Following an impressive first-quarter earnings report, shares in Alphabet are up big.

There are only seven companies in the world with a market capitalization of at least $1 trillion. Among these businesses, only Microsoft, Apple, Nvidia, and Alphabet (GOOG 1.06%) (GOOGL 1.08%) have reached an even more exclusive club.

No, I’m not talking about gaining access to the “Magnificent Seven” — although each of those companies is in that club, too. All four of these tech giants have a market cap of at least $2 trillion, and Alphabet is the newest member to reach that milestone.

Following an encouraging first-quarter earnings report, Alphabet’s shares have soared as high as 9%. Is it too late for growth investors to scoop up shares in Alphabet since eclipsing a $2 trillion valuation?

I don’t think so. In fact, now looks like as good a time as ever to scoop up some shares. Let’s explore why.

Don’t sleep on the advertising business

One of the biggest knocks against Alphabet over the last couple of years is that its core advertising business has been slowing down. Stiff competition from Meta Platforms, TikTok, and some smaller players, such as Pinterest and Snap, have found ways to attract cyclical advertising dollars away from Alphabet.

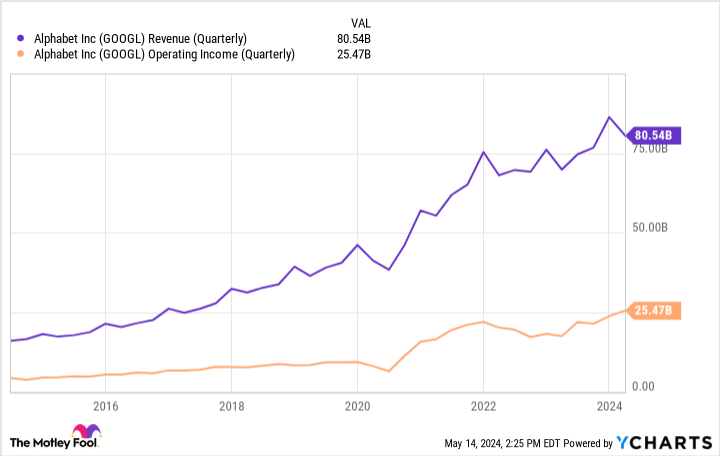

What I think investors are missing is that even though Alphabet’s advertising business may not be growing at levels seen in the past, this segment remains enormously profitable for the company. In fact, Alphabet’s advertising and services operations account for nearly all the company’s operating income — with cloud computing contributing nominal profitability.

GOOGL Revenue (Quarterly) data by YCharts.

The chart above demonstrates the growth in Alphabet’s operating income relative to revenue. Although Alphabet’s revenue has started slowing down a bit, the company is still achieving an impressive level of operating efficiency. This has resulted in significant margin expansion and robust free-cash-flow generation for Alphabet. It’s these excess profits that are fueling the next frontier of Alphabet beyond advertising.

Image source: Getty Images.

An end-to-end artificial intelligence platform

The hottest ticket in the technology realm right now is artificial intelligence (AI). Over the last year or so, Alphabet has made a number of strategic investments in AI. Namely, the company’s generative AI model (called Gemini) is Alphabet’s response to the highly popular ChatGPT.

Although ChatGPT may have a first-mover advantage, Alphabet has a secret weapon of its own: data. Remember, Alphabet owns Google and YouTube — the world’s top two most visited websites.

Alphabet collects an unprecedented amount of data. Considering large language models (LLMs) essentially rely on vast libraries of data, Alphabet has a competitive advantage that will be hard to match.

Where Alphabet really has an opportunity to leapfrog the competition is in integrating AI across its entire ecosystem. While Alphabet may be best known for Google and YouTube, keep in mind that the company also has a workplace productivity suite akin to Microsoft Office and a budding cloud computing business that grew 28% just during the first quarter.

The valuation narrative is compelling

The chart below benchmarks the forward price-to-earnings (P/E) ratio among mega-cap tech. Alphabet’s forward P/E of 22.6 is the lowest among this cohort.

GOOGL PE Ratio (Forward) data by YCharts. PE = price to earnings.

Shares in Alphabet rose significantly following first-quarter earnings due to the company’s demonstrated growth across the business and the strides it’s making in AI. Yet, even after a big upswing, the company is still valued at a noticeable discount compared to most of its peers.

It’s very possible that many investors are still narrowly focused on advertising revenue and missing the bigger picture: margin expansion, rising cash flow, and how Alphabet reinvests these profits. I think Alphabet stock is dirt cheap right now, and I see the disparity in valuation multiples above as a compelling buying opportunity.

Now looks like a lucrative time to take advantage of the current trading activity in Alphabet and scoop up some shares.

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, Pinterest, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.