Investor excitement for artificial intelligence (AI) might be overhyped today. The stock market can at times seem like a manic-depressive being, exaggerating any positive or negative developments with rapid share price swings. With AI stocks like Nvidia soaring tenfold in just a few years, it is possible these stocks will head into a correction, given that they are priced for perfection at the moment.

This doesn’t change the fact that the generative AI sector is still in the early innings of growth. Some analysts estimate that spending on generative AI alone will reach $356 billion in 2030, growing at a 46% annual rate over the next six years, making it one of the fastest-growing sectors in the world. That would be up from an estimated $36 billion this year. With its premium valuation, a company such as Nvidia already has a lot of this growth priced into its stock.

However, there is one reasonably priced AI stock hiding in plain sight: Alphabet (GOOGL -1.71%) (GOOG -1.58%). Here’s why the technology giant will benefit from surging demand for generative AI through 2030.

Alphabet’s AI comeback

OpenAI struck fear into Alphabet investors back in late 2022. With the rapid growth of ChatGPT and its advanced conversational AI tools, investors worried that Alphabet — parent company of Google Search — had fallen behind in AI. This led its stock to fall to a price-to-earnings ratio (P/E) of close to 15 in early 2023, its cheapest earnings ratio in a decade.

In the last two years, Alphabet has proven these doubters wrong. The stock has posted a 90% total return since these 2023 lows. Through its various subsidiaries and research labs, Alphabet has copied or bested every single one of OpenAI’s innovations and has come up with some new AI products of its own.

There is NotebookLM, a document summary tool that can speak audibly or provide written summaries on complex topics. There are also the new Google Search AI summaries, which are helping improve the customer value proposition of the most-used product on the planet. Let’s not forget the new Google Lens feature, which allows people to search by taking a picture instead of the traditional text query.

The list could go on. Alphabet is winning outside of generative AI, too. Its self-driving start-up, Waymo, has expanded to multiple cities across the United States and now does 100,000 weekly rides, growing tenfold year over year. This is an underrated part of Alphabet’s business that is only enabled by its leadership in AI.

Betting on cloud revenue growth

Alphabet has proven in the last few years that it is not a lagging tech company in AI. In fact, you might be able to argue that the company is the definitive winner so far in this new generative AI space. But how will the company monetize all these new tools?

One way is through Google Cloud, Alphabet’s most promising subsidiary at the moment. The cloud computing giant takes all of Alphabet’s innovations in AI, computer chips, and data centers and sells these tools to third parties. Last quarter, Google Cloud revenue grew 35% year over year to $11.4 billion. Over the long term, investors should expect this fantastic growth to continue if the analysts are correct about booming generative AI spending through 2030.

At $100 billion in annual revenue and 25% profit margins — a milestone Google Cloud should reach within a few years — the segment will be generating $25 billion in operating earnings for the parent company. That is a sizable and growing chunk of its $105 billion in trailing consolidated operating earnings.

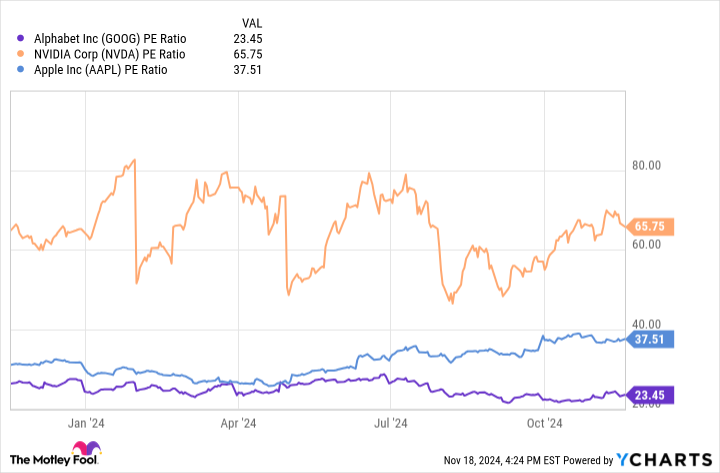

GOOG PE Ratio data by YCharts

Investors are still underrating the stock

Even though Alphabet is proving its might in AI both with product innovation and its financial performance, the stock is still not performing in line with other technology peers.

With a P/E of just 23, Alphabet has one of the cheapest earnings ratios across the AI and broader technology landscape. Nvidia has a P/E of 66. Apple — which is growing much slower than Alphabet and has shown little ability to succeed with AI products — is trading at a P/E of 37.

Generative AI revenue is going to soar through the rest of this decade. The one company set to take the largest slice of this revenue is Alphabet because of its plethora of AI products and monetization tactics. You can buy the stock today at a P/E of 23, well below the S&P 500 index average of 30. That is a recipe for producing fantastic long-term returns for your portfolio.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Brett Schafer has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Apple, and Nvidia. The Motley Fool has a disclosure policy.