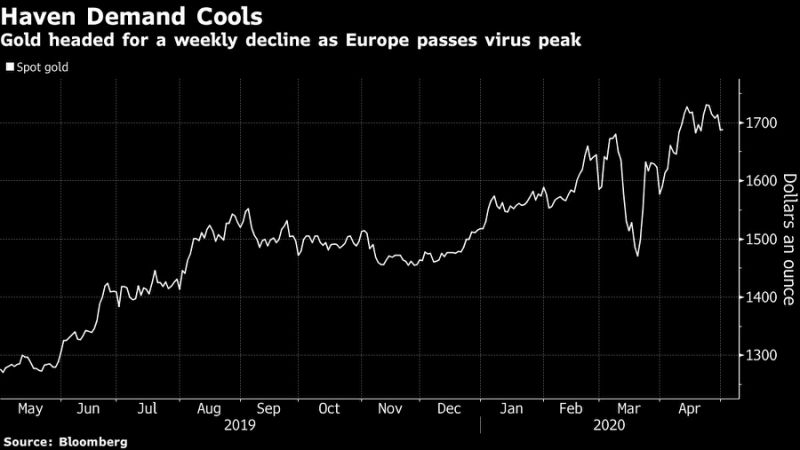

(Bloomberg) — Gold headed for its largest weekly decline in seven weeks as European nations, including the U.K., offered cautious signals they’ve passed through the peak of the coronavirus outbreak and as U.S. cases rose at the slowest pace this month.

U.K. Prime Minister Boris Johnson said the country was through the worst of the virus and pledged to deliver plans to lift the lockdown, while Italy, France and Germany all also outlined proposals to gradually ease restrictions. The European Central Bank stepped up its response to the coronavirus crisis by cutting funding costs for banks, but refrained from boosting its bond-buying program.

“Demand for safe haven assets took a further dive” after Johnson’s virus comments Thursday in the U.K., Australia & New Zealand Banking Group Ltd. economist Kishti Sen said Friday in a note. Asian trading was limited Friday, with much of the region out on holidays.

Spot gold declined 0.5% to $1,678.15 an ounce as of 3:51 p.m. in Sydney, after falling 1.6% Thursday. The metal was headed for its biggest weekly decline since March 13.

In other precious metals, platinum fell as much as 2%, while silver and palladium were both lower.

Industrial metals declined for a second day amid gloomy economic data, including deepening job losses in the U.S., and cratering exports from South Korea. Overseas shipments from South Korea fell 24% in April from a year earlier, led by declines in exports of ship, cars and auto parts, semiconductors and oil products.

U.S. and U.K. futures slid along with Japanese and Australian shares, and the dollar climbed, after sobering comments from Amazon.com Inc. and Apple Inc. about the impact of the coronavirus.

Metals fell as a “raft of Asian data pointed to troubles ahead,” including the export figures, and falling industrial production in Japan, Marex Spectron’s Anna Stablum said in an emailed note.

Copper on the London Metal Exchange fell as much as 1.9% to $5,090 a ton after a 1.4% decline Thursday. Nickel in London fell 1.4% and aluminum was 0.8% lower.

Iron ore futures in Singapore rose as much as 0.6% to $80.98 a ton. Demand for the steelmaking ingredient remains firm in China, according to producer Fortescue Metals Group Ltd.

“We are seeing economic activity resume and pick up, we are seeing steel inventories start to decrease and we are seeing very strong demand for iron ore,” Fortescue’s Chief Executive Officer Elizabeth Gaines said Thursday in a Bloomberg TV interview.

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="For more articles like this, please visit us at bloomberg.com” data-reactid=”52″>For more articles like this, please visit us at bloomberg.com

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="Subscribe now to stay ahead with the most trusted business news source.” data-reactid=”53″>Subscribe now to stay ahead with the most trusted business news source.

©2020 Bloomberg L.P.