Social Security needs help, but Congress has yet to decide which type of reform to take — and American voters aren’t sure either, but believe a solution can be found, a recent study shows.

The social safety net Americans pay into through their paychecks is facing insolvency in the next 15 years. The two trust funds that pay Social Security’s benefits (for retirees and people with disabilities) is expected to run out of money by 2035. If Congress does nothing by then, retirees will receive only 80% of their scheduled benefits, the 2019 Social Security Administration’s trustees report released earlier this year said. (Some experts say Congress has never let that happen, and it likely won’t.)

The federal government has taken retirement savings more seriously in recent months, especially as studies consistently show how little Americans are investing for their futures. But legislators have yet to agree on the numerous reform strategies they can take, arguing increasing taxation would hurt young workers who can’t afford it and lowered or delayed benefits could destroy elderly retirees on a fixed budget. Many Americans, especially young ones, don’t believe they’ll even see a Social Security benefit come retirement (but that’s not true).

See: This hybrid Social Security plan could help more people save enough for retirement

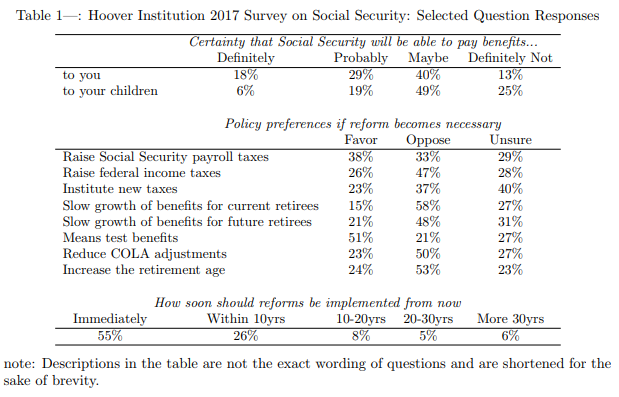

Americans believe Social Security can be fixed, but it will take some work, according to a recent study distributed by the National Bureau of Economic Research, which analyzed the Hoover Institution YouGov Survey on Social Security. Two-thirds of respondents agreed the program is facing a crisis, and 43% said minor changes could resolve those issues, according to the survey. The researchers, from Stanford University and New York University, looked at these reforms, and their timing:

• Benefit reductions beginning immediately, in 2019

• Benefit reductions beginning in 2035, the year the trust funds are expected to be exhausted

• A payroll tax increase beginning immediately, in 2019

• A payroll tax increase beginning in 2035, the year the trust funds are expected to be exhausted

• Indexing initial benefits by prices instead of wages, beginning in 2019 (price indexing can mean many things, the researchers noted, but in this case it refers to switching the index the Social Security Administration uses for benefits from national averages of wages to consumer prices, like the weighted average of a basket of goods and services Americans use).

• Benefit cuts that exclude current and near-retirees, beginning in 2019

• Benefit cuts that exclude current and near-retirees, beginning in 2035

Of course, keeping Social Security the same is always a preferred method, the researchers noted. “Any reform that improves Social Security’s financial outlook will necessarily make many worse off, in terms of lower projected benefits or higher taxes, compared with the impossible unfunded scenario,” they said.

But the status quo won’t work forever, and of the reforms legislators can take, the most preferred method of fixing Social Security was reducing or slowing the growth of benefits for high-income individuals. More than a third of participants also voted in favor of a payroll tax increase, though another third opposed that option. Only 15% of survey participants thought slowing the growth of benefits for current retirees was a good idea.

The researchers also pitted different reforms against one another in a hypothetical referendum, using the Hoover survey and the Social Security Administration’s assumptions. Participants who would have to choose between benefit reductions now or when the trust funds were exhausted would likely choose the latter. Between immediate tax increases or benefit reductions in 2035, they would likely choose waiting as well. Price indexing was the most preferred immediate reform, according to the study, though future tax hikes were also well-supported.

Also see: Setting the record straight on 5 Social Security myths

The researchers analyzed the Hoover survey and calculated the expected net present value of Social Security benefits and taxes for 112 archetypes (or types of beneficiaries), based on their birth cohort, marital status and work history. For example, a 65-year-old couple in a dual-income household in the lowest income cohort would have a present value of Social Security benefits equal to 12 times their yearly earnings at 65, while a similar couple also in a dual-income household in the highest income cohort would have a present value of benefits equal to 6.5 times their yearly earnings. (As income increases, the multiplier of the present value of their benefits decreases.)

Single earners in married households gain disproportionately because of the spousal benefit, which is generally 50% of the earning spouse’s benefit. A sole-income household pays the same amount of taxes for Social Security over the course of their lives as a single individual with the same earnings. Younger workers will pay more in taxes, but also receive more in benefits, because they will live longer to pay and receive them respectively.