Investors are often guided by the idea of discovering ‘the next big thing’, even if that means buying ‘story stocks’ without any revenue, let alone profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

So if this idea of high risk and high reward doesn’t suit, you might be more interested in profitable, growing companies, like Cronos Australia (ASX:CAU). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Cronos Australia with the means to add long-term value to shareholders.

See our latest analysis for Cronos Australia

Cronos Australia’s Improving Profits

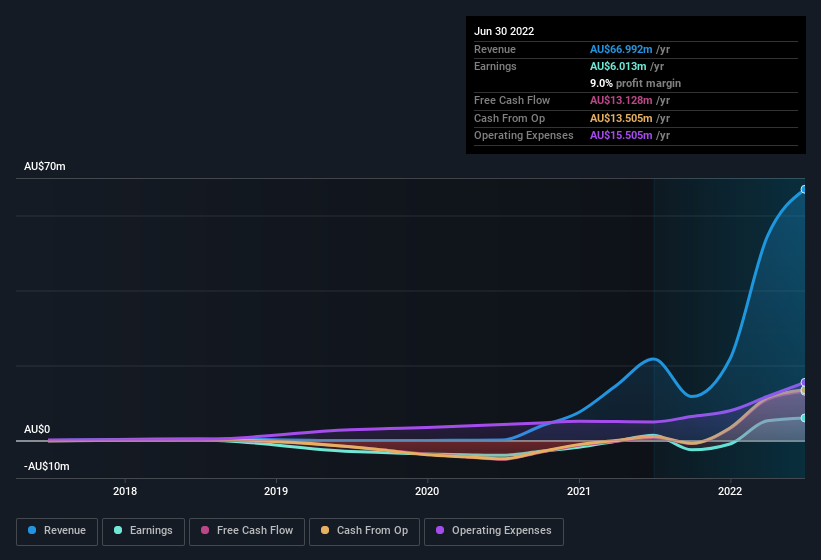

In business, profits are a key measure of success; and share prices tend to reflect earnings per share (EPS) performance. Which is why EPS growth is looked upon so favourably. Commendations have to be given in seeing that Cronos Australia grew its EPS from AU$0.0035 to AU$0.011, in one short year. Even though that growth rate may not be repeated, that looks like a breakout improvement. This could point to the business hitting a point of inflection.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. The music to the ears of Cronos Australia shareholders is that EBIT margins have grown from 7.8% to 15% in the last 12 months and revenues are on an upwards trend as well. Ticking those two boxes is a good sign of growth, in our book.

In the chart below, you can see how the company has grown earnings and revenue, over time. For finer detail, click on the image.

Cronos Australia isn’t a huge company, given its market capitalisation of AU$455m. That makes it extra important to check on its balance sheet strength.

Are Cronos Australia Insiders Aligned With All Shareholders?

It’s said that there’s no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. Because often, the purchase of stock is a sign that the buyer views it as undervalued. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

The good news for Cronos Australia shareholders is that no insiders reported selling shares in the last year. So it’s definitely nice that company insider Shane Tanner bought AU$49k worth of shares at an average price of around AU$0.35. It seems that at least one insider is prepared to show the market there is potential within Cronos Australia.

And the insider buying isn’t the only sign of alignment between shareholders and the board, since Cronos Australia insiders own more than a third of the company. In fact, they own 55% of the company, so they will share in the same delights and challenges experienced by the ordinary shareholders. This should be seen as a good thing, as it means insiders have a personal interest in delivering the best outcomes for shareholders. In terms of absolute value, insiders have AU$251m invested in the business, at the current share price. So there’s plenty there to keep them focused!

While insiders already own a significant amount of shares, and they have been buying more, the good news for ordinary shareholders does not stop there. That’s because on our analysis the CEO, Rodney Cocks, is paid less than the median for similar sized companies. Our analysis has discovered that the median total compensation for the CEOs of companies like Cronos Australia with market caps between AU$161m and AU$642m is about AU$984k.

Cronos Australia offered total compensation worth AU$801k to its CEO in the year to June 2022. That seems pretty reasonable, especially given it’s below the median for similar sized companies. While the level of CEO compensation shouldn’t be the biggest factor in how the company is viewed, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. It can also be a sign of a culture of integrity, in a broader sense.

Should You Add Cronos Australia To Your Watchlist?

Cronos Australia’s earnings have taken off in quite an impressive fashion. The cherry on top is that insiders own a bunch of shares, and one has been buying more. This quick rundown suggests that the business may be of good quality, and also at an inflection point, so maybe Cronos Australia deserves timely attention. What about risks? Every company has them, and we’ve spotted 2 warning signs for Cronos Australia (of which 1 is potentially serious!) you should know about.

Keen growth investors love to see insider buying. Thankfully, Cronos Australia isn’t the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here