This millennial claims he was FIRE before FIRE became popular.

FIRE refers to the “financial independence, retire early” movement bubbling up in the younger generation these days as a pathway out of the grind — slash expenses, save a bundle and enjoy the freedom that approach ultimately allows.

Read: Suze Orman’s bleak take on FIRE

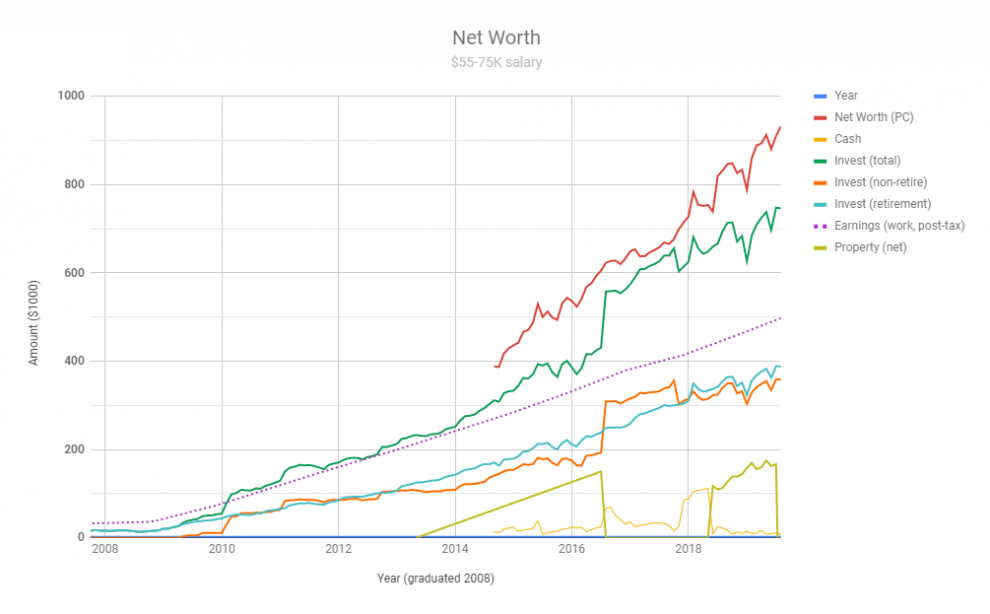

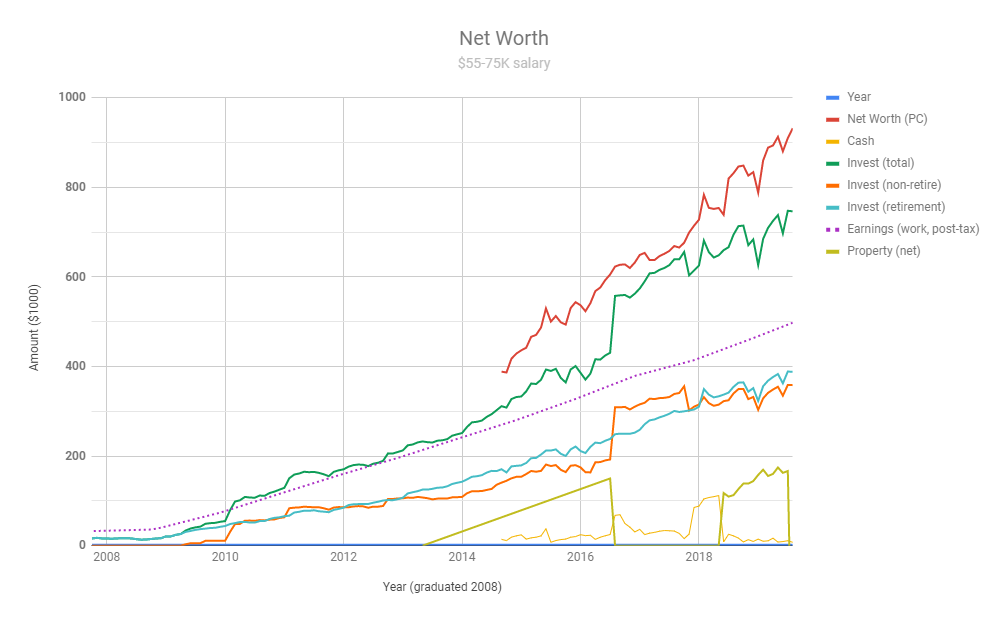

Using the name FluffayPenguin, one anonymous thirtysomething took to Reddit to illustrate his FIRE blueprint, which allowed him to graduate college in 2008 and build a small chunk of change all the way up to $930,000 in savings.

“My salary ($55K-$75K) has never been particularly high, so FIRE was always an attractive long-term solution for me,” he wrote. “Considering that I’ve only made roughly $450K post-tax from work over the past 10 years, I’m pretty happy with how much I’ve saved up. I don’t have any side jobs or blogs for supplemental income, so everything’s coming from my work and investments.”

Here’s what his journey looks like in one chart:

How did he manage to do it?

Well, for starters, he lived at home half of that time, a choice many millennials are making as housing costs skyrocket. Living rent-free allowed him to put big chunks of money away — up to a whopping 80% of his take-home, he said.

Not having a spouse or kids didn’t hurt either.

FluffayPenguin says his taxable accounts consist of investments in the Vanguard Total Stock Market fund VTI, -2.52% , and other similar ETFs. He also puts a “tiny percentage” of his money in Fundrise, an online platform that lets you get into the real-estate game with a minimal initial investment

“Sometimes, it feels like I’m investing with the Wizard of Oz. My account keeps paying regular dividends (~10% my first year. Now down to 6-8% due to drop in housing prices),” he wrote. “The company does give regular updates on what they invest, but nearly all of what they do is behind smoke and mirrors.”

He’s dabbled directly in real estate, as well, having eventually owned two houses — not at the same time — over that decade.

As for his retirement accounts, FluffayPenguin says he has broad-market funds held in a Roth IRA, a traditional IRA and a 401(k).

‘I’m preparing for that drop, and it’s fine. I’d be happy if it drops double-digits since I’ll just stick more money in.’

Readers cheered on his FIRE success story, though some pointed out reaching those numbers are unrealistic for those without the parental boost.

“This absolutely proves success from early compounding, no student loans and living with parents for an extended period of time,” one wrote. “There is a huge stigma with living at home, but when you can save >80%, it’s a very attractive alternative lifestyle.”

Of course, this kind of run also wouldn’t be possible without a surging market for home prices and a raging bull stock market, which, of course, won’t last forever.

“I’m preparing for that drop, and it’s fine,” FluffayPenguin countered. “I’d be happy if it drops double digits since I’ll just stick more money in.”

No double-digit drop on Tuesday, but both the Dow DJIA, -2.37% and the S&P SPX, -2.59% were trading lower at last check.