The wide range of products and services Microsoft offers means its business faces fewer risks than other big tech companies.

The “Magnificent Seven” is a name given to a group of the world’s largest and most promising tech companies. Its members are Microsoft (MSFT 0.15%), Apple (AAPL 0.63%), Nvidia (NVDA 4.14%), Alphabet (GOOG 0.45%) (GOOGL 0.40%), Amazon (AMZN 0.04%), Meta (META -0.23%), and Tesla (TSLA -0.84%). Of those, Tesla is the smallest, with a market cap of about $700 billion. Needless to say, these are powerhouse companies.

There are great cases for investing in all of the Magnificent Seven companies, but Microsoft is the one I’m most excited about now. If you have $1,000 to invest (meaning you already have an emergency fund set aside and your high-interest debt is paid down), it could become a staple of your portfolio.

Microsoft is like a Swiss army tech knife

I like Microsoft going into 2025 because its business is much more diversified than the other Magnificent Seven companies. Its success — or lack thereof — won’t rely on a specific product or service. For perspective, here are products or services that will determine a lot about how the other Magnificent Seven stocks fare:

- Apple: As the iPhone goes, so does Apple. When iPhone sales are great, Apple’s revenue growth is great; when they’re down, it weighs heavily on Apple’s revenue.

- Nvidia: Nvidia’s success will be tied to the sales of its graphic processing units, which have become vital to the artificial intelligence pipeline.

- Alphabet: Advertising on Google Search is the backbone of Alphabet. Any slowdowns or disruptions to the advertising business will have tangible effects on its bottom line.

- Amazon: E-commerce is Amazon’s bread and butter. Amazon Web Services brings in the most profit, but e-commerce generates the revenue Amazon relies on to fund its other ventures.

- Meta: Advertising provided more than 98% of Meta’s revenue in its latest quarter. Any slowdown in the digital ad business will stall the company’s financial growth.

- Tesla: If Tesla can’t scale its electric vehicle production and hold onto its lead in the industry, the company faces a major uphill battle.

This isn’t a knock on any of the above businesses. I’m a strong believer in most of them. More than anything, it highlights how wide Microsoft has cast its business web.

Microsoft has enterprise software, consumer software, cloud services, gaming, social media, and hardware products, and it’s not overly dependent on any of them. Its largest business segment, Intelligent Cloud, only accounts for about 44% of its revenue.

You can’t argue against Microsoft’s financials

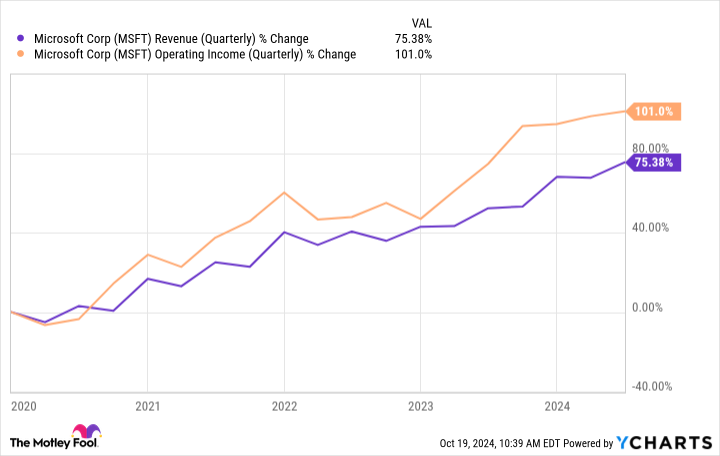

Microsoft’s strong financial performance in recent years is undeniable. In its fiscal 2024 fourth quarter (ended June 30), its revenue and operating income both increased 15% year over year to $64.7 billion and $27.9 billion, respectively.

MSFT Revenue (Quarterly) data by YCharts.

It has also doubled its operating income (profit from core operations) during the past five years — a great feat for a company of its size. It’s a testament to its operational efficiency and growth of high-margin businesses like its cloud platform, Azure.

Cloud computing will continue to be a high-growth area for Microsoft in the near future. Even if it doesn’t grow at the pace it has during the past few years (although it should), it will still provide a nice boost to Microsoft’s financials.

It’s not cheap, but it’s worth it for long-term investors

Admittedly, Microsoft is priced at a premium, though that has been the case for a while. The shares trade at about 31.6 times forward earnings, significantly higher than the S&P 500‘s average of 22.8. But rarely do world-class companies with as much attention as Microsoft trade at a bargain level, so it’s not too surprising.

MSFT PE Ratio (Forward) data by YCharts.

Anytime you invest in a stock that’s priced at a premium, you run the risk of limiting your near-term upside potential. Luckily, Microsoft has committed to returning shareholder value via dividends and stock buybacks.

Its $0.83 quarterly dividend gives it a yield of about 0.8% at the recent share price, but Microsoft has consistently increased its payouts through the years. Investors will also appreciate Microsoft’s recently announced $60 billion stock buyback program.

If you’re looking for an undervalued company or a true income stock, Microsoft likely won’t be your go-to pick. However, if you’re in it for the long haul, Microsoft is a stock you could feel comfortable buying and holding on to without too much concern about its current valuation.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Stefon Walters has positions in Apple and Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.