(Bloomberg Opinion) — Since the U.K. decided more than three years ago to leave the European Union, the nation’s savviest investors have succeeded by putting their money where Brexit matters least.

Uncertainty about the date of Britain’s departure (now pushed back to Oct. 31) and the terms of the divorce has meant purging the U.K. from their holdings or limiting them to investments traditionally impervious to man-made and natural disasters. Over 38 months, British sterling depreciated 16 percent, the worst shrinkage for any similar period in 8 years. The pound remains the poorest performer in the actively-traded foreign exchange market and inferior to the No. 3 euro.

Europe’s strongest major economy in the 21st century became a shadow of its former self, reversing two decades preceding the June 23, 2016 referendum when the U.K. outperformed the European Union in growth and investment. London’s stock and bond markets similarly languished as laggards to world benchmarks, after beating them consistently in the 20 years prior to the decision to leave the EU, according to data compiled by Bloomberg.

“If I give myself some credit, I would say that we acted reasonably fast liquidating U.K. shares” in 2016, said Ben Rogoff, whose Polar Capital Technology Trust PLC has been the most consistent winner out of the 212 British global funds with at least 1 billion pounds this year and during the past three years. His team’s 114 percent total return (income plus appreciation) was 22 percentage points better than the Dow Jones World Technology Index, mostly because 68% of the fund is invested in the U.S., two-thirds of that in California companies, according to data compiled by Bloomberg. “It’s all about the Internet and where do you get exposed to the Internet? The U.S. and China,” Rogoff said last month during an interview at Bloomberg in London.

While Rogoff reduced his holdings of three California tech powers during the past year — Cupertino-based Apple Inc., Menlo Park-based Facebook and Santa Clara-based Advanced Micro Devices — he acquired more shares in Hong Kong-based Tencent Holdings Ltd, Hangzhou-based Alibaba Group Holding Ltd, South Korea’s Samsung Electronics Co. and Tokyo-based Yahoo Japan Corp., according to data compiled by Bloomberg.

The 46-year-old graduate of St. Catherine’s College, Oxford, became the lead manager of the trust in 2006, “and at that time,” he said, “the U.K. weighting might have been 5% to 10%, so if you had already been backing away to the door, it’s a lot easier to escape than if you built a career around being an expert in U.K. equities.” Since the Brexit referendum, he said, “There’s just been a complete buyers’ strike of U.K. equities.”

Proof of such disdain comes with the crisis this year at the LF Woodford Equity Income Fund, Britain’s most-prized investment when it was launched by star money manager Neil Woodford in 2014. The celebrated stock picker became even more prominent with his contrarian bullish stance on Brexit. The fund plummeted 31% during the past two years by holding a combination of large and small U.K. companies and has frozen redemptions indefinitely.

“It’s symptomatic of a broader problem,” Bank of England Governor Mark Carney told reporters earlier this month. “Our sense is that the financial-stability risks are increasing.”

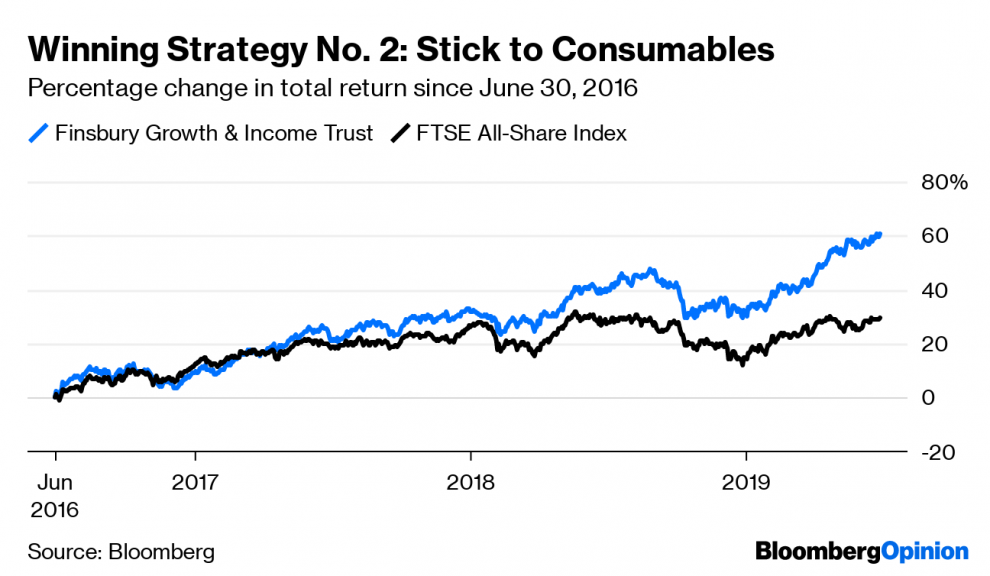

One U.K. investor who’s successfully resisted the trend away from domestic stocks is Nick Train, who manages Finsbury Growth & Income Trust. It returned 61% the past three years — more than twice the FTSE All-Share Index benchmark — as the most consistent one- and three-year performer among the 129 U.K.-based funds investing mostly in domestic stocks or bonds, according to data compiled by Bloomberg. Unlike Woodford, who doubled down on the British economy writ large, Train, a 60-year-old graduate of Queen’s College, Oxford, dramatically increased his holdings in consumer staples. These are the companies that make such essentials as food, beverages and household goods and can resist business cycles because their products always are in demand.

Train, who declined to be interviewed, increased the consumer staples weighting relative to the benchmark to 27% from 23% in 2015 and he enhanced his holdings of Deerfield, Illinois-based Mondelez International Inc., which manufactures and markets packaged food products, and London-based Diageo PLC, the world’s largest producer of spirits and beer, according to data compiled by Bloomberg.

That’s likely to be a safe bet as no one is counting on the British economy rebounding significantly from near the bottom of the EU while the uncertainty created by Brexit persists. “If you take a long view, then this may well be a great time to be investing in U.K. equity,” said Rogoff. “Thankfully, I don’t have to make that binary call because there are very few U.K. companies I’m frankly interested in.”

–With assistance from Shin Pei, Richard Dunsford-White and Kateryna Hrynchak.

To contact the author of this story: Matthew A. Winkler at [email protected]

To contact the editor responsible for this story: Jonathan Landman at [email protected]

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Matthew A. Winkler is a Bloomberg Opinion columnist. He is the editor-in-chief emeritus of Bloomberg News.

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="For more articles like this, please visit us at bloomberg.com/opinion” data-reactid=”65″>For more articles like this, please visit us at bloomberg.com/opinion

©2019 Bloomberg L.P.