The semiconductor giant is achieving record revenue thanks to AI.

In its brief tenure as a public company, semiconductor giant Arm Holdings (ARM 4.77%) has benefited from a skyrocketing stock. After debuting with an initial public offering (IPO) price of $51 per share last year, Arm zoomed to a 52-week high of $188.75 in July.

The price has dropped since then, but shares are still up nearly 100% in 2024. Its stock performance is understandable since Arm’s business has been on a tear, experiencing record revenue for four consecutive quarters.

Can the company continue growing sales? If so, given its elevated share price, does it make sense to invest in the semiconductor chip designer? To get to an answer, let’s dissect Arm to determine if it’s a good long-term investment.

Arm’s technological strengths

The foundation of Arm’s success lies in its semiconductor chip designs. The company dominates the mobile device market with over a 90% market share thanks to the energy efficiency of its chips.

That’s just the start. Arm’s power-efficient chip designs are increasingly in demand across a rising number of devices. This encompasses the Internet of Things, smart cars, and more, which bodes well for the company’s future.

Arm’s technology is used by the biggest names in tech. It’s employed by Nvidia in its semiconductor products, by Amazon Web Services (AWS) in cloud computing, and in Alphabet-owned Google’s consumer offerings, including the Pixel mobile phone and Nest smart home solutions.

With the arrival of power-hungry artificial intelligence systems, Arm’s energy-saving chip designs are in demand here, too. Management described the current market conditions by stating, “AI’s substantial energy requirements are driving growth in Arm’s compute platform, which is the most power efficient solution available.”

This brings me to a key factor in the company’s future success: its latest chip architecture, Armv9. The company recognized the need for a new chip platform to support the processing demands of artificial intelligence, and launched Armv9 back in 2021. The Armv9 architecture enables AI to quickly process the massive amounts of data needed to complete tasks while remaining energy efficient.

Adoption of Armv9-based chips is growing, and consequently, Armv9 comprised 25% of the company’s $939 million in sales during the fiscal first quarter, ended June 30.

Arm’s approach to revenue generation

Arm produces revenue in two main ways. First, it licenses its designs for semiconductor products. Then, it collects royalties on those designs, even years after the sale is completed. For instance, it’s still amassing royalties from products developed in the 1990s.

The complexity inherent in Armv9 means it commands higher royalties than previous generations of Arm architectures. This enabled the company’s Q1 royalty revenue to increase 17% year over year. Meanwhile, the AI-driven demand for energy-efficient, high-performance chips helped Arm grow Q1 license and other sales by a jaw-dropping 72% year over year.

With the AI era ramping up, management anticipates ongoing revenue growth. For its 2025 fiscal year, the company expects full-year sales in the range of $3.8 billion to $4.1 billion. This is an increase from its 2024 fiscal year revenue of $3.2 billion.

To buy or not to buy Arm Holdings stock

Arm’s market dominance in the mobile phone industry, the rising adoption of its Armv9 architecture, and its anticipated revenue growth for fiscal 2025 are all factors that make it a worthwhile investment.

The more difficult question is whether now is the time to buy Arm shares. The stock dropped on Oct. 23 as the company battled a legal dispute. Could this create the opening to buy?

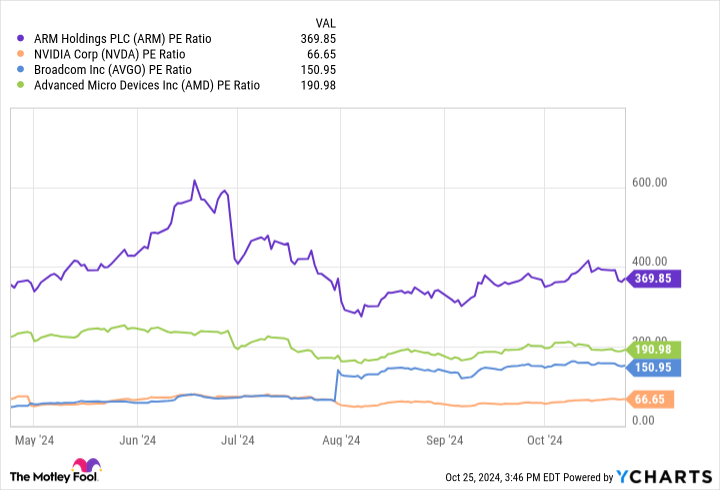

Looking at Arm’s price-to-earnings (P/E) ratio, a widely used metric to assess stock valuation, tells you how much investors are willing to pay for a dollar’s worth of earnings. Comparing it to other semiconductor companies, such as Nvidia, Broadcom, and Advanced Micro Devices, helps to evaluate if Arm stock is overpriced.

Data by YCharts.

Arm’s P/E multiple is far greater than others in the industry, suggesting its stock is still too pricey. Wall Street analysts have a consensus share price target of about $143 for Arm stock. With the shares closing at $143.75 on Oct. 25, Wall Street appears to concur that the current share price is still too expensive despite the recent dip.

So while Arm is a company to consider investing in for the long haul, given the elevated share price right now, it’s best to wait for the stock to drop further before deciding to buy.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Robert Izquierdo has positions in Advanced Micro Devices, Alphabet, Amazon, Arm Holdings, and Nvidia. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, and Nvidia. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.