surging stock price. Demand is off the charts for the company’s graphics processing chips (GPUs) for data centers, because they are the best in the industry when it comes to training artificial intelligence (AI) models. I’ll discuss this further in a moment.

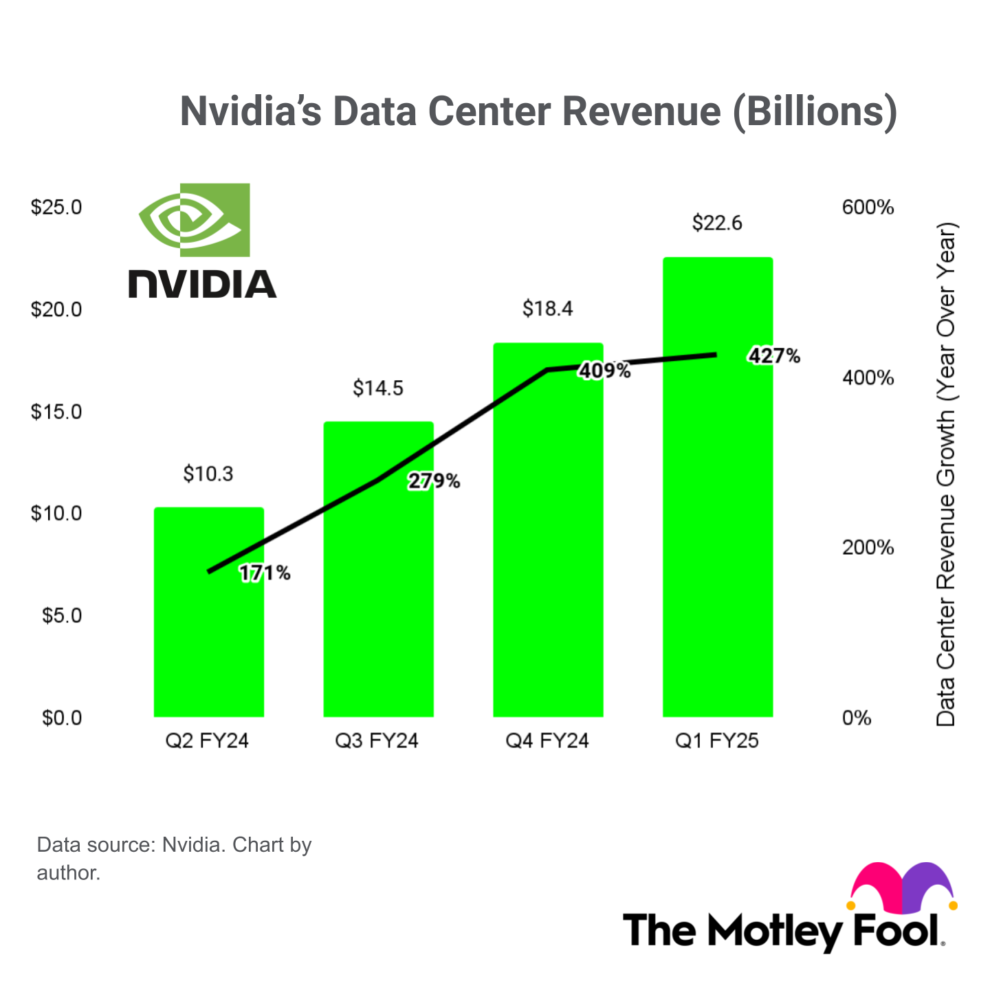

In the recent fiscal 2025 first quarter (ended April 28), Nvidia’s data center revenue surged 427% year over year to a record $22.6 billion. It was the latest in a string of incredible results over the past year:

Considering that Nvidia has an estimated market share of more than 90% in the AI data center GPU industry, it has significant pricing power, which translates to remarkable profitability. As a result, the company’s non-GAAP earnings per share soared 461% year over year during Q1, to $6.12, which followed a series of similar results (note: you can divide the below figures by 10 to account for the stock split):

2. A trillion-dollar long-term opportunity

Some of Nvidia’s biggest customers include cloud giants like Amazon, Microsoft, and Alphabet‘s Google. They fill their data centers with advanced chips like Nvidia’s H100 GPUs, and they rent the computing power to businesses and AI developers.

Nvidia says cloud providers can earn $5 in revenue over four years for every $1 they spend on data center hardware, because of the incredible demand for that computing power. That equation might grow even more profitable in the future, because Nvidia continues to release chips with better capabilities.

The company’s new GB200 superchip, for example, is based on its new Blackwell GPU architecture, and it can inference AI models five times faster than the H100. Inferencing involves feeding live data to an AI model so it can make predictions, which makes them faster and more accurate. Blackwell chips are already in production and are expected to reach customers next year — if H100 demand is any indication, they should be sold out long into the future.

In fact, Nvidia CEO Jensen Huang says the $1 trillion worth of existing data center infrastructure globally will have to double over the next five years to meet demand from AI developers. In other words, there’s a $1 trillion opportunity on the table, and considering Nvidia’s dominant market share, it’s poised to capture an enormous slice of that pie.

Competition is coming online from other leading chipmakers like Advanced Micro Devices, but it could take years for them to catch up to the performance of Blackwell GPUs.

3. The stock is cheap

If you refer to the above charts, you can see Nvidia has generated $18 in non-GAAP earnings per share over the last four quarters. That converts to $1.80 per share now that the stock split is in effect, and based on Nvidia’s current stock price of $120.88, that places it at a price-to-earnings (P/E) ratio of 67.2. That’s more than twice as expensive as the 30.9 P/E ratio of the Nasdaq-100 index.

From that perspective, Nvidia stock doesn’t look like a good value today. However, the picture changes when you factor in the company’s future earnings. Wall Street expects Nvidia to generate $2.71 in earnings per share during fiscal 2025, which places its stock at a forward P/E ratio of 44.6. Then, in fiscal 2026, its earnings could rise to $3.59, which translates to a forward P/E ratio of 33.7.

Keep in mind those are the consensus estimates, which Nvidia regularly beats.

Simply put, Nvidia stock looks cheaper the further into the future you look, so holding it for the long term is critical. The below chart illustrates this perfectly, because it shows how Nvidia’s P/E ratio has declined over the past year despite its stock price tripling, because its earnings have grown so quickly:

NVDA PE Ratio data by YCharts

Of course, Nvidia won’t maintain its triple-digit percentage growth at the top and bottom line for much longer, purely because the numbers have become so large. Therefore, while its stock likely has more upside potential, the best gains are almost certainly in the rear-view mirror.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.