First published on Simply Wall St News

Amazon.com, Inc. (NASDAQ:AMZN) is getting stress tested as the stock erases the gains it made in the last 12 months and is currently some 3% in the red. Given that there is a lot of volatility in markets at the moment, we will step back and re-evaluate the fundamentals.

For investors, it is important to have a clear picture of the performance of a company, especially during uncertain times. That way, we can be more confident that a stock can regain whatever was lost in the short term.

We start our analysis by looking at how much and now efficiently Amazon grew in the last 12 months.

Growth

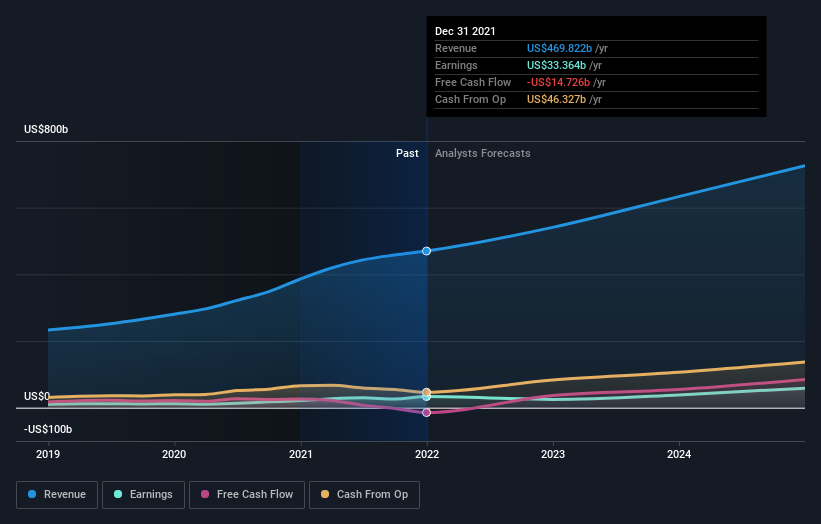

For a mega cap like Amazon, even their long term performance has been extraordinary. Some investors think that in crises “the strong get stronger”, and while it is not a rule, it does ring true for Amazon. In the last 5 years, Amazon.com, Inc. has increased its revenue by 245.5%, going from US$136b in December 2016 to US$469.8b in December 2021.

This amounts to a CAGR of 28.1% over that period.

Last year, the company’s revenues increased by 21.7%, which is less than the 3-year average growth rate of 28.2%. Albeit slightly, this is a sign that growth seems to be decelerating. Given how much the company is reinvesting, this seems to be within the expected fundamental growth rate of 14%, indicating that this growth is sustainable.

Fundamental growth is the long term growth we expect to see, based on how much and how well management reinvests in a company. Think “spend money in order to make money” – cliché but true.

View our latest analysis for Amazon.com

There are 2 more things we will go through when evaluating the quality of growth. These are COGS and total cost scaling. This essentially shows us if the company is reducing costs as it grows.

We look at how growth scales in relation to the costs of producing the product or service. In this regard, we take the last 12-month revenue growth and subtract the growth of costs in the same period. Amazon actually grew revenue -1.6% less than costs of goods sold, but this is considered noise since the percentage is so low.

Looking at gross margins across time, we see that Amazon has a 42% margin, which has been steadily growing over time. The company may still be prioritizing high growth before they intensify cost economics.

While growth vs. costs is one side of the coin, the other is growth vs. profitability. Some companies spend too much on marketing and other business expenses, while not managing to cover the loss in margins with enough growth.

It seems that the company negatively scaled revenues in relation to total costs by -4.0%. This means investors should take a deeper dive at the justification for expenses, as they seem to enable growth, but at the cost of profitability.

Margins

In the last 12 months, the company made US$24.9b in EBIT. This represents a margin of 5.3%. Which is less the median 3-year EBIT margin of 5.8%. This slowdown is too small to matter, and likely represents cyclicality or noise in the business.

EBIT margins are the point where expenses end, and we start calculating cash flows attributable to all investors. Since they are before debt, we should remember to factor-in the debt which helps the company generate these margins. They also help us assess profitability better, as they are usually more stable than net income.

When a margin is single digit, investors should also examine the cyclical nature of the business, and see how management handles tight periods. In the case of Amazon. The EBIT margin seems so low because the business is massively investing in R&D, and if we add back the associated amortization for the current year, we actually get a value closer to US$51.7b – representing an adjusted margin of 11%.

This shows us that profitability is a bit understated for Amazon, which is probably why many people find this business to be actually worth US$1.5t.

Now let’s move towards the future and compare analyst estimates with our fundamentals.

Future Estimates

After the latest results, the 44 analysts covering Amazon.com are now predicting revenues of US$540.8b in 2022. If met, this would reflect a meaningful 15% improvement in sales compared to the last 12 months. This is quite close to our calculated fundamental growth rate of 14%, and indicates that analysts’ estimates are justified based on how much Amazon is reinvesting into the business.

Whenever we try to make future projections, it is great to have more than one source, and then those sources are aligned, we gain even more confidence that this can materialize.

Unfortunately for Amazon, earnings are expected to drop by 27% to an EPS at US$47.85, and free cash flows are already down $-14.7b. For investors, this has 2 meanings:

-

Things might get worse before they get better for the stock.

-

If there is a macro-driven drop in the near term, it might be possible to use it as an entry point, since the stock is fundamentally strong and cash flows will return.

Valuation & Key Takeaways

The analysts reconfirmed their price target of US$4,129. This reflects a forward P/E of 84.7x with 2023 earnings. Currently, the stock is trading at a 41.9x P/E, so it seems that analysts are even more bullish on the company’s future than today. We should note that the price target comes from averaging out price targets from the 44 analysts that cover Amazon, so their position vary quite a bit.

That being said, here are the main takeaways:

The company is expected to grow revenue around 15%, this rate is justified based on how they are reinvesting back into the business.

Margins are low, but understated. They also have a cyclical pattern, and are still steadily growing.

While analysts are quite bullish with their price targets, the negative cash flow may indicate that things aren’t going to change for the better right away. However, the company is actually increasing in value and investors might be able to find a good entry amongst the short term volatility.

To get the complete fundamental picture for Amazon, view our updated daily report here.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.