Billionaires buy stocks for their own reasons, but some of these plays can also work for average investors.

Billionaire investor activity tends to gain the attention of individual investors. When it comes to the investment moves of Warren Buffett and others, many investors comb through billionaires’ quarterly 13-F filings to the Securities and Exchange Commission (SEC), looking for investment ideas and possible insights.

Admittedly, billionaires often make such decisions for reasons that would not help or interest the average investor. However, some of their investments indeed hold growth potential, and three Motley Fool contributors believe Alphabet (GOOGL -1.28%) (GOOG -1.35%), Uber Technologies (UBER 0.59%), and Texas Instruments (TXN -0.32%) could serve their shareholders well.

Bridgewater founder Ray Dalio is loading up on shares of Alphabet

Jake Lerch (Alphabet): It’s true: Billionaires love tech stocks. And among their favorites is Alphabet. Indeed, according to Motley Fool Research, Alphabet (along with fellow digital advertising giant Meta Platforms) tops the list as the most-owned tech stock at the end of 2023 among hedge funds run by billionaires.

In particular, Bridgewater Associates, founded by billionaire Ray Dalio, owned over $285 million of Alphabet shares at the end of 2023, making the company Bridgewater’s largest holding. However, Bridgewater has added even more shares of Alphabet this year. As of the fund’s latest filing in mid-May, Bridgewater now owns 5,368,853 shares, or roughly $951 million in Alphabet stock.

So, why is Bridgewater loading up on shares of Alphabet? The answer is simple: Dalio thinks Alphabet shares are cheap. In fact, he said as much in a report issued earlier this year to investors.

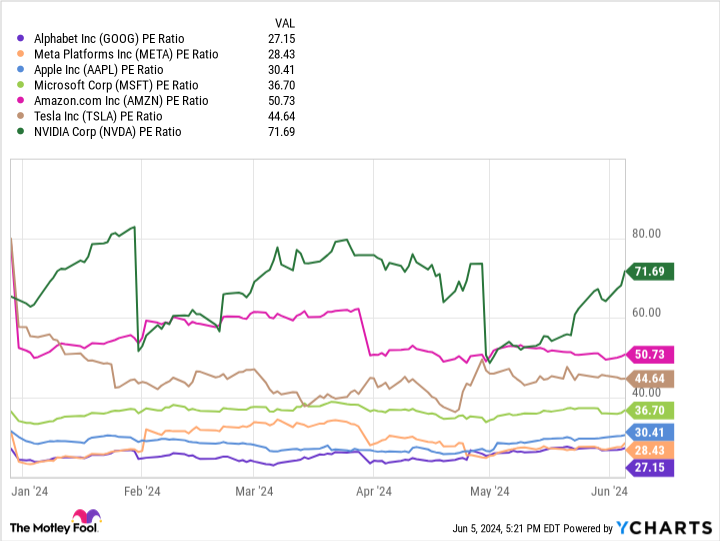

Specifically, Dalio highlighted that Alphabet’s stock is more affordable than several other stocks in the “Magnificent Seven” category — which is true. When considering a simple trailing price-to-earnings (P/E) multiple, Alphabet emerges as the most reasonably priced stock among the Magnificent Seven.

GOOG PE Ratio data by YCharts

A trailing P/E ratio is a time-tested measure that helps investors understand a stock’s value. The lower the ratio, the less investors pay for their share of the company’s profits. Conversely, the higher the ratio, the more investors pay for a company’s profits.

For a successful portfolio manager like Dalio, who is looking to balance growth and value, Alphabet offers the best of both worlds: A relatively modest P/E ratio and a revenue growth rate of roughly 15%.

So, for those looking for an affordable growth stock loved by billionaires, it’s time to consider Alphabet.

Uber’s future earnings growth makes the stock a bargain today

Justin Pope (Uber Technologies): According to research on hedge funds by The Motley Fool, Uber Technologies has become a popular pick among Wall Street’s wealthiest players. The ride-hailing leader sits in the top 10 holdings for four of the 16 hedge funds analyzed. When the research was published, it was the top tech holding of late billionaire fund manager Jim Simons’ Renaissance Technology.

What makes Uber so special? It’s become the de facto ride-hailing leader in the United States and has established a footprint worldwide. Uber has an estimated 76% market share in America, which helped it grow large enough to realize remarkable operating leverage in recent years. That means revenue grows faster than expenses, leading to rapid earnings growth.

You can see that Uber’s free cash flow began ramping up as revenue crossed $30 billion in late 2022:

UBER Free Cash Flow data by YCharts

Bottom-line earnings tend to follow cash flow. Analysts believe Uber’s earnings per share will grow by over 50% annually on average for the next three to five years. That seems attainable as Uber enjoys strong growth and drives new revenue streams. Uber is monetizing its platform traffic in new ways, such as advertising.

Shares are trading at a forward P/E of 76. That would normally seem expensive, but not if the business is growing profits as fast as analysts believe Uber will. The current PEG ratio of 1.4 signals the stock is attractive, considering Uber’s anticipated growth. Wall Street’s wealthiest seem to agree.

Active billionaire involvement could make Texas Instruments stock a buy

Will Healy (Texas Instruments): Perhaps one of the more unexpected billionaire investments is Elliott Management’s $2.5 billion purchase of Texas Instruments stock. Texas Instruments specializes in analog and embedded chips. It is best known for inventing the integrated circuit in 1958 and today for its industrial and automotive chips. It has 100,000 clients.

Under the previous CEO, Rich Templeton, it also became known for a dividend that grew at a 24% compound annual growth rate between 2004 and 2023. Since then, Templeton retired and Haviv Ilan took over as CEO.

It may be Ilan’s leadership that drew the attention of the fund run by billionaire Paul Singer. In 2024, its payout hike was only 5% amid an industry slump. Also, a $5 billion commitment to build additional fabs helped cause the trailing 12-month free cash flow to drop 79% in a year to $940 million, well under the $4.7 billion annual dividend expense.

In its letter to Texas Instruments’ board, Elliott noted the falling free cash flows and a belief that ambitions to add capacity far exceed anticipated demand. To this end, Elliott wants the company to increase its free cash flow above $9 per share by 2026, far above the current annual payout of $5.20 per share.

For now, investors may want to await the company’s response to Elliott’s shareholder activism before adding shares. Texas Instruments consistently outperformed the S&P 500 until about a year ago, implying that the semiconductor stock responded well to Templeton’s management philosophy. If Elliott can persuade the company to again prioritize free cash flows, the stock could again become a buy, especially for income investors.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Jake Lerch has positions in Alphabet, Amazon, Nvidia, and Tesla. Justin Pope has no position in any of the stocks mentioned. Will Healy has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, Tesla, Texas Instruments, and Uber Technologies. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.