One analyst predicts Nvidia’s data center business will see massive growth thanks to its new AI chips.

This year is shaping up to be a record-breaking one for Nvidia (NVDA 2.49%) investors as shares of the semiconductor giant have already shot up more than 91%, and there is a good chance that the stock’s rally could get a nice shot in the arm once Nvidia reports its first-quarter fiscal 2025 earnings on Wednesday, May 22.

Nvidia is heading into its next quarterly report riding on favorable developments within the artificial intelligence (AI) semiconductor market, which can help it crush Wall Street’s expectations. KeyBanc analyst John Vinh predicts Nvidia will deliver $5.81 per share in Q1 earnings on revenue of $25.6 billion. That’s higher than the consensus expectations of $5.57 per share in earnings and $24.6 billion in revenue.

Vinh’s forecast also exceeds Nvidia’s revenue guidance of $24 billion, and it won’t be surprising to see the company match the KeyBanc analyst’s expectations considering its immense pricing power and dominant share in the AI chip market. Those are precisely the reasons why Vinh forecasts a serious acceleration in Nvidia’s growth in the current quarter and the second half of the year.

Nvidia’s new AI chips could push data center revenue to $200 billion by next year

While Vinh points out that the solid demand for the company’s current-generation Hopper AI chips will allow it to beat Wall Street’s fiscal first-quarter expectations and also deliver better-than-expected guidance, he also claims that the next-generation AI chips from Nvidia are set to drive some serious growth for the company.

Nvidia’s new Blackwell chips are expected to hit the market in the third quarter of 2024. Vinh estimates that the new B100 and B200 processors, which will replace Nvidia’s current top-of-the-line offerings, could command 40% higher average selling prices (ASPs) than their predecessors.

As Nvidia ramps up the production of its Blackwell chips in 2025 and starts shipping the GB200 Superchip — which combines two Nvidia B200 GPUs (graphics processing units) with its Grace server CPU (central processing unit) — the company could pull in a massive $200 billion in data center revenue in 2025 (which will coincide with its fiscal 2026).

That would be a huge jump from the $47.5 billion in revenue that Nvidia generated in fiscal 2024 and the $87 billion it is expected to generate from AI chip sales this year (fiscal 2025). The company’s terrific pricing power in AI chips could drive such massive acceleration in Nvidia’s data center sales. According to HSBC, the company is expected to price its entry-level B100 GPU between $30,000 and $35,000. However, the GB200 Superchip could command a price in the range of $60,000 to $70,000.

What’s more, Nvidia’s server systems equipped with multiple CPUs and GPUs are estimated to command prices between $1.8 million and $3 million on average. It is worth noting that Nvidia management pointed out on the company’s February earnings conference call that it expects its “next-generation products to be supply constrained as demand far exceeds supply.”

So, despite a potential increase in pricing, the demand for Nvidia’s new chips is likely to remain robust. That is a testament to the company’s solid pricing power, as well as its ability to continue maintaining a solid share of the AI chip market. TechInsights estimates that Nvidia’s market share of the AI GPU market increased to 97% in 2023 from 96% in 2022.

Therefore, the company seems set to benefit from a combination of higher AI chip sales and improved pricing over the next couple of years, which is probably the reason why analysts have been raising their growth expectations for the company.

Why it would be a good idea to buy the stock

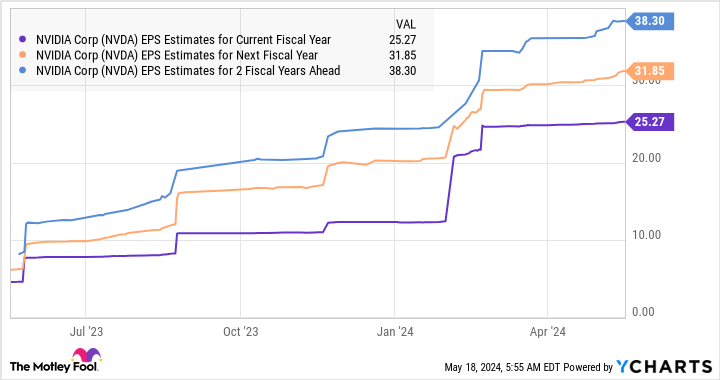

A closer look at the chart below tells us that Nvidia’s earnings estimates have been heading higher of late.

NVDA EPS Estimates for Current Fiscal Year data by YCharts

More specifically, the company’s bottom line could jump 52% in a couple of fiscal years from this year’s projected $25.27 per share to $38.30 per share in fiscal 2027. However, if Nvidia’s next-generation AI chips indeed hit gold, the company could end up delivering much stronger earnings growth.

The stock is currently trading at 38 times forward earnings, just below its five-year average. Investors, therefore, are getting a relatively good deal on Nvidia stock right now, and they should consider buying it since its red-hot rally seems here to stay thanks to the catalysts discussed above.

HSBC Holdings is an advertising partner of The Ascent, a Motley Fool company. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool recommends HSBC Holdings. The Motley Fool has a disclosure policy.