These AI stocks have delivered terrific returns so far in 2024, and they still have room to climb.

The advent of artificial intelligence (AI) systems has been one of the biggest drivers of stock market growth over the past couple of years. Shares of the technology companies best placed to make the most of the hot tech trend have soared, lifting the major indexes with them.

This explains why the Nasdaq-100 Technology Sector index’s gain of 75% in the past two years has outpaced the 54% rise in the S&P 500 index over the same period. That’s the reason why buying and holding AI stocks for the long run could turn out to be a smart move, especially as the technology is in its early phases of adoption.

McKinsey, for instance, forecasts that generative AI has the potential to boost the global economy between $2.6 trillion and $4.4 trillion annually. So, if you have $3,000 in investible cash right now after paying off your bills, settling any high-interest debt you’re carrying, and making sure you have set aside enough in an emergency fund, you should consider investing that money in shares of Nvidia (NVDA 3.96%), Palantir Technologies (PLTR -2.77%), or both.

Both companies have already delivered healthy gains to investors in the past year, based on their AI-related prospects, they are likely to deliver more upside in the long run.

1. Nvidia

Nvidia has played a pioneering role in the growth of the AI trend. Its highest-end graphics processing units (GPUs) have been deployed by major cloud computing providers, tech companies, and governments to train large language models (LLMs). The company has been supplying between 80% and 95% of AI chips sold, and its recent results indicate that it is unlikely to lose its dominance in this lucrative market any time soon.

Nvidia is growing at a much faster pace than its rivals. Its revenue soared by 122% year over year in the second quarter of fiscal 2025 to a record $30 billion, driven by a 154% increase in its data center revenue to $26.3 billion. That number far eclipsed the revenue that rival AMD is expecting to generate from selling AI GPUs for the entire year.

Nvidia’s market share dominance means that it is in pole position to benefit the most from the growth of the AI chip market, which (according to a forecast from Next Move Strategy Consulting) is expected to generate $305 billion in annual revenue in 2030. Japanese investment banking firm Mizuho predicts Nvidia’s revenue could hit $200 billion in calendar 2027 (which will run nearly parallel to its fiscal 2028). That would be more than triple the $61 billion revenue it generated in its fiscal 2024 (which coincided with the majority of calendar 2023).

Mizuho analyst Vijay Rakesh says the robust demand for Nvidia’s current generation Hopper chips and the arrival of its new Blackwell processors will be key catalysts for the company’s data center business. Additionally, the company is looking to make its presence felt in the enterprise AI software market, and it’s witnessing a rapid increase in its revenue from this segment.

Specifically, Nvidia expects to end the current fiscal year with a $2 billion annual revenue run rate in its software business, which would be twice its run rate at the end of the previous fiscal year. Mordor Intelligence forecasts that the enterprise AI market could clock an annualized growth rate of 52% through 2029, generating $311 billion in revenue that year.

Nvidia, therefore, is growing at a faster pace than this rapidly expanding market right now, and the opportunity present in enterprise AI means that it is capable of benefiting from AI adoption beyond just the hardware market. All this explains why buying this AI stock could turn out to be a smart long-term move.

After all, a $3,000 investment made in Nvidia stock at the beginning of 2024 would already be worth more than $7,000 as of this writing. It could deliver more such performances over the long run as well.

2. Palantir Technologies

While Nvidia is primarily a play on the fast-growing demand for hardware capable of supporting the processing demands of AI, Palantir is a play on the growing business uses for AI software. Investors have already seen how fast the enterprise AI market is set to grow, and this is the reason why there has been an acceleration in Palantir’s growth in recent quarters.

The company, which provides software platforms to both commercial and government customers, has been striking bigger deals and gaining more customers thanks to its Artificial Intelligence Platform (AIP). Palantir’s AIP helps organizations integrate generative AI into their operations, and the company has been aggressive with the roll-out of this platform. More specifically, Palantir hosts “boot camps” for potential clients where they focus on company-specific problems to show precisely how its generative AI can be used to make an operation more efficient.

These boot camps have been paying off. During its August earnings conference call, Ryan Taylor, Palantir’s chief revenue officer, noted:

Boot camps remain a key go-to-market motion, particularly for prototyping what is possible with AI, but the real opportunity and our unique capability lies in moving from prototype to production with these customers. That is where we are focused. We closed a seven-figure deal with a large wholesale insurance brokerage firm for an initial production automated policy review use case just 16 days after the boot camp.

Palantir also gave other examples where it has managed to convert boot camps into paid pilots or actual deals. All this explains why in Q2, the company’s revenue growth accelerated to 27%, bringing the top line to $678 million, as compared to 21% year-over-year growth in Q1. The company’s commercial revenue grew 33% to $307 million, while government revenue increased by 23% to $371 million.

More importantly, Palantir’s customer count jumped by 41% year-over-year to 593 last quarter. This healthy growth in the company’s customer base was accompanied by higher customer spending. Palantir closed 96 deals worth at least $1 million last quarter, up from 66 in the same quarter last year. Additionally, the number of deals worth more than $10 million increased by 50% year over year to 27.

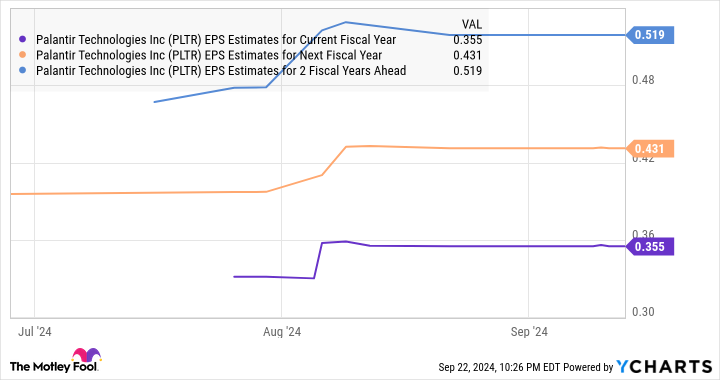

This improving customer base and stronger deal activity have led analysts to increase their growth expectations for Palantir for 2024 and the next couple of years.

PLTR EPS Estimates for Current Fiscal Year data by YCharts.

As the chart above shows, Palantir is expected to generate almost $4 billion in revenue in 2026. However, it won’t be surprising to see the company deliver even stronger growth considering its impressive revenue pipeline. Palantir’s total remaining deal value shot up by 26% year over year in the second quarter to $4.3 billion. This metric refers to the total remaining value of contracts that Palantir has yet to fulfill, which means that the company is positioned to sustain healthy levels of growth that could help it outpace analysts’ expectations.

As it turns out, Palantir is expected to clock annualized earnings growth of 85% over the next five years. So this AI stock looks likely to keep delivering healthy returns to investors. It is worth noting that Palantir stock has more than doubled so far in 2024, turning a $3,000 investment made in it at the beginning of the year into $6,500 as of this writing. It could repeat that feat in the long run, based on its huge addressable opportunity in the AI software market.