The technology giant is pushing out dozens of new updates to customers.

The tech arena is in the midst of a full-blown artificial intelligence (AI) boom. It seems like every company is doing something to take advantage of new AI advances, with leading computer chip provider Nvidia up hundreds of percentage points to a market cap of $2.5 trillion as of this writing. That is a lot of computing power.

No company is better poised to take advantage of the AI boom than Alphabet (GOOG -0.35%), the parent company of Google and YouTube. It may have the most data of any company in the world and billions of users. Yet a year ago investors were worried that Microsoft and OpenAI were far in the lead with these new chatbot tools, and that Alphabet was losing the race in AI.

Today I think it’s safe to say Alphabet has gained a lot of ground after its plethora of product announcements at the latest Google I/O event. Is Alphabet actually winning in AI now? Here’s what that could mean for the stock.

Bringing AI responses to Google search (and more)

Alphabet’s most important product is still Google Search, the dominant search engine used by billions around the globe with 90% market share. Now Google users will be getting generative AI search results when asking certain queries through its Gemini AI chatbot. This is not in every market yet, but is a step toward competing with upstart response query platforms like OpenAI and Perplexity. These responses are aimed to improve the value of Google Search, which will keep users from switching to places like Bing or OpenAI.

Perhaps more important is how Alphabet will be integrating Gemini into other products. From Google Maps to Google Photos to its Pixel hardware devices, Alphabet products will be getting Gemini advancements to improve the customer value proposition. Essentially, Alphabet wants to make all of its platforms smarter for users, further separating them from the competition. Time will tell how truly valuable these advancements are (Amazon Alexa, I’m looking at you), but Alphabet is back on the offensive, pushing out dozens of AI products to customers.

Enviable infrastructure advantage

AI products are great, but anyone who has studied this industry knows that they require a ton of computing power. This is why Nvidia is now one of the largest companies in the world.

Lucky for Alphabet investors, the company has been investing in AI computing infrastructure for over a decade. It released an update to its Tensor chips — a competitor to Nvidia — with a 4.7x improvement in performance. It has its own Google Cloud unit that now does tens of billions in revenue and is powered by these chips.

This year Alphabet expects to spend $50 billion on capital expenditures, mainly for AI infrastructure. There are very few companies that could even match this spending, and Alphabet has been at this for a long time. This is why the company can spread its AI tools to all of its products and billions of users, while start-ups have to raise $1 billion to maintain a user base of tens of millions.

Shareholders should be applauding the forward-thinking nature of Alphabet’s management. The company has the best AI infrastructure in the world, and is looking to improve it over the next few years as well.

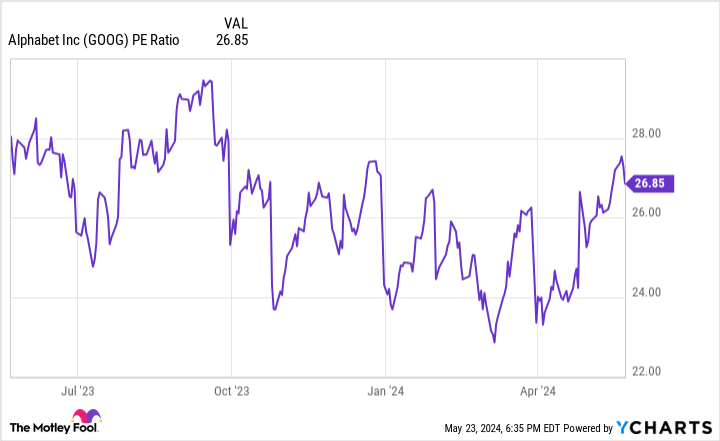

GOOG PE Ratio data by YCharts

Does all this matter for the stock, though?

All these AI products, but not a single focus on how to make money. That is what an investor might think when looking at these AI announcements from Alphabet.

While it is true the company is not making much money directly from AI today, I think Alphabet is set up nicely to benefit from AI growth over the long haul. Google Cloud can outsource these AI tools to third parties, which can bring in tens of billions in revenue over the next few years. Generative AI search can have advertisements included in links, which will drive further growth at Google Search.

And it is looking more and more likely that Google Search is not going to get disrupted by OpenAI, which was a major fear a year ago. With the stock at a price-to-earnings ratio (P/E) of 27, shares are not too expensive if you believe these AI tools can drive revenue growth over the long haul. Investors in Alphabet should rest easy knowing it is now leading in AI.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Brett Schafer has positions in Alphabet and Amazon. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.